Uniswap Flips the Fee Switch: From Governance Token to Value Accrual

State of the Network #346

Uniswap Flips the Fee Switch: From Governance Token to Value Accrual

Introduction

State of the Network #346

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- Uniswap’s fee switch links the UNI token to protocol usage through supply burns. Protocol fees now flow into UNI supply reduction, shifting UNI from governance-only to direct value accrual.

- Early data implies ~$26M annualized protocol fees and a ~207x revenue multiple. Ongoing burns of ~4M UNI per year embed high growth expectations into UNI’s $5.4B valuation.

- DeFi is shifting toward fee-linked token models. Burns, staker distributions, and ve-style locking are all attempts to better align tokenholders with protocol economics, shaping how the sector is valued.

Introduction

In late 2025, Uniswap governance approved the “UNIfication” proposal, turning on the long awaited protocol “fee switch”. This is one of the most consequential token‑economic changes among DeFi blue chips since 2020, arriving as markets are increasingly focused on real yield and sustainable, fee‑driven value accrual. The fee switch now creates a more direct link between the UNI token and the revenue and trading activity taking place on one of crypto’s largest decentralized exchanges.

In this issue of State of the Network, we break down Uniswap’s token economics after the implementation of its fee switch, assess burn and fee dynamics and valuation implications for UNI, and explore what this shift means for the DeFi sector.

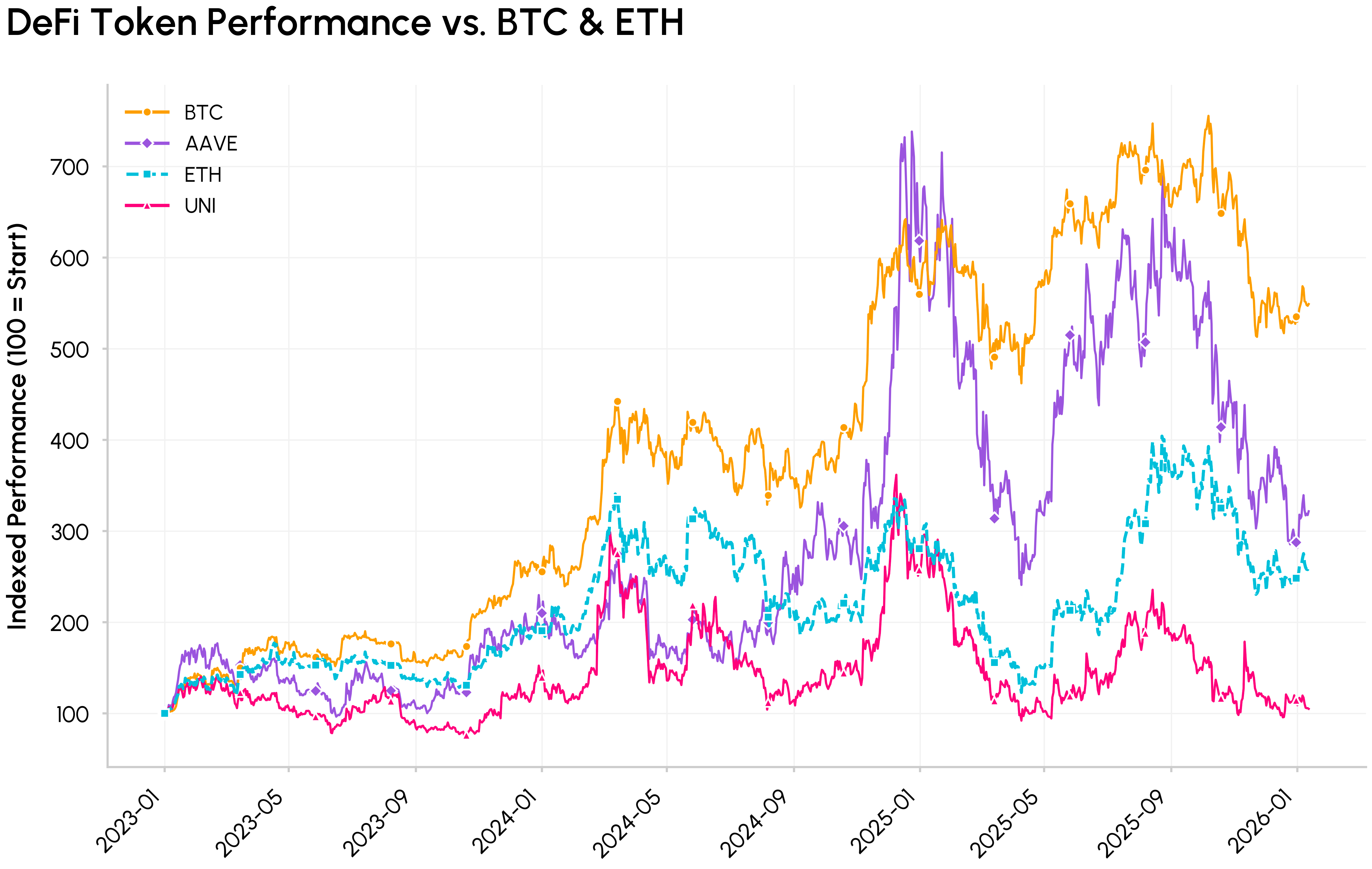

The DeFi Token & Protocol Value Disconnect

A core challenge in DeFi has been the gap between strong protocols and weak tokens. Many protocols have achieved clear product market fit, high usage and stable revenues, but their tokens often function mainly as governance, with little direct claim on cash flows. In that world, capital increasingly chases BTC, L1s, memecoins and other sectors, while many DeFi tokens trade apart from clear claims on protocol growth.

Uniswap launched as a decentralized exchange (DEX) on Ethereum in November 2018, designed to enable ERC‑20 swaps without order books or intermediaries. Soon after in 2020, UNI was launched as a governance token, mirroring a broader wave of DeFi blue chips (Aave, Compound, Curve and others) that issued tokens primarily as governance and incentive instruments.

Source: Coin Metrics Network Data Pro

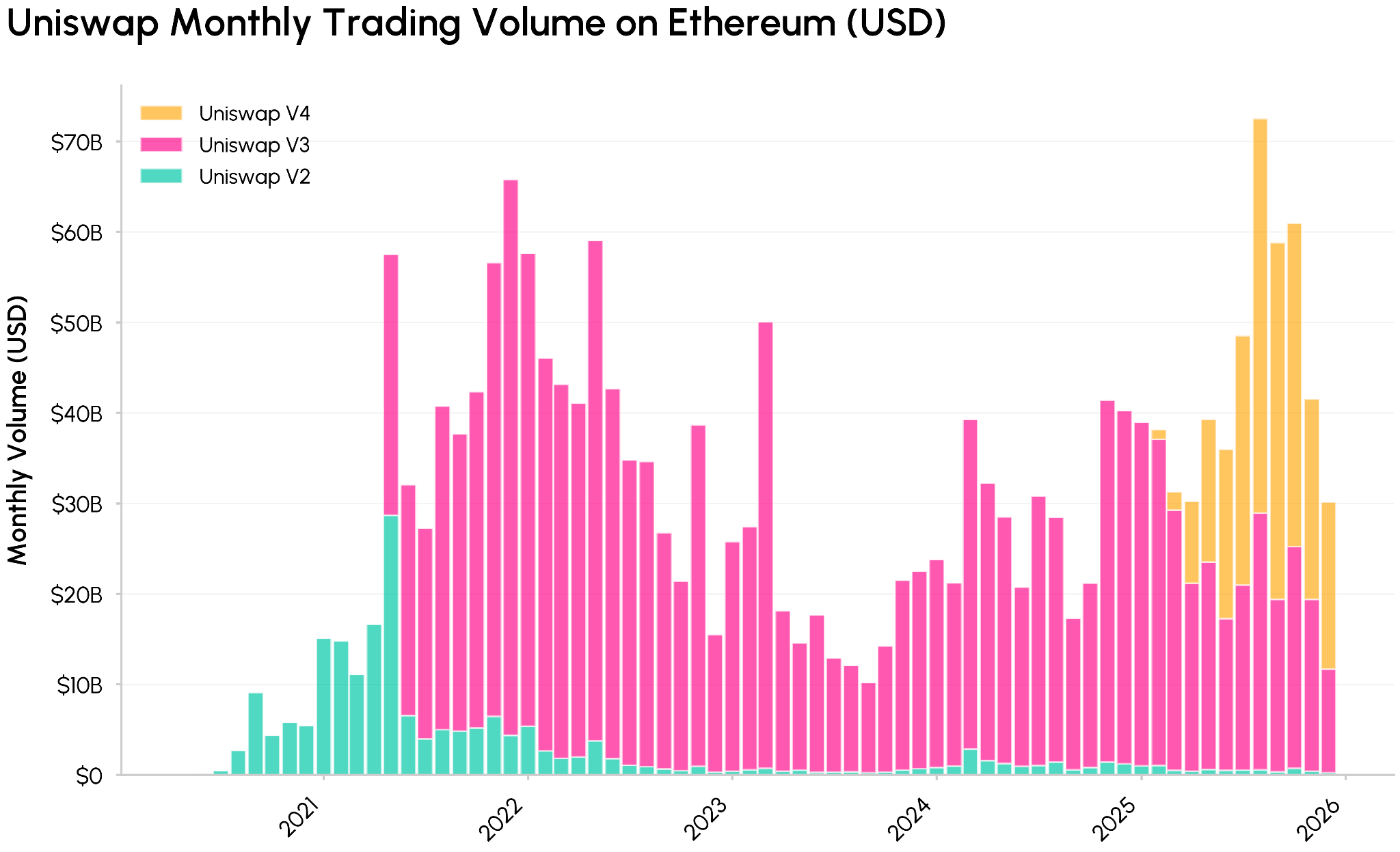

With new iterations, Uniswap became a core piece of on‑chain financial infrastructure, processing billions in volume and generating fees for its liquidity providers (LPs). Yet UNI, like most DeFi governance tokens, did not receive any direct share of protocol revenues, creating a growing disconnect between the scale of underlying cash flows and tokenholder economics.

Instead, value primarily accrued to liquidity providers (LPs), borrowers and lenders, or associated development teams, while tokenholders were left with governance rights and inflationary rewards. This tension between “governance only” tokens and value accrual set the stage for Uniswap’s fee switch and UNIfication proposal, which explicitly ties UNI’s value to protocol usage and better aligns tokenholders with the economics of the DEX.

Uniswap Fee Switch: Fee & Burn Mechanics

With the passing of UNIfication governance proposal, the protocol introduces the following changes:

- Activates protocol fees and UNI burns: Turns on the protocol “fee switch” and routes protocol‑level (v2 and v3 on Ethereum mainnet) pool fees into a UNI burn mechanism. Shifts UNI’s economic model from governance only to deflationary value accrual via a programmatic link between protocol usage and token supply.

- Executes a retroactive treasury burn: Conducts a one off retroactive burn of 100 million UNI from the treasury, backfilling years of missed fee capture for tokenholders.

- Pulls in Unichain revenue: Directs all Unichain sequencer fees, (after L1 data costs and a 15% share to Optimism), into the same burn‑driven value capture mechanism.

- Realigns organizational incentives: Folds most Foundation functions into Uniswap Labs and introduces a 20 million UNI per‑year growth budget, allowing Labs to focus on protocol adoption while reducing its take rate on the interface, wallet, and API to zero.

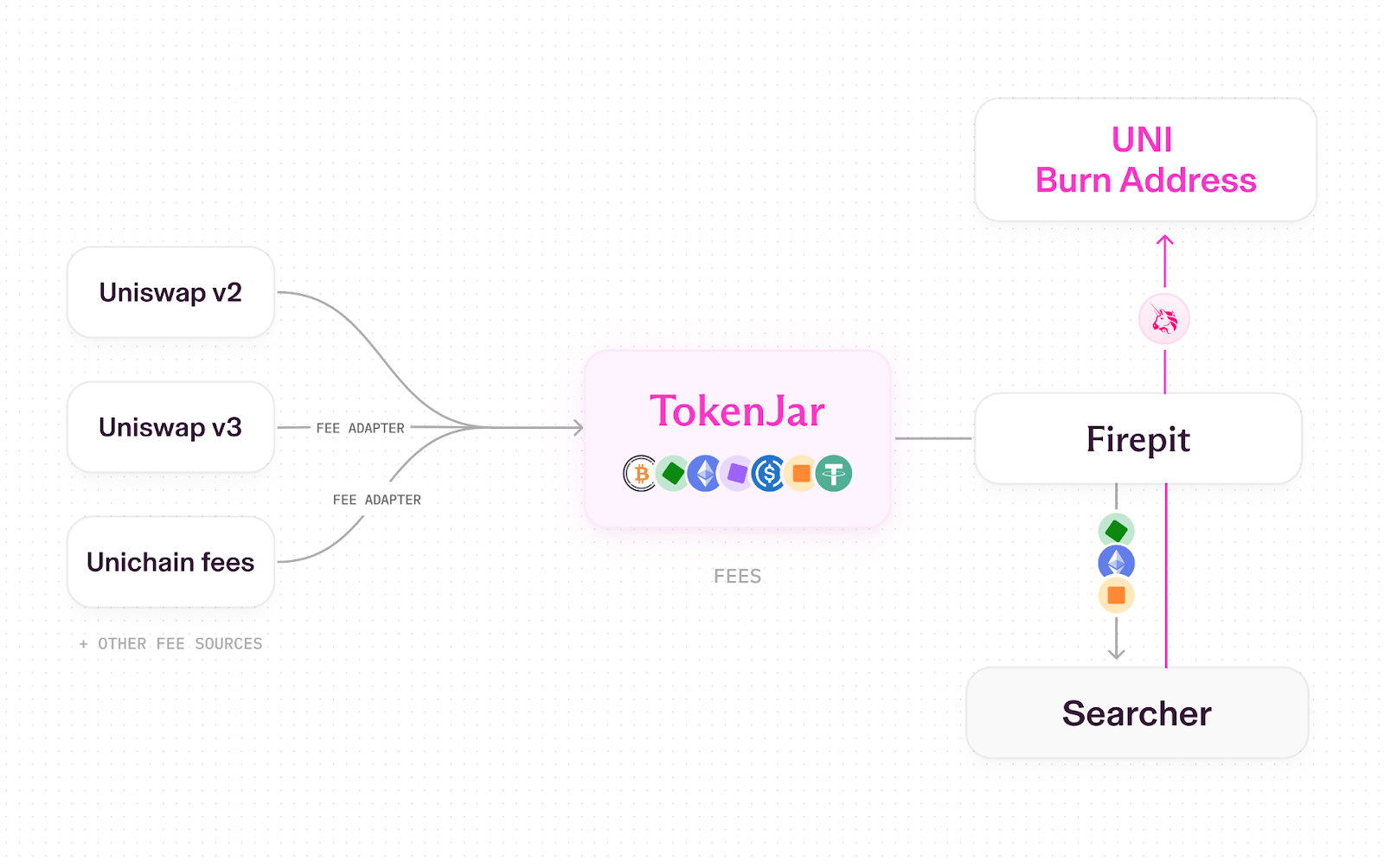

Uniswap now follows a “pipes” model with specialized smart contracts that handle how the assets are released or transformed (for example, burning UNI). Trades on v2, v3 and Unichain generate fees → a portion goes to the protocol (rest to LPs) → all protocol fees flow into a single vault smart contract called TokenJar on each chain → value can only leave TokenJar if UNI is burned via the Firepit smart contract.

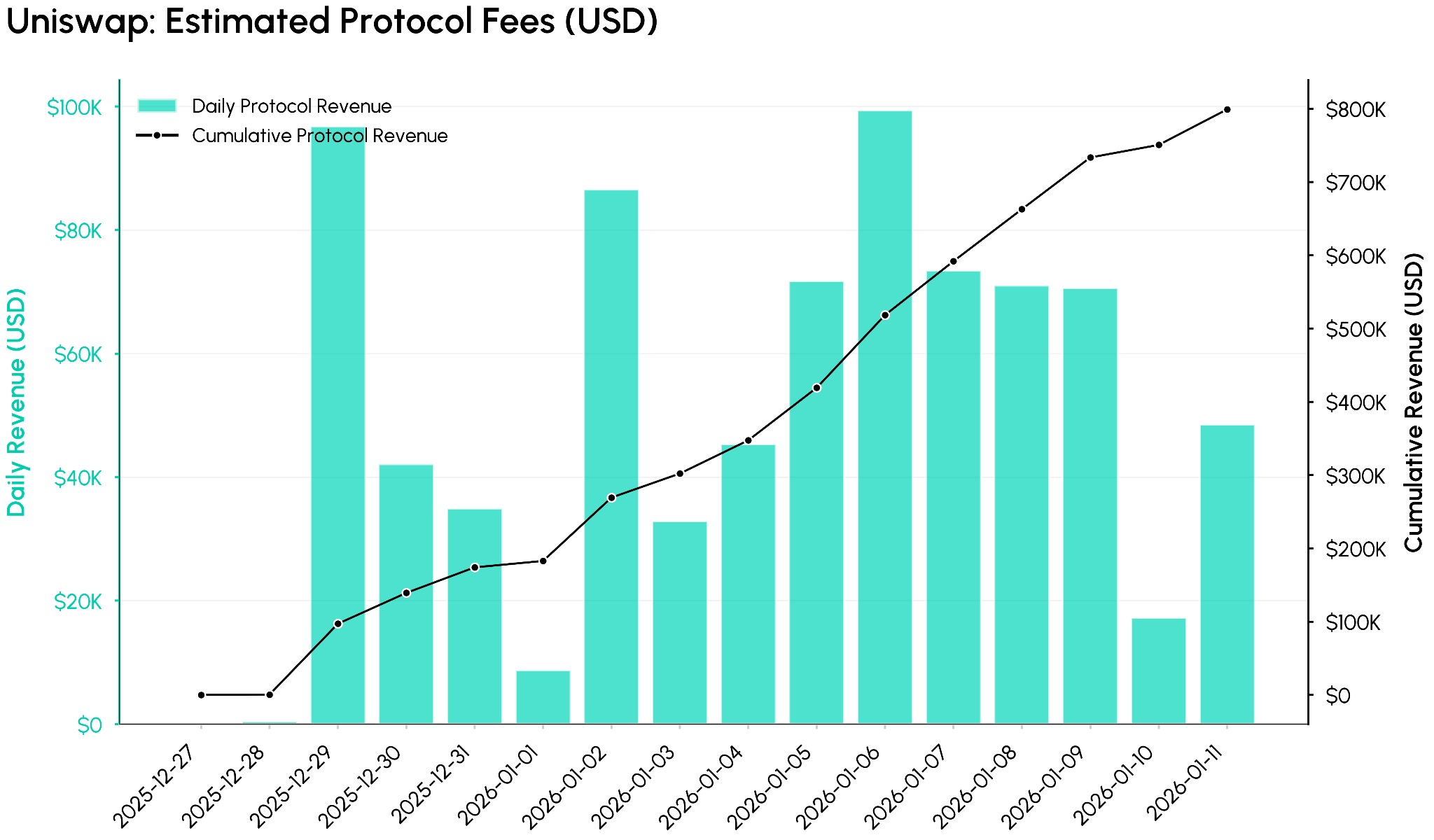

Using Coin Metrics ATLAS data, the first 12 days show a meaningful flow of protocol fees into the system. The chart below tracks estimated daily protocol fees (in USD) alongside the cumulative total, illustrating how quickly the fee switch begins to monetize Uniswap’s volumes in its initial configuration, with cumulative protocol‑level fees reaching roughly 0.8 million USD over this short window.

This implies an illustrative annualized protocol revenue run‑rate of around 26–27M USD if current conditions persisted, though actual outcomes will depend on market activity and the rollout of fees across pools and chains.

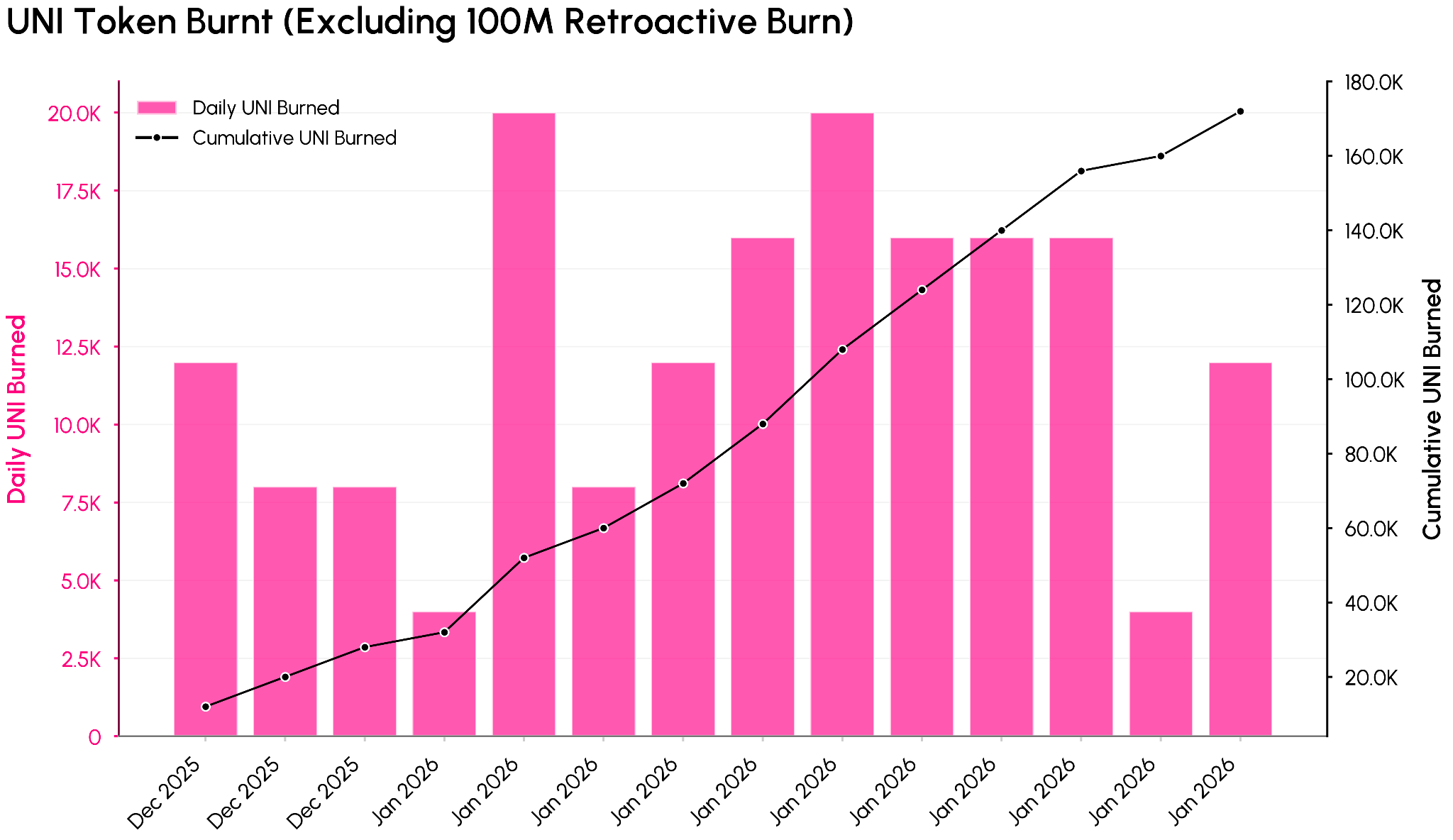

The burn chart above shows how those fees translate to UNI supply reduction (excluding the 100M retroactive burn). Total UNI burn has reached about 100.17M UNI (~557M USD), corresponding to a realized burn of roughly 10.1% of the original 1 billion UNI supply.

Based on the observed post‑UNIfication burns over the initial 12‑day period, ongoing burns correspond to an annualized rate of roughly 4–5M UNI per year, highlighting how protocol usage is now generating recurring, programmatic UNI destruction rather than purely inflationary issuance.

Valuation & DeFi Sector Implications

With the fee switch on, UNI can now be viewed through a cash‑flow based lens rather than only as a governance token. Comparing UNI’s market value of $5.4B to roughly $26M in annualized protocol fees implied by the first days of TokenJar data suggests a revenue multiple of roughly 207x, placing it closer to a high‑growth tech asset than a mature DEX. An annualized burn of roughly 4.4M UNI (ex‑treasury burn) equates to only ~0.4% of supply per year, giving a modest “burn rate” relative to that valuation.

Source: Coin Metrics Network Data Pro

This highlights a new tradeoff. UNI has become more investable as a result of more explicit value capture, but the current numbers imply a high rate for future growth. For that revenue multiple to compress, Uniswap likely needs a combination of higher fee capture (broader pool coverage, v4 hooks, fee discount auctions, Unichain), sustained volume growth, and deflation that offsets the 20M UNI per‑year growth budget and other emissions.

Structurally, UNIfication nudges DeFi toward a world where governance tokens are expected to have clearer links to protocol economics. Burns like Uniswap’s, direct fee distributions to stakers (e.g., Ethena), vote escrow locks that share fees and bribes (e.g., Aerodrome and other DEXs), and hybrids like Hyperliquid’s perp model are all versions of protocol‑fee sharing aimed at tightening that link. As the largest DEX adopts a fee‑linked, burn‑driven design, DeFi tokens are likely to be judged less on TVL or narrative alone and more on how efficiently each model converts protocol usage into durable value for holders.

Conclusion

Uniswap’s fee switch marks a turning point, moving UNI from a purely governance asset to one with a clearer link to protocol fees and usage. This makes UNI meaningfully more analyzable and investable on fundamentals, but it also puts its valuation under greater scrutiny, embedding strong expectations for future fee capture and growth.

From here, the key variables are how far Uniswap can expand protocol‑level fees without undermining LP economics or volumes, and how regulatory views on fee‑linked and buyback and burn token models evolve. Together, these factors are likely to shape UNI’s long‑term risk reward profile and how other DeFi protocols share value with holders.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.