On-chain Vaults: Mechanics, Landscape and Risk

Introduction

State of the Network #359

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways

- Vaults are non‑custodial smart contracts that pool deposits into yield‑generating strategies, offering a transparent and composable alternative to traditional funds and structured products.

- Vaults have grown into core onchain infrastructure, underpinned by the ERC‑4626 vault standard and modular lending protocols as stablecoins, tokenized RWAs, and yield‑bearing assets have expanded.

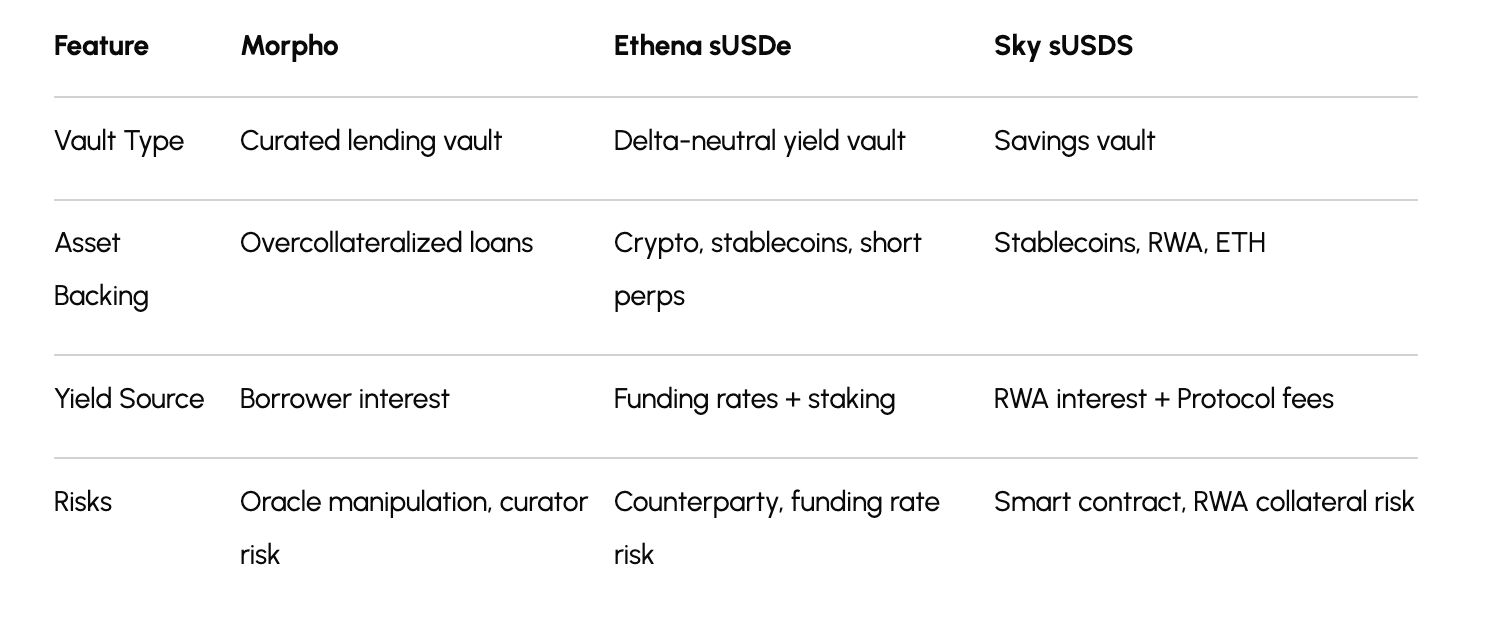

- Morpho, Sky’s sUSDS, and Ethena’s sUSDe highlight how vaults span savings products, delta‑neutral strategies, and curated lending, each with its own yield sources and risk profile.

- Vault curation is emerging as a specialized function, with firms managing billions in assets and actively shaping collateral, liquidity, and oracle risk across vaults.

Introduction

Vaults have emerged as a core primitive in the onchain ecosystem, aggregating capital into yield generating strategies with exposure to lending markets, staking protocols or tokenized real world assets (RWAs). Like professionally managed investment funds or structured products, vaults pool capital into predefined portfolios targeting different risk profiles, but operate with greater transparency, composability and capital efficiency.

As the pool of productive assets expands onchain, from stablecoins, to yield-bearing tokens and RWAs, vaults have become the natural aggregation layer for this capital. Adoption is accelerating, with asset managers like Bitwise joining vault curation, Kraken embedding vault strategies into its “DeFi Earn” product, while protocols like Morpho, Spark, and Aave are evolving the underlying infrastructure. At the same time, vaults are not without tradeoffs, making risk management and curator design crucial to the growth of the vertical.

In this issue of State of the Network, we provide an overview of onchain vaults, the ERC-4626 token standard that underpins them, and understand the role of protocols, markets and risk curators. We also highlight the risk dimensions of vault curation and how they shape the emerging vault landscape.

What are Vaults?

At their core, vaults are non-custodial smart contracts that aggregate capital and execute yield-generating strategies, automating what would otherwise require active monitoring and management of assets across protocols. Depending on how they are structured, vaults can supply assets into lending markets, facilitate delta-neutral strategies, stake/restake assets to earn validator rewards, or allocate to tokenized instruments for off-chain returns.

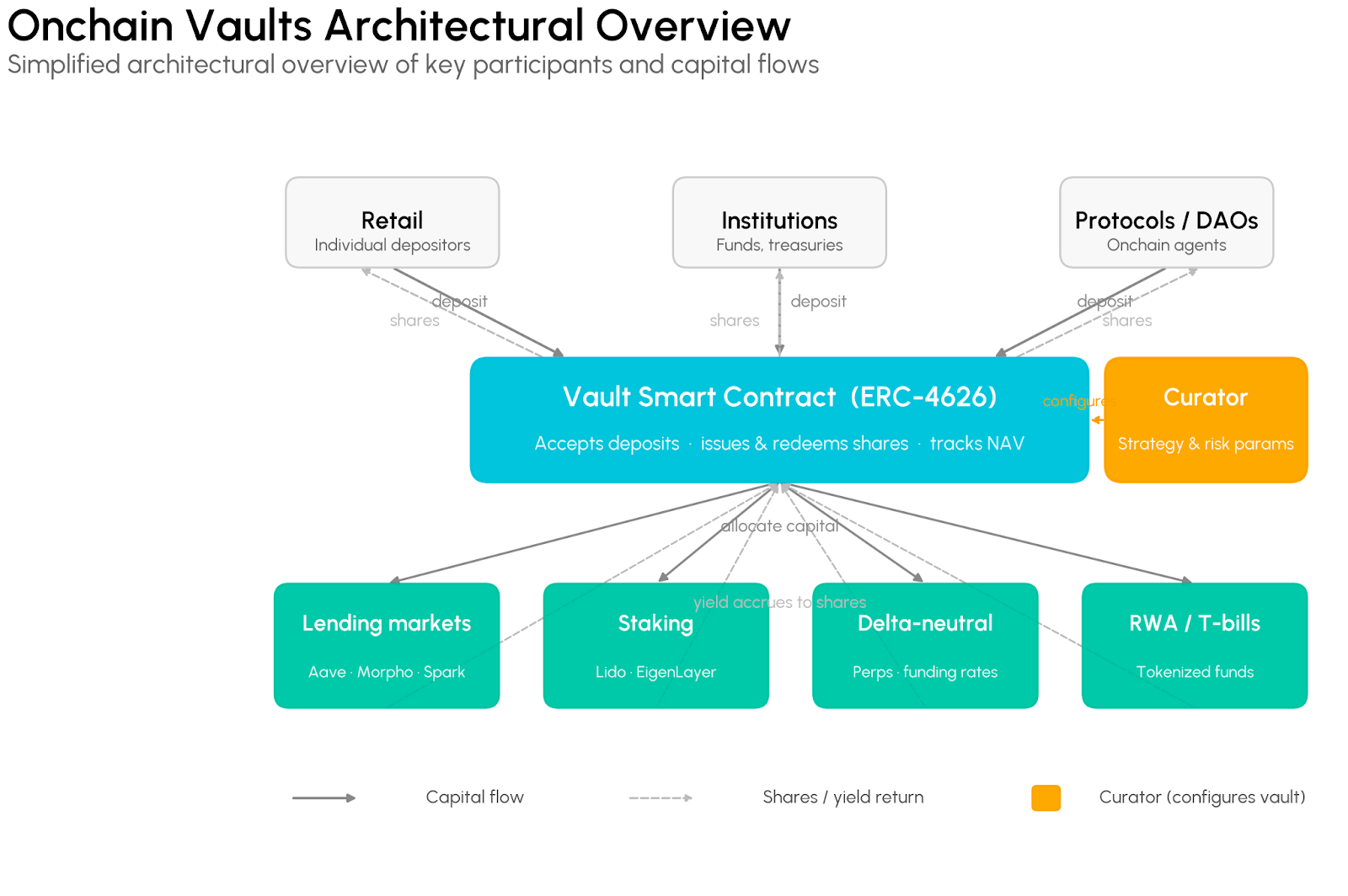

The diagram below is a simplified illustration of the key participants and capital flows in a typical vault structure, from depositors and curators to the underlying markets where yield is generated.

At the center is the vault smart contract (ERC-4626), which handles deposit intake, share issuance, and accounting. Curators or strategy managers configure the vault’s risk parameters and allocation logic, while capital is deployed into underlying markets. Depositors interact with a single interface regardless of the complexity of the underlying strategy, made possible by a shared technical standard that underpins most vaults in the ecosystem today.

ERC-4626: A Common Interface for Vaults

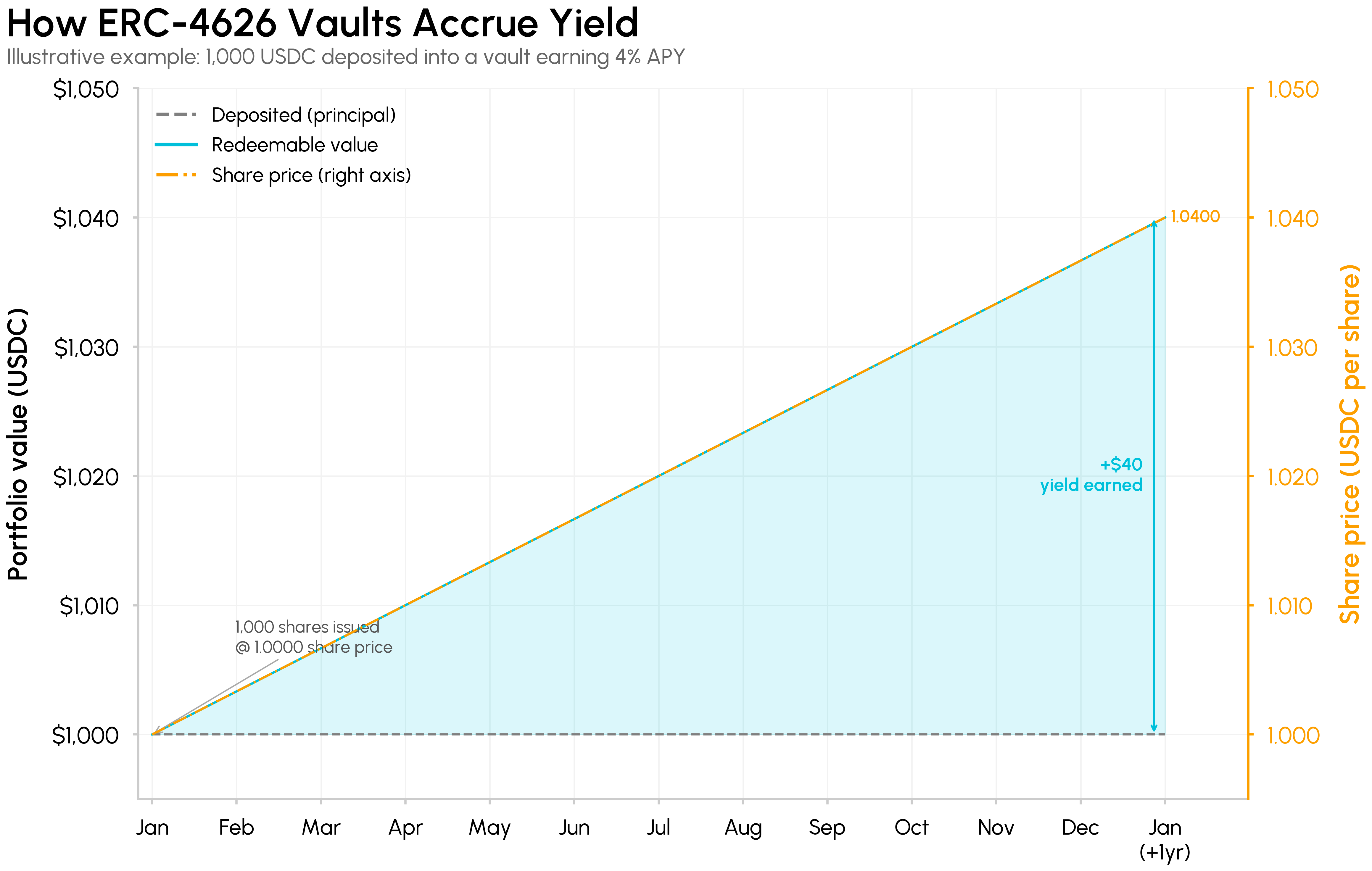

In 2022, a tokenized vault standard called ERC-4626 was introduced as an extension to the ERC-20 token standard. This provided a uniform interface for deposits, withdrawals, share issuance and accounting, eliminating the need for custom implementations. Today, it underpins the functionality of vaults across lending markets, savings products and interest bearing tokens.

In exchange for assets deposited into an ERC-4626 vault (eg., USDC, WETH), users receive shares representing their proportional claim on the vault’s underlying assets. These shares can be redeemed to withdraw the assets plus any yield earned. The number of shares received depends on the amount deposited and the current exchange rate (the ratio of total assets to total shares outstanding).

As the vault generates yield, the asset balance grows while shares remain fixed, causing the exchange rate to appreciate. Each share becomes redeemable for progressively more of the underlying asset over time. Illustrating a simple example:

- 1,000 USDC deposited into a USDC vault

- Exchange rate at deposit: 1.0 (user receives 1,000 shares)

- After one year at 4% APY, exchange rate appreciates to 1.04

- 1,000 shares redeemed for 1,040 USDC

Vault Market Landscape

Interest Bearing Stablecoins

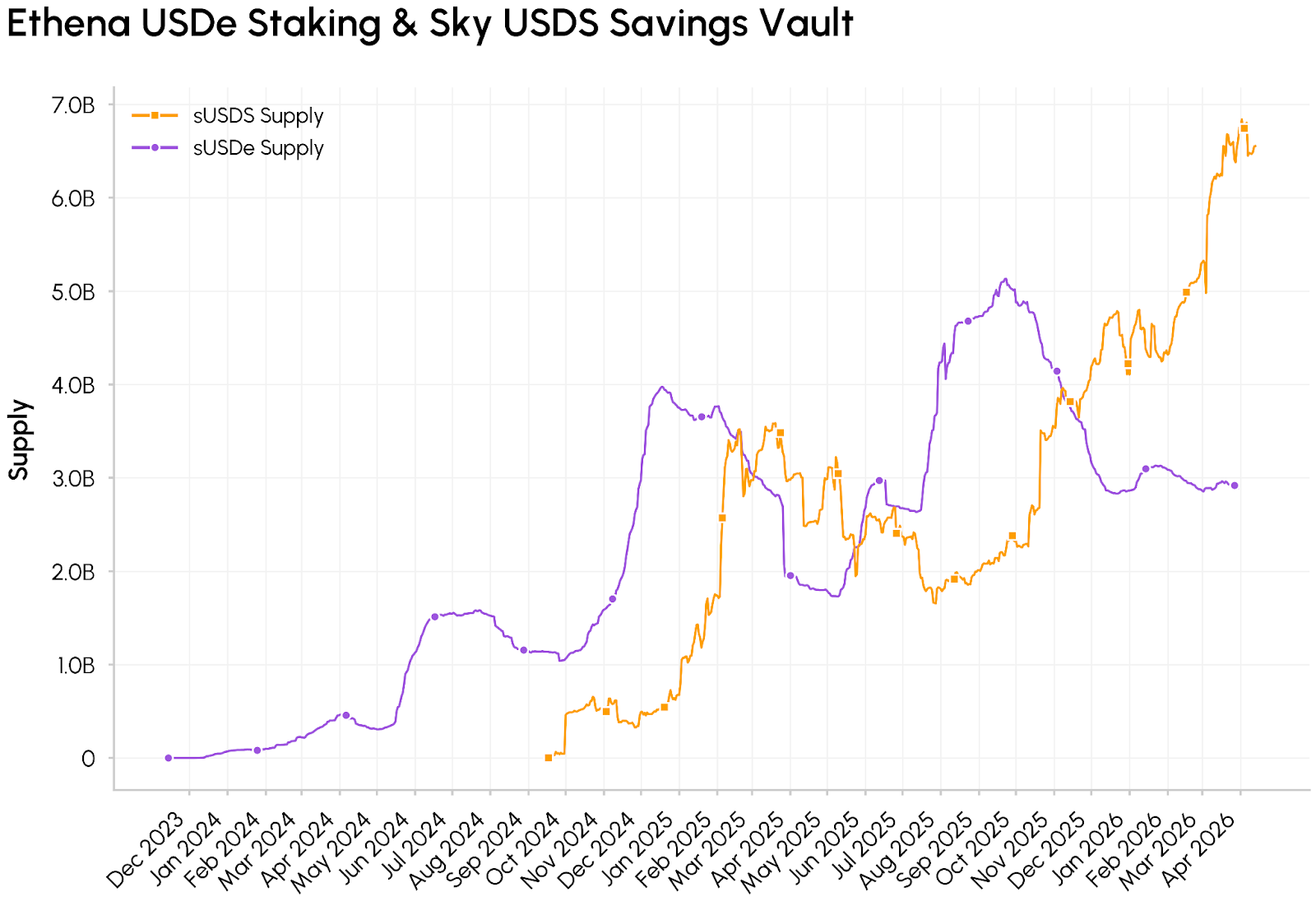

The most widely adopted vault products today are yield bearing stablecoins, tokens that accrue interest passively through the ERC-4626 share mechanism. Sky’s Savings USDS (sUSDS) and Ethena’s staked USDe (sUSDe), are the two biggest examples, with combined supply exceeding $9.4B.

sUSDS functions as Sky’s savings vault, with Spark protocol allocating USDS into RWA instruments, stablecoins like USDC, onchain and OTC lending markets to provide a stable savings rate. It functions as the onchain equivalent of a money market fund. Ethena’s sUSDe takes a different approach, capturing funding rates through delta-neutral hedging across crypto and increasingly RWAs. Both tokens appreciate in value against their underlying asset over time through the ERC-4626 exchange rate mechanism described above.

Their supply trajectories reflect the difference in their strategies. sUSDS has grown steadily as a result of a diverse basket of underlying yield including RWAs, while sUSDe has been more sensitive to funding rate regimes and broader crypto market conditions. As a result, Ethena is actively expanding collateral backing towards: overcollateralized institutional lending, liquid RWAs and non-crypto futures exposure.

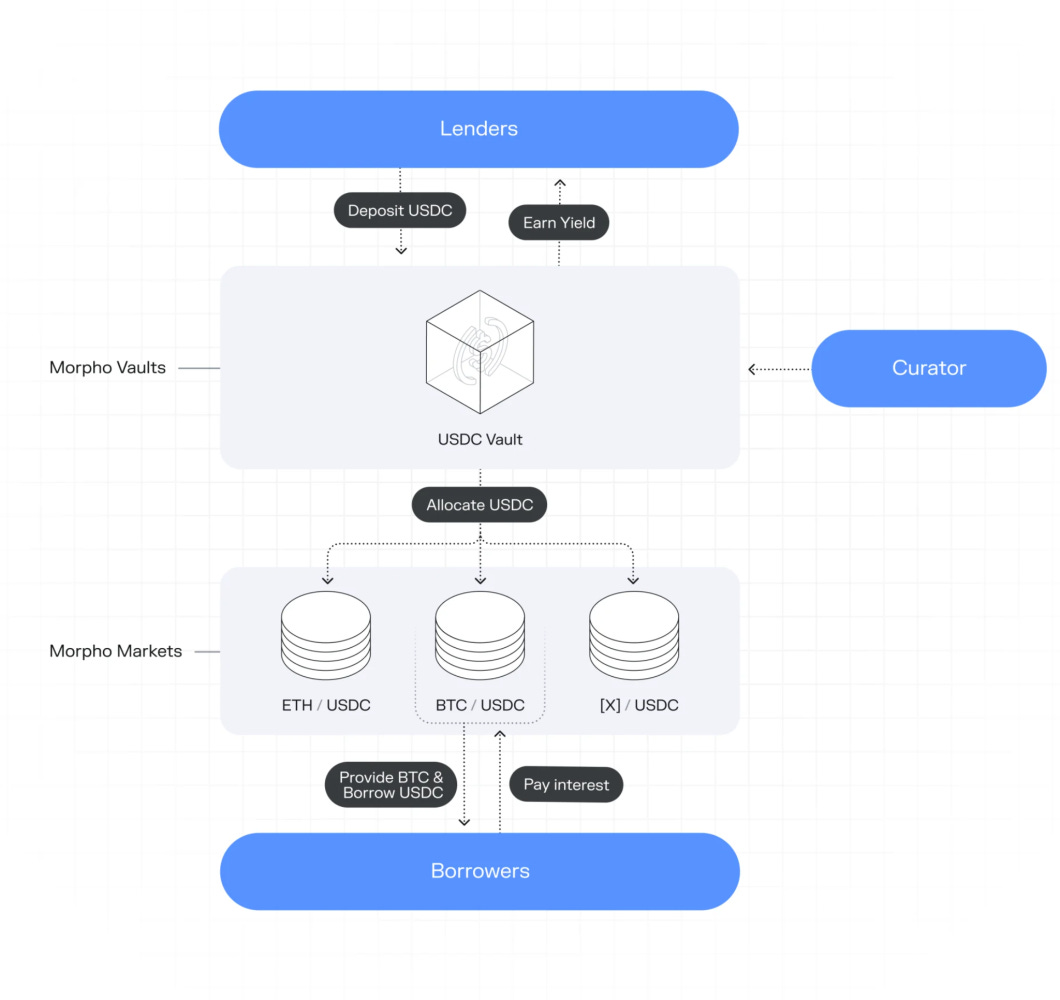

Curated Lending Markets

While yield-bearing stablecoins embed a fixed strategy into the vault itself, protocols like Morpho separate the vault layer from the strategy or curation layer entirely. Morpho Vaults are ERC-4626 compliant lending vaults where independent curators such as Gauntlet, Steakhouse Financial, or Bitwise define risk parameters, collateral eligibility, and allocation limits. Depositors supply a single asset (e.g. USDC) and earn borrower interest as curators allocate that capital across lending markets like BTC/USDC, WETH/USDC, and others.

This modular infrastructure is increasingly powering products built on top of vault rails. Coinbase leverages Morpho to offer BTC-backed loans directly within its consumer app, Kraken embeds vault strategies into its DeFi Earn product, and Bitwise became one of the first traditional asset managers to enter vault curation on Morpho with a non-custodial USDC vault.

Comparison Table of Vault Examples

Beyond Morpho which is the largest in the category with $11.5B in deposits, Spark underpins Sky’s sUSDS as its primary lending and allocation layer, while Aave v4 moves from unified liquidity pools toward isolated, vault-based markets with modular risk parameters.

Vault Curation and Risk Management

Vault curators sit between infrastructure and depositors, performing a crucial role similar to fund or risk managers in traditional finance. Yet the risks they manage are fundamentally different given the non‑custodial, composable, 24/7 nature of onchain markets. Curators determine approved collateral, loan‑to‑value (LTV) ratios, allocation caps, liquidation thresholds, and parameters such as oracle configurations.

This function is increasingly handled by specialized teams like Steakhouse Financial, Gauntlet, and other third‑party curators. They now oversee billions of dollars in assets across lending vaults, focusing on stablecoins, blue‑chip crypto collateral, RWAs, and other strategies across the risk/return spectrum. Key risk dimensions for curators include:

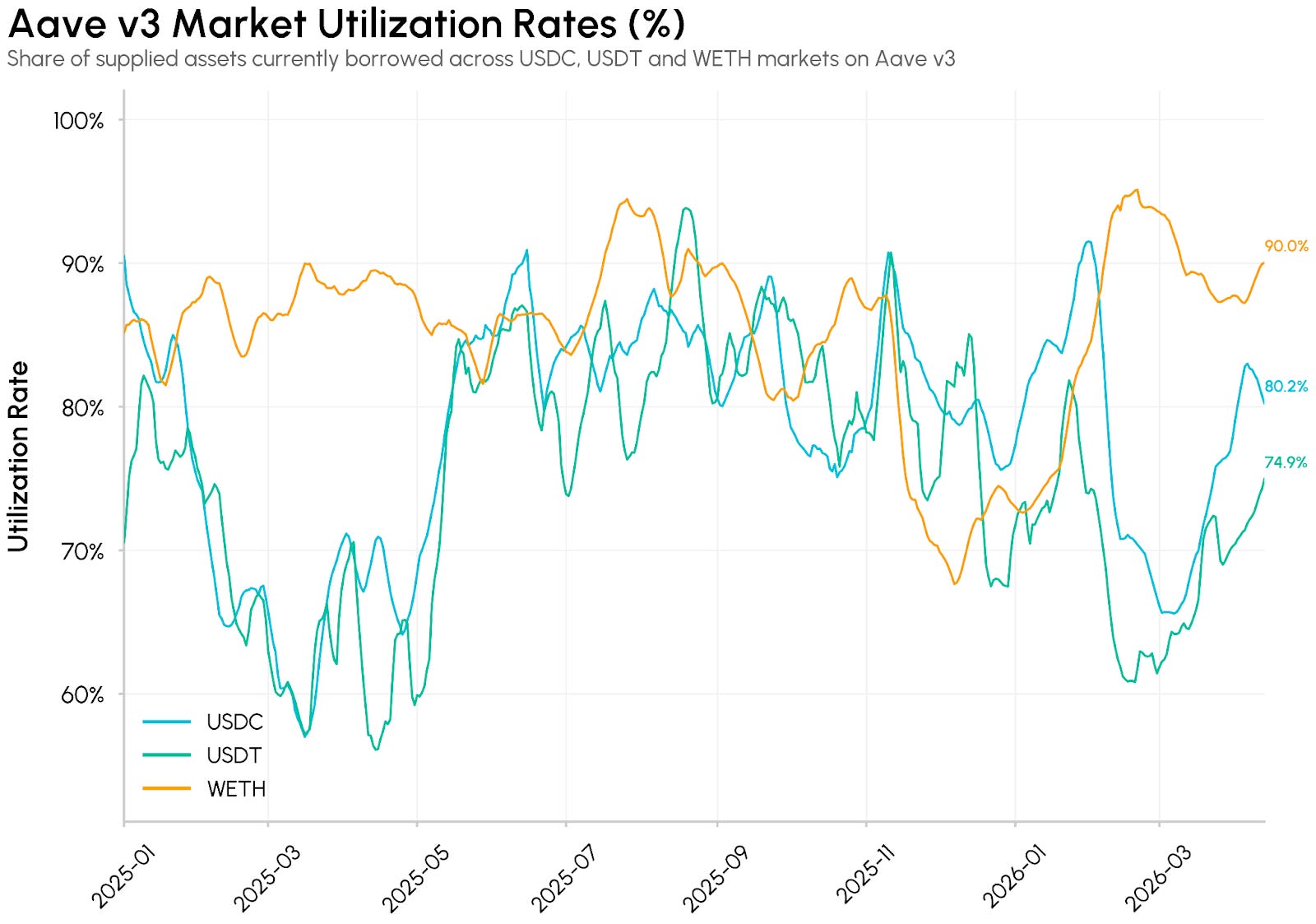

- Liquidity risk: the risk that depositors cannot exit a vault when needed.

In lending markets, this can occur when borrowing demand outpaces available supply, leaving insufficient liquidity for withdrawals. Curators typically adjust supply caps or reallocate capital, with utilization rate and pool depth as critical inputs. The chart below shows utilization across key Aave v3 markets, with the WETH market at 90% utilization. While Aave uses a different model, it serves as a direct benchmark for liquidity and leverage conditions curators navigate.

- Collateral risk: the risk of bad debt from low-quality or illiquid collateral.

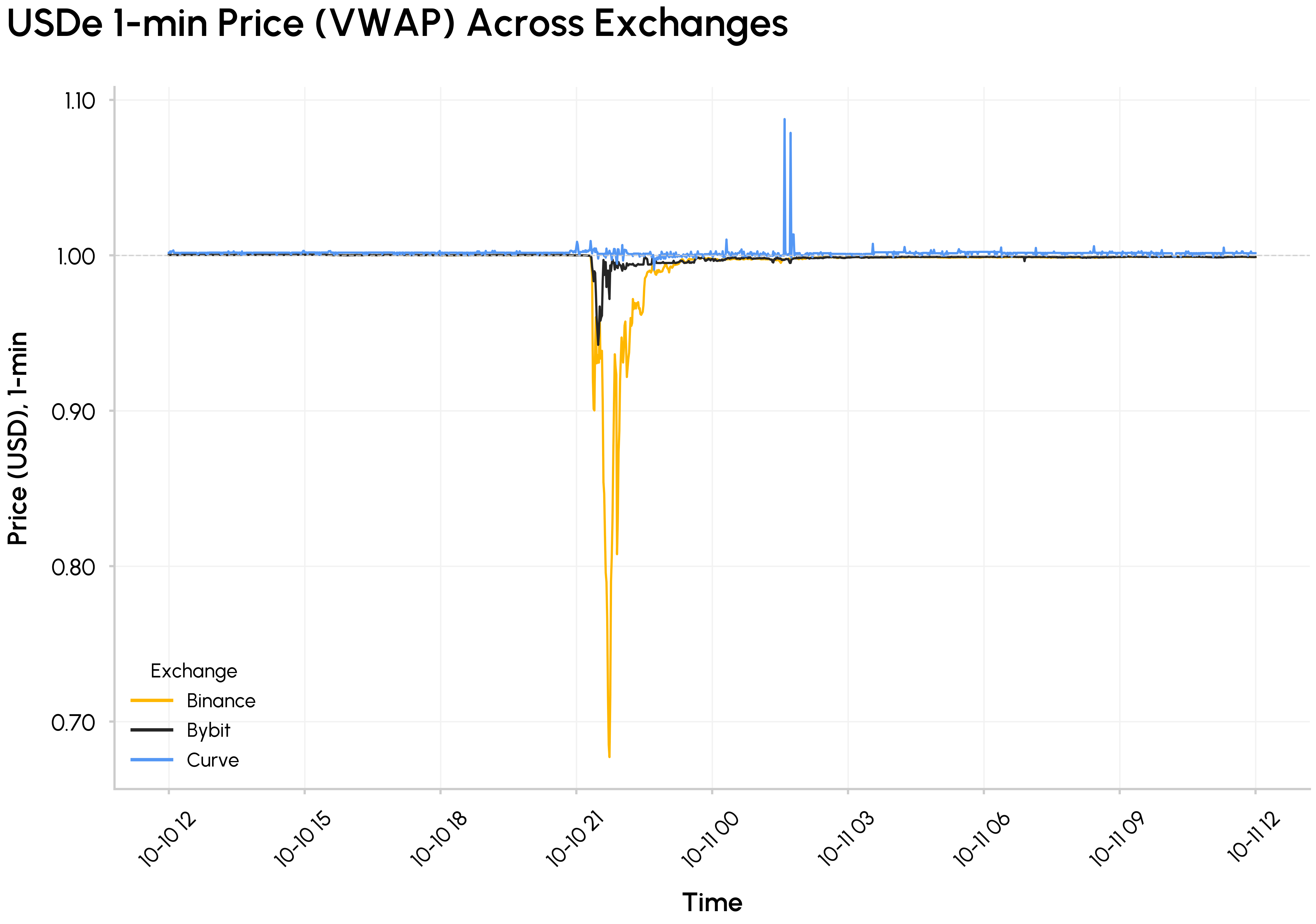

If collateral prices fall faster than liquidations can execute, vaults are left with undercollateralized positions.In March 2026, Resolv Labs’ USR collapsed after an attacker minted 80M unbacked tokens, generating bad debt across several vaults on Morpho, Euler, and Fluid. Curators manage this through conservative LTV ratios, borrow caps, and strict collateral whitelists. - Oracle risk: the risk that faulty, manipulated or hard-coded price feeds trigger incorrect liquidations or allow undercollateralized borrowing.

In October 2025, USDe fell to $0.65 on Binance due to an internal oracle referencing a thin orderbook despite Ethena’s collateral remaining intact. Oracle source selection and fallbacks are core parts of curator design, handled through multi-source oracle configurations and avoiding feeds that reference thin or single venue liquidity.

Conclusion

Vaults are rapidly becoming the core allocation and abstraction layer for onchain asset management. Powered by ERC‑4626 standardization, curated institutional strategies, and modular lending infrastructure, they are now the primary way to access stablecoin yield, RWA exposure, and more complex basis or credit trades. Looking ahead, vaults are set to underpin onchain credit and fixed income, turning increasingly sophisticated and off‑chain exposures into programmable, interoperable primitives. Scaling the category will require balancing the surface area of risk against the rewards, especially as more off‑chain assets and complex strategies are brought onchain.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.