Transaction Priority & Block Building on Ethereum

Introduction

State of the Network #356

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- Transactions can be affected by multiple external parties before being executed, creating opportunities known as Maximum Extractable Value (MEV).

- Block building is a competitive marketplace where transaction flow and transaction ordering are critical to gain and maintain market share.

- Transaction ordering is important for both traders and block builders to maximize their respective value.

Introduction

Transactions on public blockchains like Ethereum are arranged into blocks before being added to the chain by validators. Along this process, a transaction goes through several steps and parties before being confirmed, often sitting first in a public queue for pending transactions known as the mempool. Because of the public nature of the mempool, competing transactions and specialized bots can pay higher fees to be prioritized in a block. Based on these fees, block builders who construct the order of a block can capture Maximum Extractable Value (MEV) opportunities.

MEV is the additional value available when reordering, including, or excluding transactions from a block. It is similar to high-frequency traders benefiting from order flow information and adjusting their trades based on pending trades.

In this State of the Network, we highlight part of the transaction process: who builds blocks on Ethereum, how transactions can be ordered in a block, and some of the challenges when trading using the mempool systems.

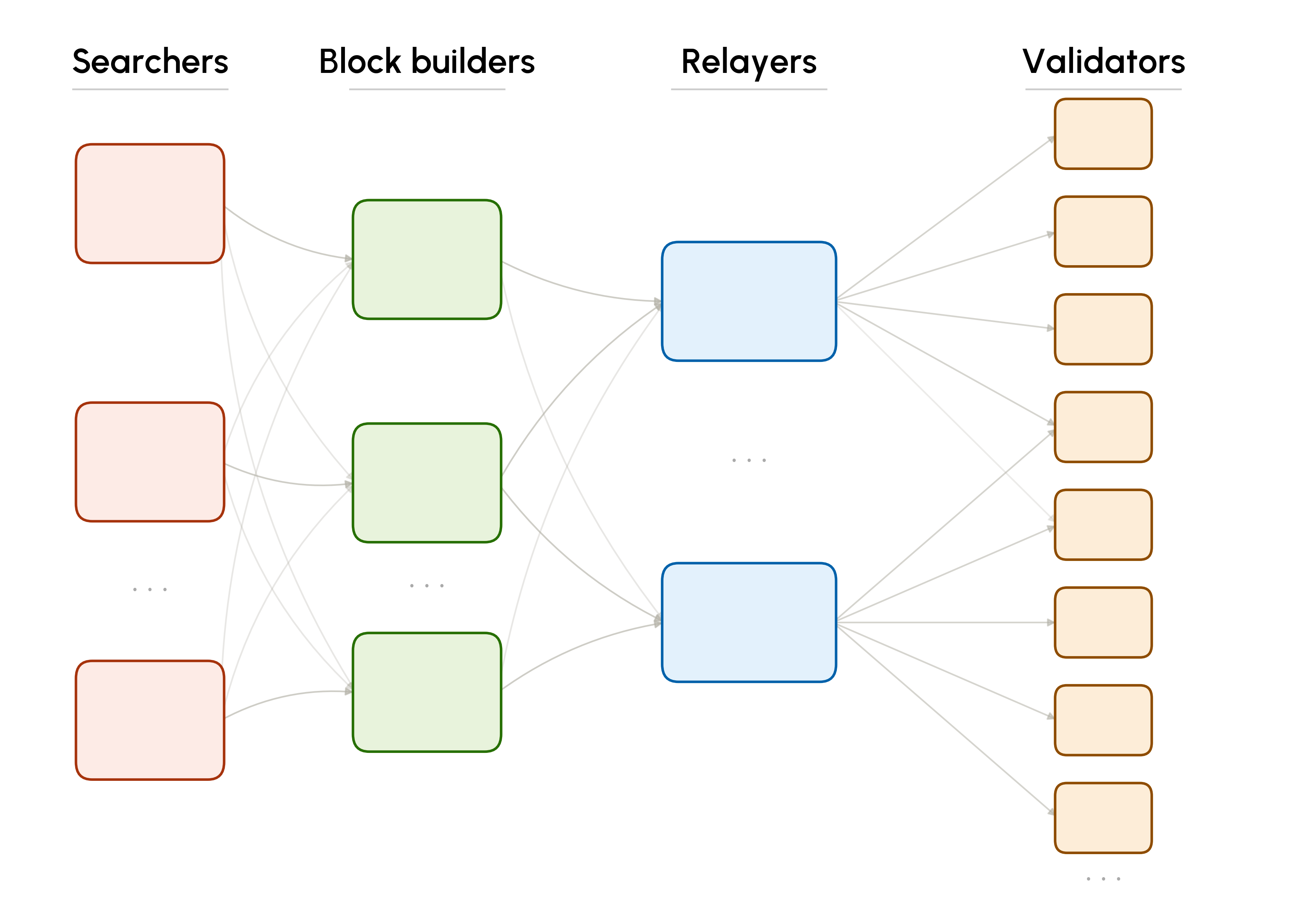

The MEV Supply Chain

Here, we highlight key intermediaries who affect the transaction lifecycle and how they contribute to generating MEV opportunities.

The Maximum Extractable Value (MEV) chain begins with searchers. Searchers scan DeFi protocols and public transactions to find profitable MEV opportunities. Not all MEV is malicious – MEV can be arbitrage bots ensuring tight trading spreads and ensuring assets maintain their peg, while others execute more harmful strategies such as sandwiching user trades on decentralized exchanges (DEXs). Searchers combine the original transaction with their own transaction into a “bundle” and send it to block builders so it executes in a specific sequence.

Block builders aggregate transactions from the public mempool, private order flow, and searcher bundles to put into a block. Block builders may not all receive the same MEV bundle, therefore blocks differ in total fees paid and transactions included. This changes how much block builders can bid in the auction for their block to be added to the chain. Builders submit bids to relayers who coordinate bids with validators. Builders pay a part of the block’s value to these participants in exchange for having their block included.

Validators or block proposers act as the final selector of whose block to include. In each slot, a validator is selected as the proposer and decides which block to add to the blockchain, typically selecting the highest value bid from builders. Rotation prevents a small number of validators from controlling too much network activity. Having too few validators proposing blocks increases the risk of transaction censorship. On the other hand, too many validators proposing blocks can put stress on network connectivity and overall performance.

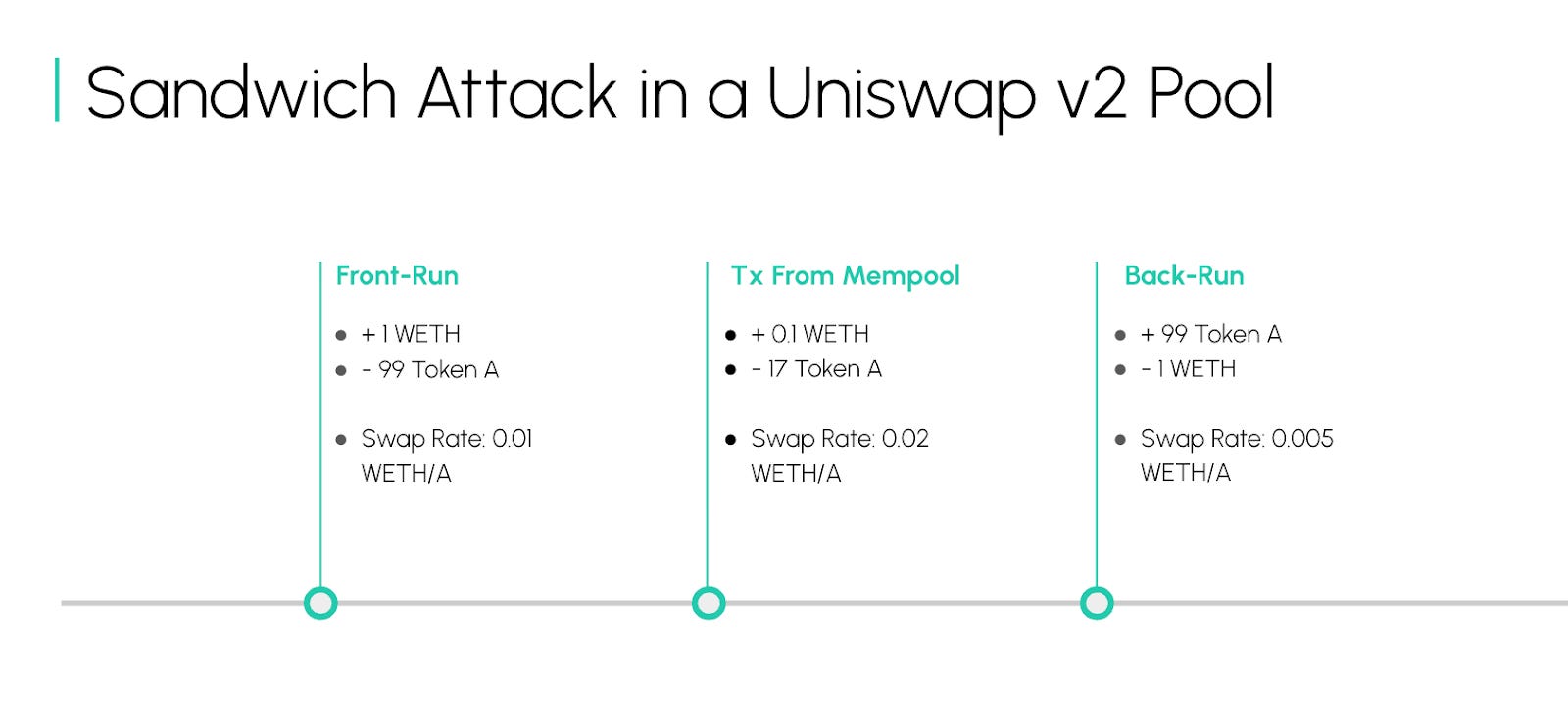

MEV Sandwich Example:

Below, we walk through an illustrative example of MEV known as a sandwich. A sandwich is where the user’s target transaction is executed between a malicious front-run and back-run transaction. A bot augments the protocol to negatively impact the target transaction’s activity with the front-run. Typically, the bot does not want to hold the affected tokens after the attack, thus back-running and receiving a better trade price. This profit is usually captured in the spread between rates during the front and back-run.

In block #24,650,612 on Ethereum, a transaction is front-run then back-run, creating a sandwich that leaves the MEV bot with a profit from the pair of transactions and the original user facing adverse swap prices.

The user sends their request to Swap WETH to Token A to the mempool for 10 seconds, waiting to be added to a block. A searcher sees the opportunity routing to the Uniswap V2 Pool and can influence the liquidity available to change the swap rate the user receives. They create a front-run transaction that does the same thing as the user, swapping WETH for A, only it is a greater magnitude than the original swap.

The front-run executes first, the target transaction pays more WETH for less A tokens due to an imbalance in pool assets. Now that there is more WETH in the pool than Token A, the next swap can receive more WETH when depositing Token A, so the bot sends a back-run transaction to deposit its Token A and get back the WETH.

A block builder executes these transactions in the searcher’s desired order because of the searcher’s higher priority fees. The priority fees add value to the block, increasing the total bid a block builder can submit and probability of the builder’s block being selected by a validator.

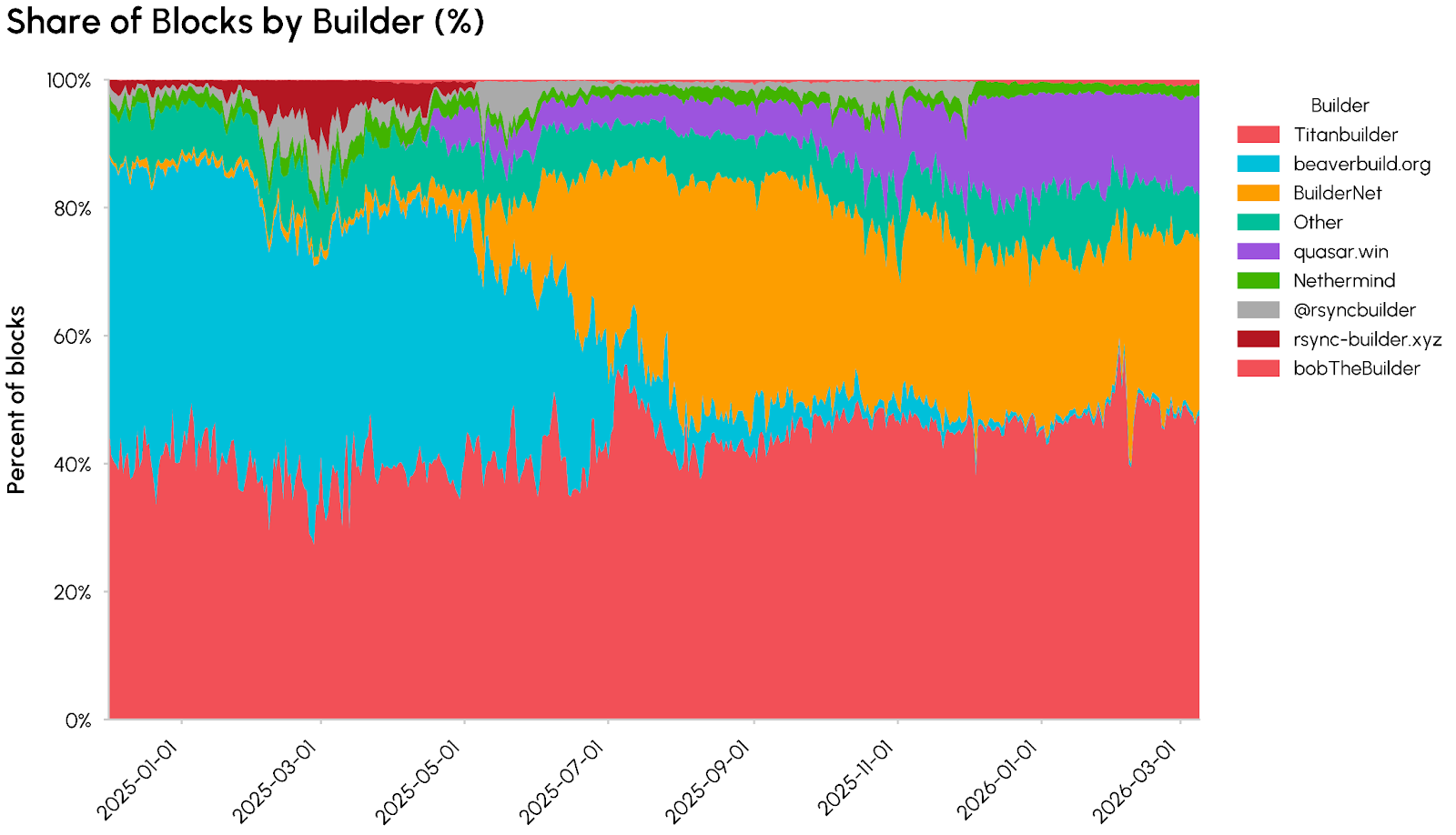

Who are the Block Builders?

Block building on Ethereum follows a model known as Proposer-Builder Separation (PBS), where builders use the 12-second block time to optimize transaction ordering in a block to extract value through transaction fees. An auction occurs every 12 seconds where block builders bid a portion of the block value to give to the lead validator. The highest bid is accepted, the lead validator publishes the block received from the block builder, and the block builder receives the remaining fees from the block.

Block building today is a highly centralized activity and risks a minority group controlling transaction ordering. The two builders with the most market share are Titan Builder (47.6%) and BuilderNet (26.0%). BuilderNet attempts to decentralize block building by sharing the transactions it ingests with a group of underlying builders. Instead of competing for transaction flow, BuilderNet works to improve the algorithms underlying transaction ordering to provide a neutral-execution environment.

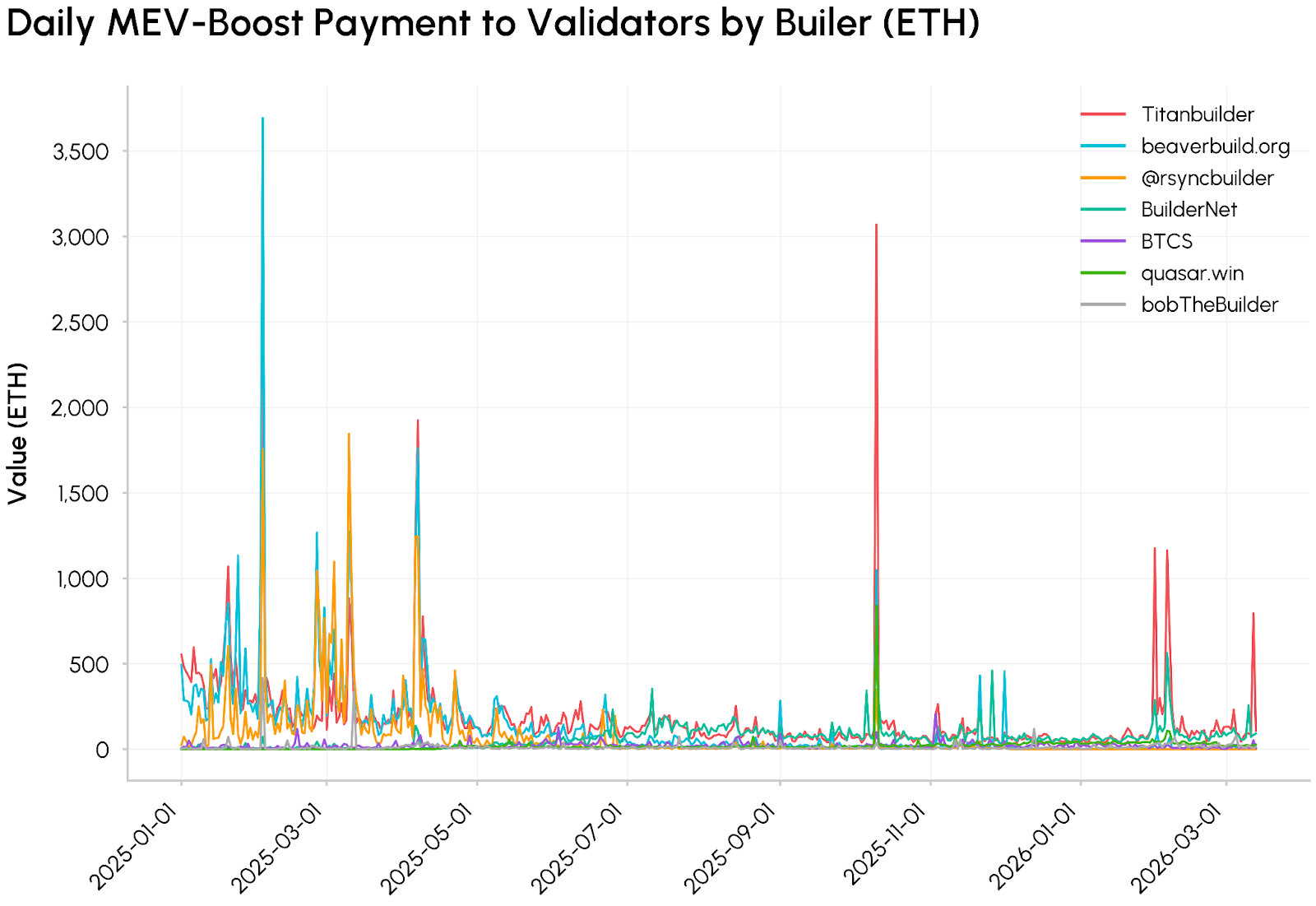

How Much Value Do Block Builders Pay To Validators?

The value in a block is important to a builder’s auction bids. If they have access to more valuable transactions to order in a block, they can place higher bids for validators to select their block. This creates a flywheel: as the builder continues to win block auctions, more users will want to send their transactions to that block builder directly, further centralizing who determines which transactions are included and excluded from a block.

Source: Talos, mevboost-data (Data Always, Github)

The auction is conducted through MEV-Boost, a sidecar where relayers share block bids to validators and validators receive the block of the winning bid to propagate to the network.

Beaverbuild and Titanbuilder were previously the two largest Ethereum block builders. They had the most valuable order flow, thus they were able to bid more ETH to validators to win block auctions. The drawdown in Beaverbuild MEV-Boost value highlights Beaverbuild partnering with BuilderNet to share transaction flow across block builders.

The overall drawdown in daily value captured by validators is a result of network improvements. Only BuilderNet and Titanbuilder have had a day over 500 ETH in MEV-Boost Value in 2026. Research continues to promote sending transactions privately or skipping the mempool to prevent malicious MEV opportunities. Adoption of Layer-2s and competing networks fighting for market share also affects the number of transactions on Ethereum.

How Incentives Affect Block Packaging

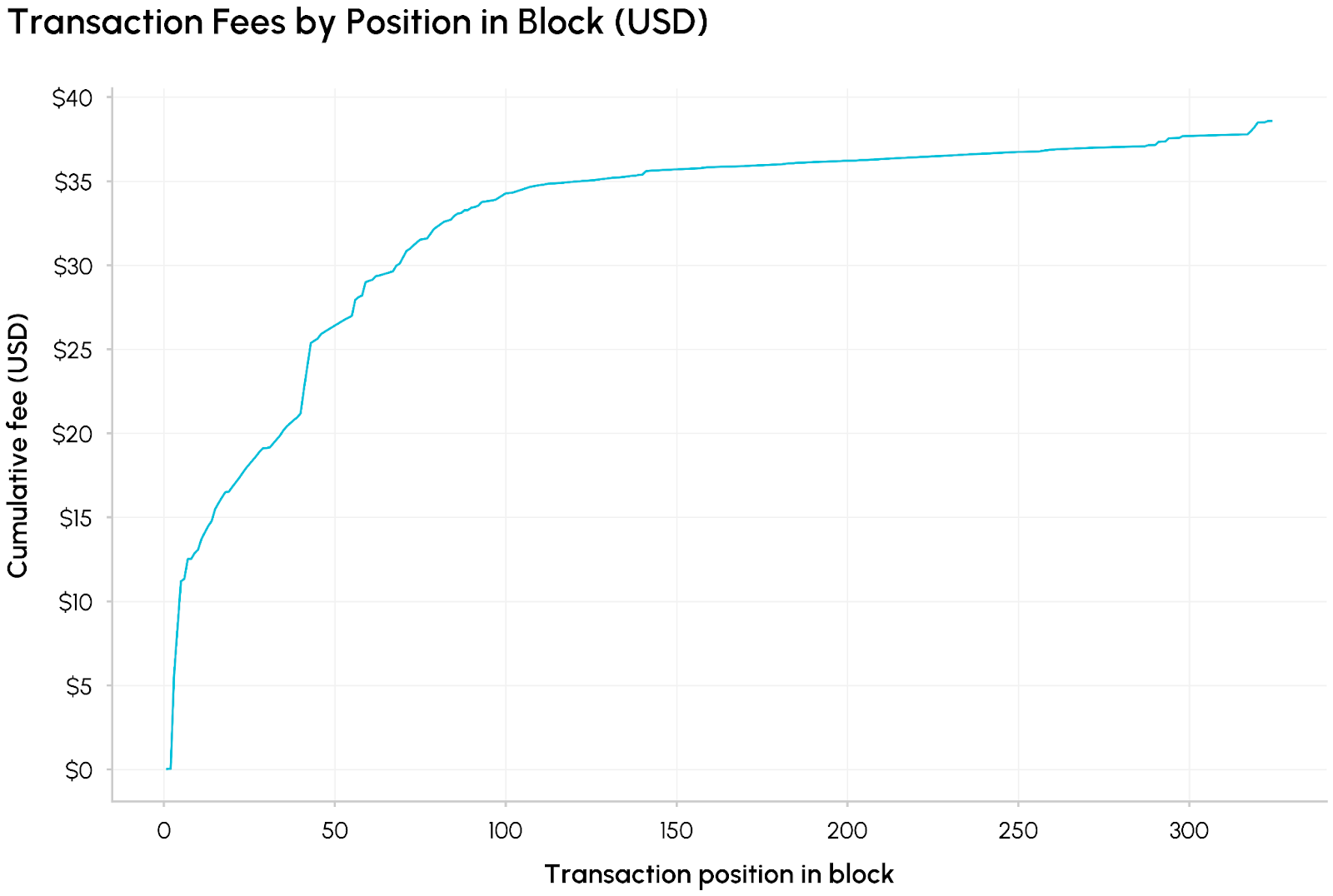

The ordering of transactions in a block not only affects their order of execution, but also the value of the block. Transaction ordering depends on the block builder’s algorithm packing blocks based on network fee, priority fee, size, and value to other participants. In block #24,120,201, more than half of the value in the block – total network and priority fees – is in the first 44 transactions of the block.

A majority of this block’s value is in the first 12.5% of transactions, which illustrates how block builders are incentivized to pack as many valuable transactions in its block to win the auction. As they continue to add transactions to a block, the builder then becomes limited by computational limits and order flow.

Conclusion

Ethereum has a unique process for executing transactions. The target 12 seconds per block allows block builders time to build an optimal block and place bids to validators while also allowing searchers time to scan for MEV opportunities to capture additional value.

Block builders are incentivized to include MEV because it increases the value of the block. Order flow, Ethereum’s size and computational limits, and speed of sending bids all limit the block builder’s ability to execute transactions in their preferred order and control part of the transaction supply chain.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.