Capital Concentration in an Expanding Crypto Universe

State of the Network #347

Capital Concentration in an Expanding Crypto Universe

Introduction

State of the Network #347

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- As the crypto investment universe expands, capital is becoming more selective across a smaller set of assets: Bitcoin dominance is in a sustained uptrend, while growth in stablecoins and onchain derivatives compresses the space for the altcoin segment.

- The altcoin segment is narrowing and becoming more top‑heavy, with the top 10 altcoins now representing about 82% of its value, up from roughly 70% over the prior five years.

- Large caps have decisively outperformed mid and small caps since 2023, and post‑shock behavior has reinforced a preference for more liquid, established assets.

Introduction

The crypto investment universe continues to expand. Hundreds of new tokens launch each year, the range of equities offering exposure to digital asset businesses is growing, and tokenization is bringing traditional assets like equities and commodities onchain. With this proliferation of options, capital is becoming increasingly selective.

Bitcoin dominance climbed back toward 65%, its highest level since early 2021. Meanwhile, stablecoins and onchain derivatives now account for nearly 12.5% of total crypto market cap. As a result, altcoins are being squeezed from both sides, with their collective share contracting even as the number of tokens grows.

In this issue of State of the Network, we examine whether the crypto market is experiencing a structural shift toward concentration. We analyze dominance and performance trends across market cap tiers and sectors to understand whether capital is gravitating toward fewer, larger, more established assets, or is opportunity still broadly distributed?

The Story of Market Cap Dominance

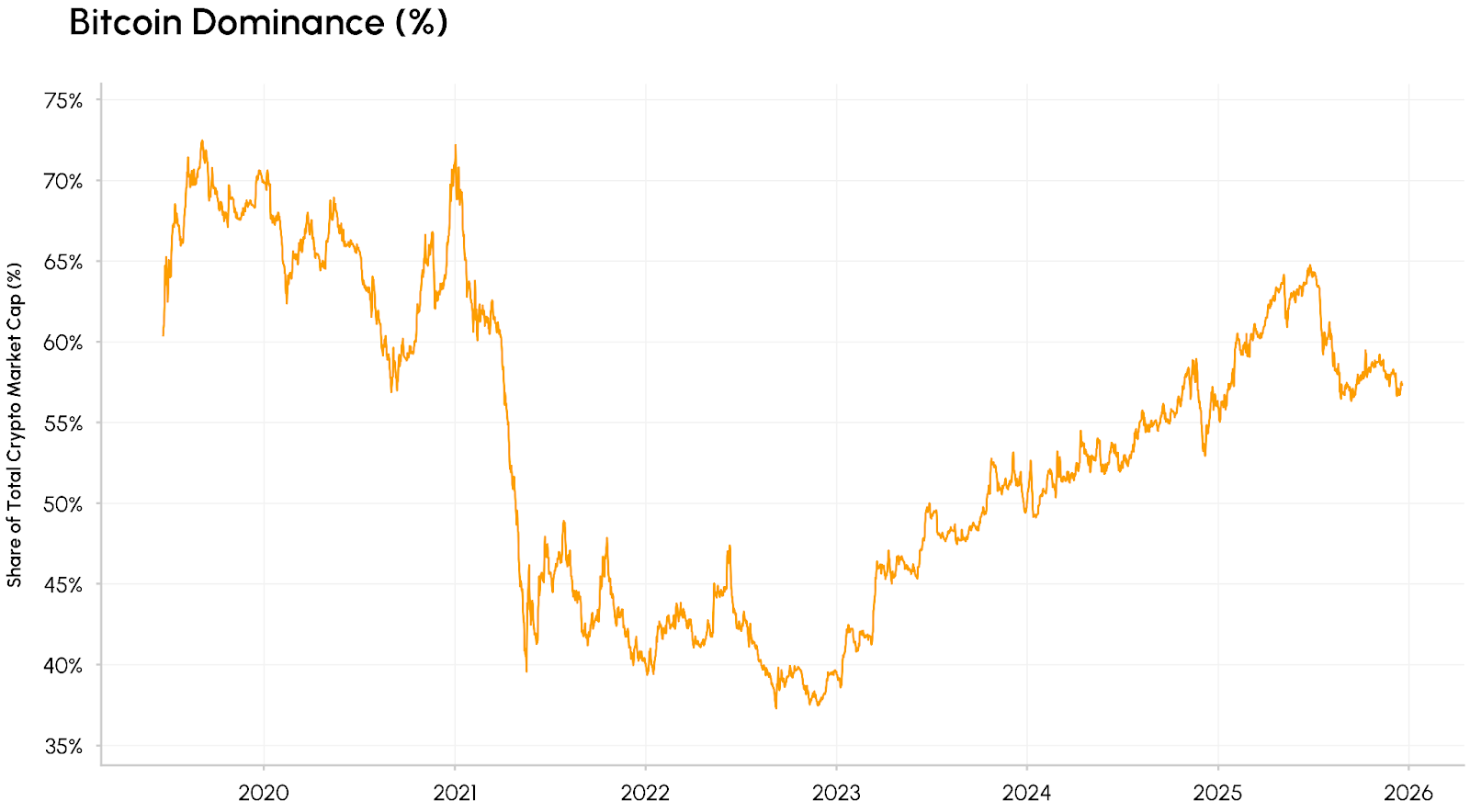

To begin, we examine market cap dominance. Bitcoin’s market cap dominance, measuring the market capitalization relative to the rest of the crypto market, has extended towards 65% in 2025—its highest level since 2021. Notably, this increase has played out over a relatively extended time frame, grinding higher since bottoming out in 2022.

This sustained rise in Bitcoin dominance has been compounded by increased institutionalization through spot ETF access, attracting over $150B in long term capital rather than short term retail flows. This has reinforced Bitcoin’s role as a “safe haven” in crypto markets and a liquid, regulated entry point for traditional allocators, making its dominance a more persistent phenomenon than in past cycles where “altcoin seasons” quickly eroded BTC’s share.

Source: Coin Metrics Network Data Pro

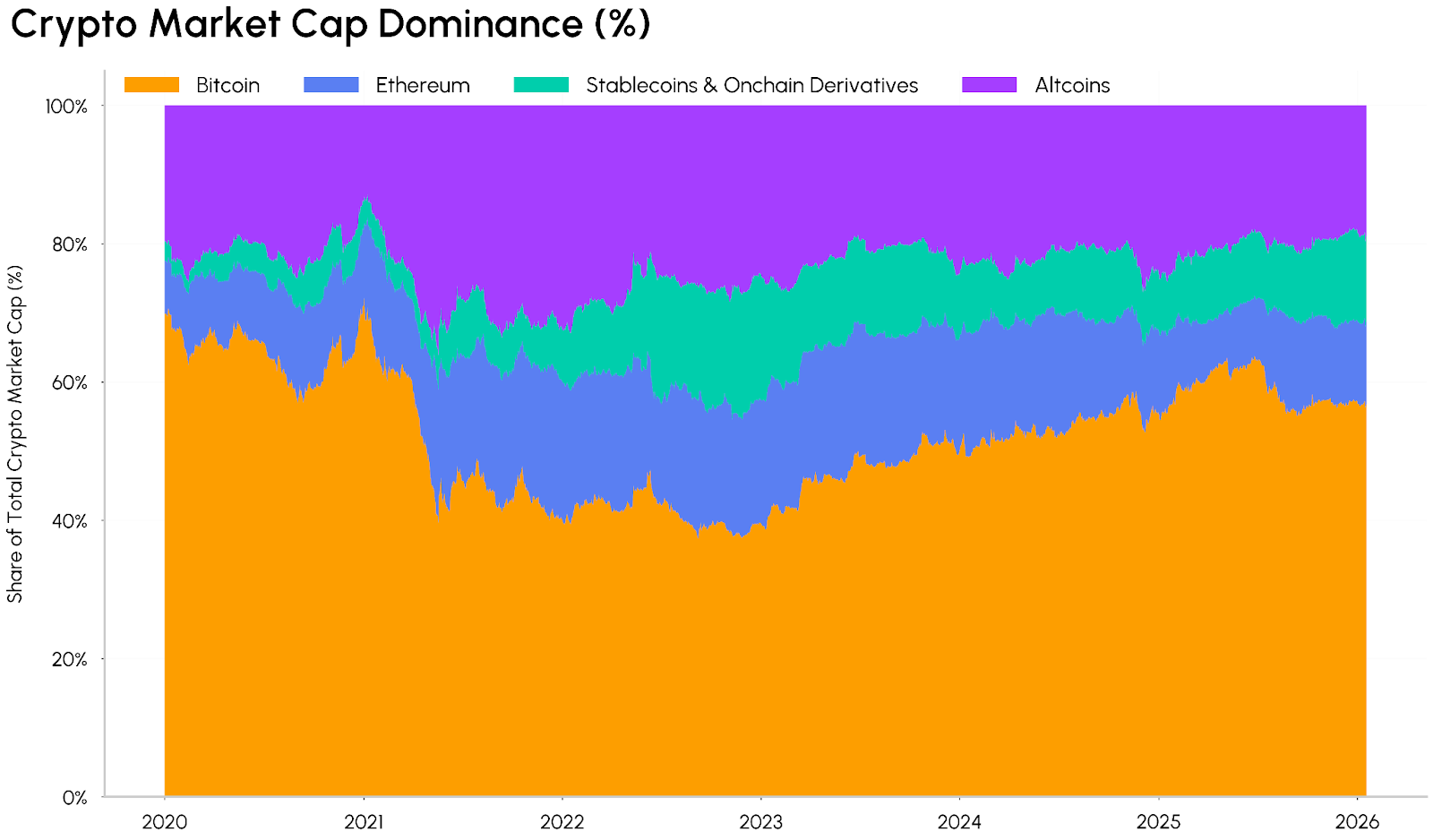

The composition of the rest of the market is also shifting. Stablecoins with a market cap of over $300B, and onchain derivatives (such as wrapped, staked, and bridged tokens) now account for a growing share of the total market. These tokens play a different role in the ecosystem, with stablecoins as the dominant medium of exchange, while onchain derivatives provide claims on underlying assets or yield generation.

Source: Coin Metrics Network Data Pro

As a result, the altcoin category is being squeezed from both ends. What remains is a smaller investable universe that is increasingly top-heavy, as value concentrates in more liquid, established assets with clearer utility, regulatory pathways, and exposure to the growth of stablecoins, DeFi, and tokenization.

Unlike previous cycles, capital has been slower to rotate from majors into altcoins, with ETFs and institutional vehicles keeping liquidity concentrated at the top. This dynamic could evolve as generic listing standards, altcoin and multi-asset ETFs broaden access to a wider set of large cap tokens, with market structure legislation as a further catalyst.

Concentration Among Altcoins

Within the altcoin segment itself, concentration is also rising. The top 10 altcoins (ex BTC) now account for ~82% of total altcoin market cap, up from a low of ~64% during the 2021 bull market. The long tail of smaller tokens that briefly captured value during the last cycle has given way to a more top-heavy structure with shorter narrative cycles that fail to sustain.

Source: Coin Metrics Network Data Pro

Another way to view this concentration is by looking at the number of tokens crossing certain thresholds. The number of altcoins with market caps above $1B has declined from a peak of ~105 in 2021 to ~58 today, even as total crypto market cap has reached new highs. The pool of “investable” altcoins appears to be shrinking even as the number of assets expand. While this does not bring doom for altcoins as a segment, interest is likely to cluster even more around durable fundamentals and resilience.

Source: Coin Metrics Network Data Pro

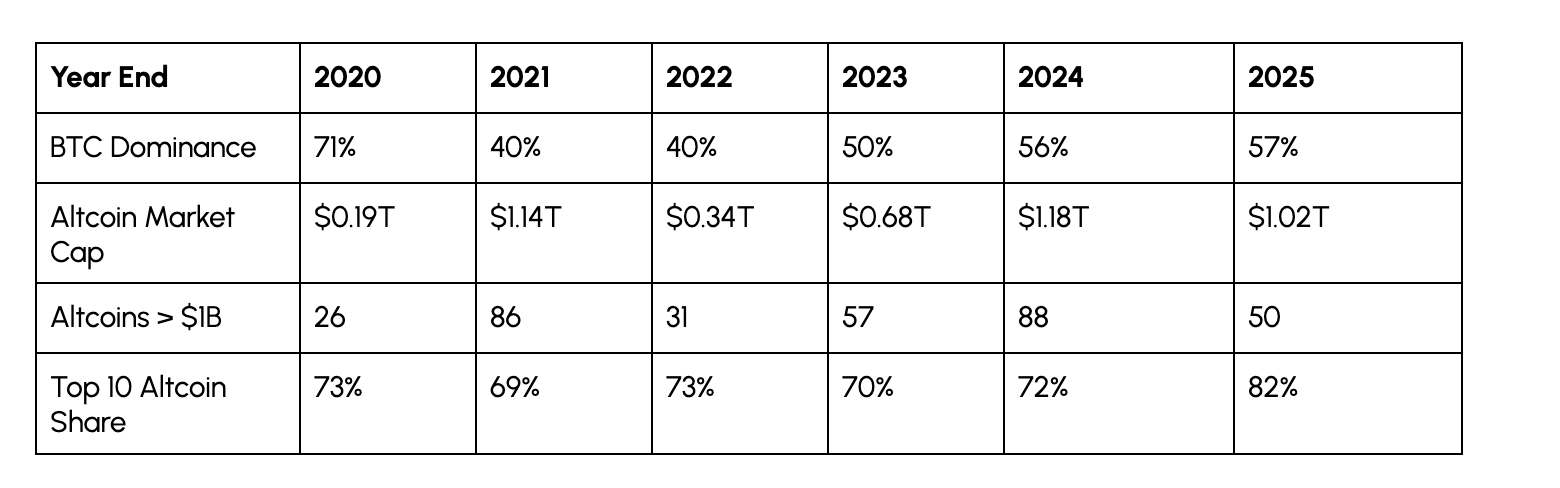

The table below summarizes how these dynamics have evolved year over year. While some metrics appear cyclical, with BTC dominance falling in bull markets and rising in bears, the market share of top 10 altcoins tell a different story. This metric remained stable at 69-73% across all market conditions from 2020-2024, then jumped to 82% in 2025, suggesting a structural or defensive shift toward established assets rather than just a temporary flight to quality.

Source: Coin Metrics Network Data Pro

A Flight to Majors & Large Caps

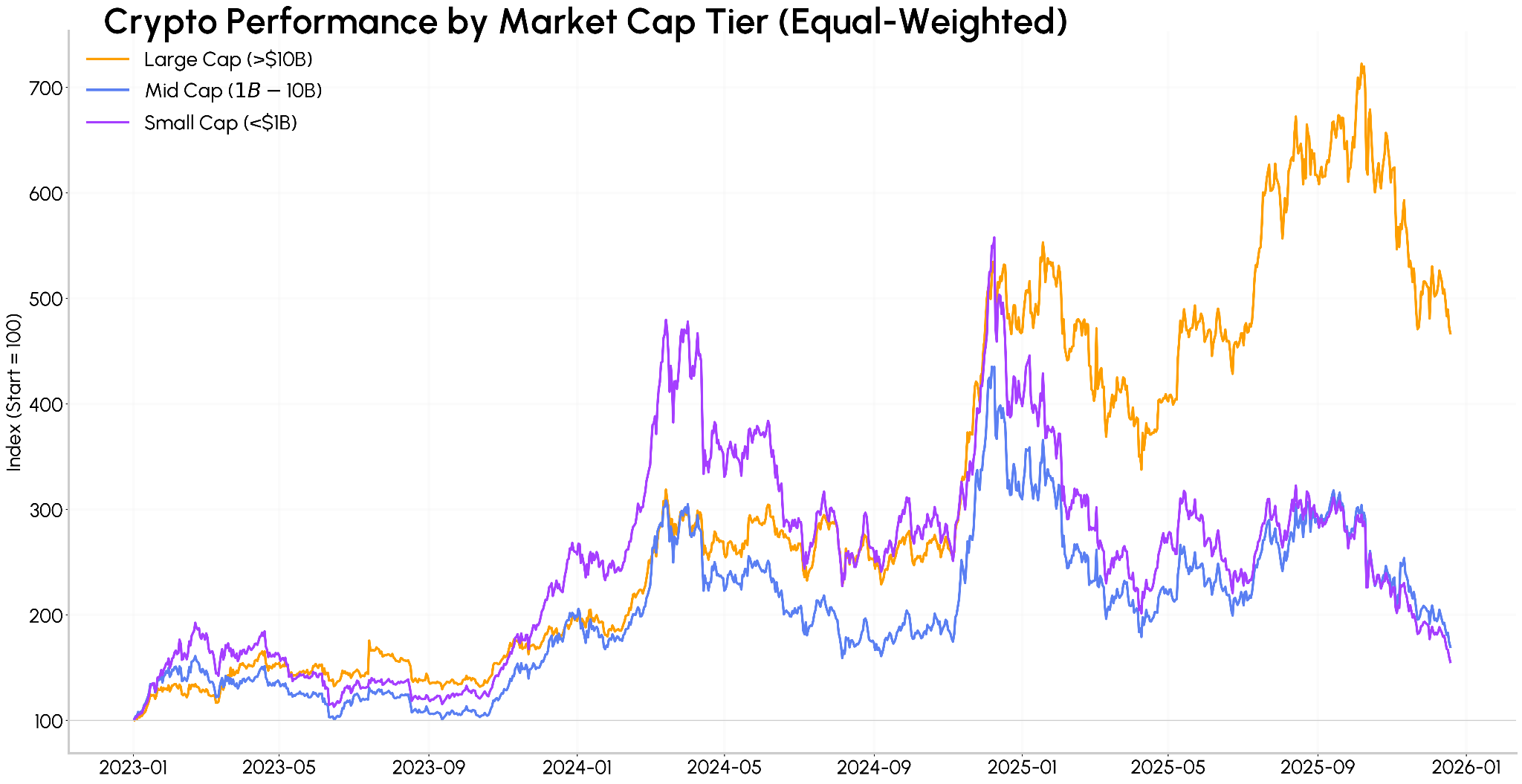

This concentration is also reflected in returns. Since 2023, mid ($1B-$10B) and especially small cap assets (<$1B) showed outperformance against large caps (>$10B market cap) during the early and late stages of 2024. However, this pattern reversed sharply in 2025 as sentiment around memecoins and other short-lived narrative rotations faded.

On an equal-weighted basis, large cap assets have returned ~365% since January 2023, while mid caps and small caps have returned ~70% and ~55% respectively, giving back much of their earlier gains. This divergence underscores how performance has increasingly tilted towards established, liquid assets, with gains in smaller tokens failing to sustain in the way previous cycles would suggest.

Source: Coin Metrics Prices & Network Data Pro

The October 10th liquidation event, driven by high leverage and thin liquidity, may reinforce this shift toward defensive positioning as investors increasingly favor more liquid assets over smaller ones prone to heightened volatility.

Conclusion

The data points to a market in flux, maturing and consolidating. While the crypto universe continues to expand in the number of assets and in its role as the substrate for a wider range of traditional assets, there is only so much liquidity to go around. At the same time, crypto is competing with strong narratives in equities and traditional hedges like gold for space in multi‑asset portfolios.

Capital has concentrated in large cap tokens and the infrastructure layer powering stablecoins, tokenized assets, and DeFi. Liquidity and scale matter more than they used to, and the bar for altcoins to attract sustained capital has risen considerably. That said, clearer market structure rules, the proliferation of altcoin and multi‑asset ETFs, and more favorable liquidity conditions could still catalyze another “altcoin season”, but one that is narrower and more selective than in past cycles.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

.jpg)

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.