Circle Scenario Analysis and KelpDAO's DeFi Liquidity Shock

State of the Network #360

Circle Scenario Analysis and KelpDAO's DeFi Liquidity Shock

Introduction

State of the Network #360

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways

- Circle’s $2.7B in FY2025 revenue was almost entirely driven by interest on USDC reserves, making the interest rate path, USDC supply growth and August 2026 Coinbase renewal key variables for its earnings outlook.

- USDC is increasingly being used, not just held: adjusted transfer volumes grew ~320% YoY in 2025, with early traction in Circle Payments Network, CCTP, and subscriptions forming a fee-based layer alongside the reserve income foundation.

- A ~$290M exploit of KelpDAO’s rsETH bridge rippled into a broader DeFi liquidity shock as unbacked rsETH was used to borrow WETH on Aave, draining liquidity and sparking a wider “bank‑run” across affected DeFi markets.

Introduction

It’s been almost a year since Circle (CRCL) went public on the NYSE. Shares quickly ballooned from a $31 IPO price on June 5th to over $280, taking the stablecoin issuer to a peak market cap of roughly $70B.

Since then, however, the stock has round‑tripped from its lofty valuation, trading closer to $103 at a current market value of about $26B. As the post‑IPO momentum phase has settled, more focus has shifted to the fundamentals of Circle’s business model and whether to view it as a reserve‑income business or as a broader payments and infrastructure platform.

In this State of the Network, we take a closer look at the key forces shaping those fundamentals going ahead, building on our previous analysis of Circle’s IPO and USDC economics. We examine Circle’s sensitivity to interest rates, the evolution of the USDC economics with Coinbase, potential yield restrictions under the CLARITY Act, and Circle’s ability to grow other fee and subscription revenues beyond reserve income.

Circle Business Model & 2025 Financials

Circle’s business model today is largely driven by four levers:

- USDC circulating supply

- Effective yields on USDC reserve assets

- Circle’s take‑rate on USDC reserve income (after distribution to partners like Coinbase)

- Subscription, services, and other fee revenue

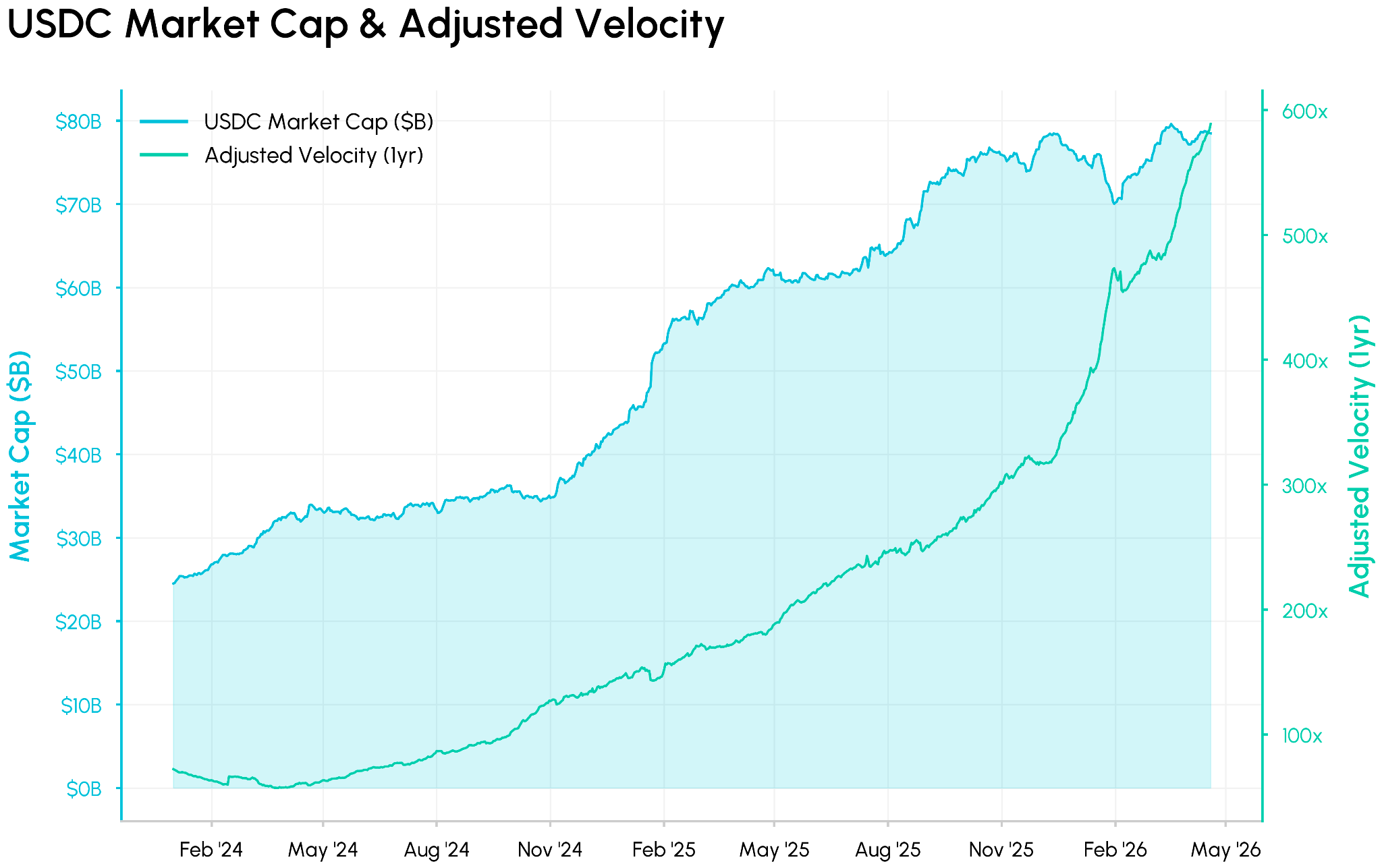

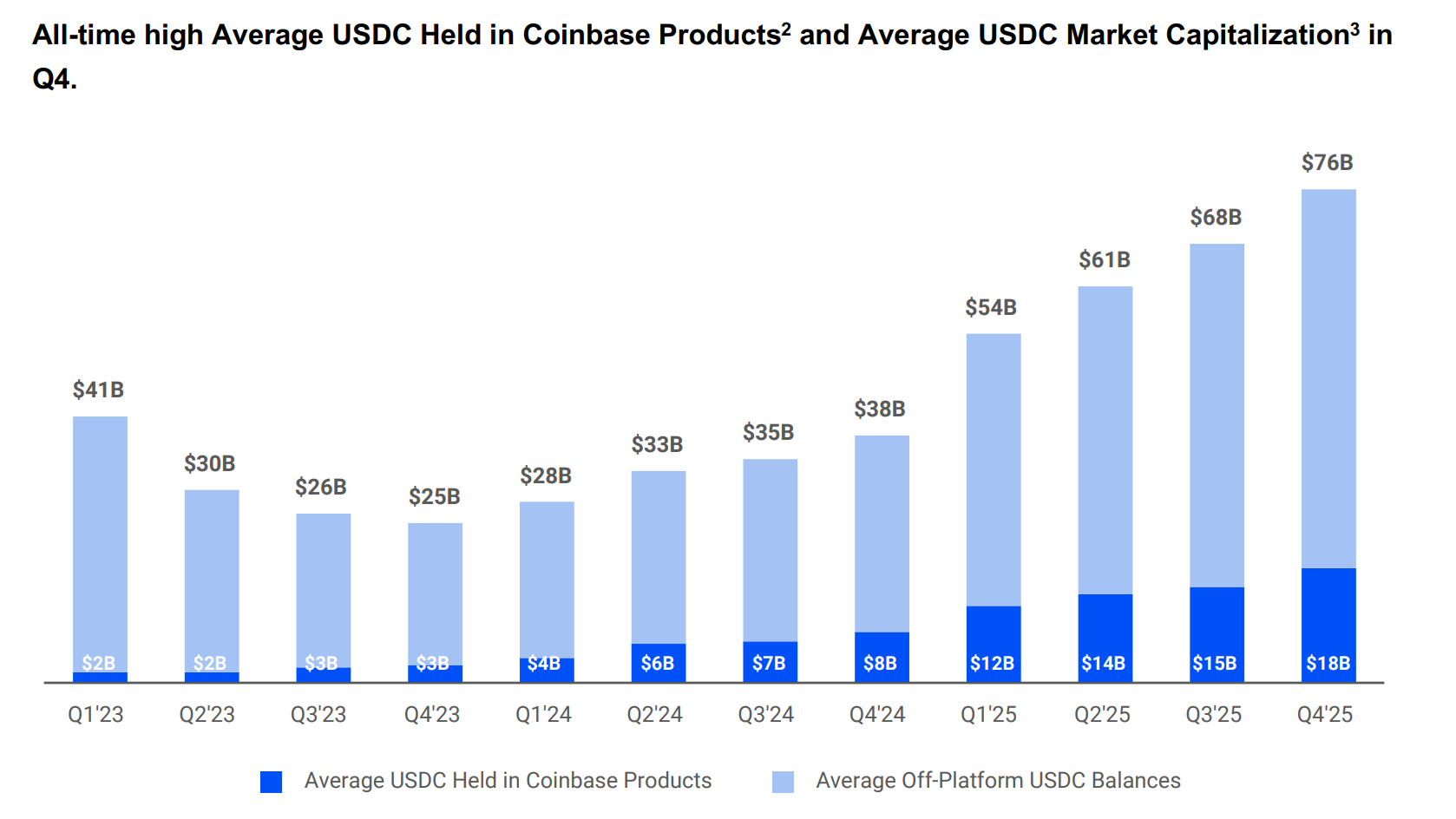

In FY 2025, Circle generated about $2.7B in total revenue and reserve income, up 64% YoY. This was boosted by USDC’s market cap reaching $75.3B by year end, maintaining a stablecoin market share of ~28% and 320% YoY growth in transaction volumes, implying higher velocity.

Source: Coin Metrics Network Data Pro

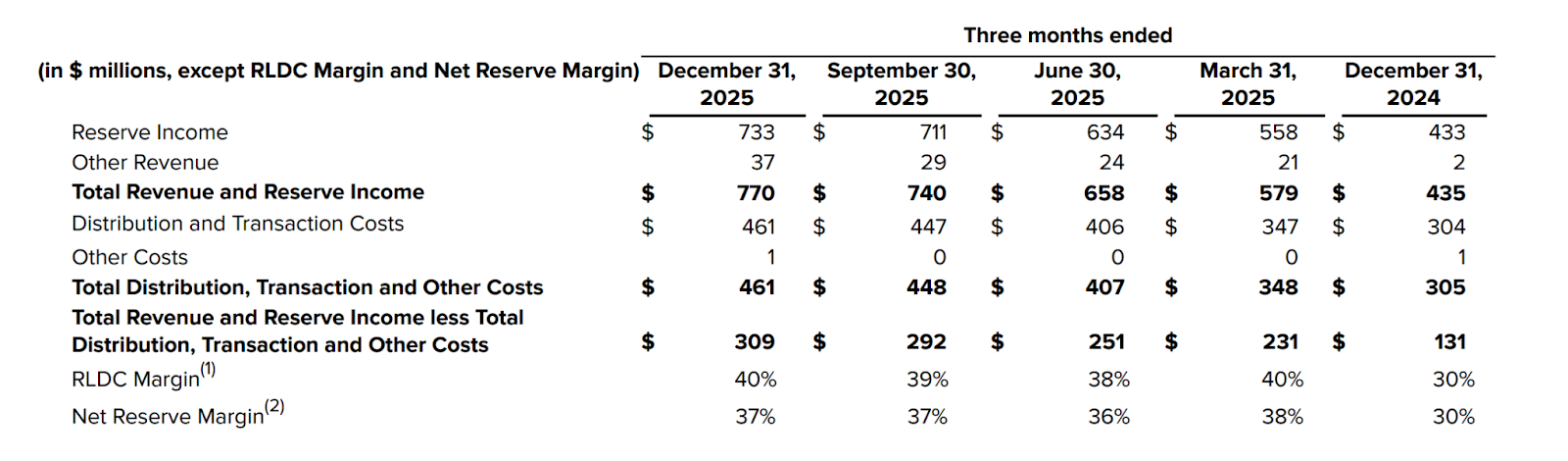

Reserve income tied to USDC balances and rates remained the dominant source of revenue ($2.64B, 96%) while subscription, services, and other fees grew from a smaller base but started to contribute more visibly to the top line ($110M).

Distribution, transaction, and other costs were $461M in Q4, reflecting the economics shared with partners for USDC distribution and usage. After those costs, Revenue Less Distribution Costs (RLDC) came in at $1.08B, for a full-year RLDC margin of 39%, a useful way to think about what Circle actually keeps from USDC economics before operating expenses.

Source: Circle Q4 2025 Earnings

The company’s near-term financial profile therefore remains driven mainly by USDC in circulation, reserve income, and the economics of revenue-sharing arrangements, particularly with Coinbase. In the sections ahead, we model how shifts in these levers could affect Circle’s financials and revenue profile.

Circle Scenario Analysis

Interest Rate Sensitivity

With roughly 96% of FY 2025 revenue coming from reserve income, Circle’s earnings power today is a function of short‑term interest rates on USDC reserves. Estimates based on Circle’s guidance suggest that a 100 basis point cut in rates would reduce annual revenue by roughly 25–30%, implying a close relationship between interest rates and Circle’s top line. Against Fed projections and futures that put the funds rate in roughly the 3–3.75% range through 2026–27, the key question is how much USDC growth can offset the drag from lower yields.

To illustrate this, we lay out a simple matrix of scenarios. Each cell shows an estimate of annualized reserve income at different combinations of effective reserve yield and USDC circulating supply, using FY 2025’s ~$2.7B at a 4.1% yield and ~$65B average supply as the baseline.

Circle Reserve Income Matrix:

Source: Coin Metrics Network Data Pro

At the high end of rate expectations (~4–4.5%), reserve income can grow from the 2025 base, with supply in the $90–110B range pushing reserve income well above $4B. Around 3–3.5%, roughly where the Fed’s 2026–27 projections and futures cluster, moderate USDC growth from the current ~$75B level can keep reserve income roughly flat to slightly higher versus FY 2025.

In a deeper easing scenario with effective yields closer to 2.5%, even very strong USDC growth only partially offsets lower rates, and reserve income could end up roughly 30–50% below what a higher‑for‑longer path would have delivered for a similar supply base.

Coinbase Revenue Sharing & Distribution

Circle’s economics are also heavily shaped by distribution arrangements, particularly with partners like Coinbase. Under the current agreement, Coinbase receives all of the interest on USDC held on its platform and 50% of the interest on USDC held elsewhere, in exchange for driving USDC distribution and demand through its products and user base.

Source: Coinbase Q4 2025 Shareholder Letter

In FY 2025, while Circle reported $2.63B in reserve income, roughly $1.35B (about 51% of gross reserve income) flowed to Coinbase under this revenue sharing structure. As a result, Circle’s revenue less distribution costs (RLDC) came in at $1.08B, leaving a 39% margin. This makes the Circle‑Coinbase relationship both strategic and economic: Coinbase is simultaneously one of the largest demand and distribution channels for USDC and a major beneficiary of USDC’s reserve income.

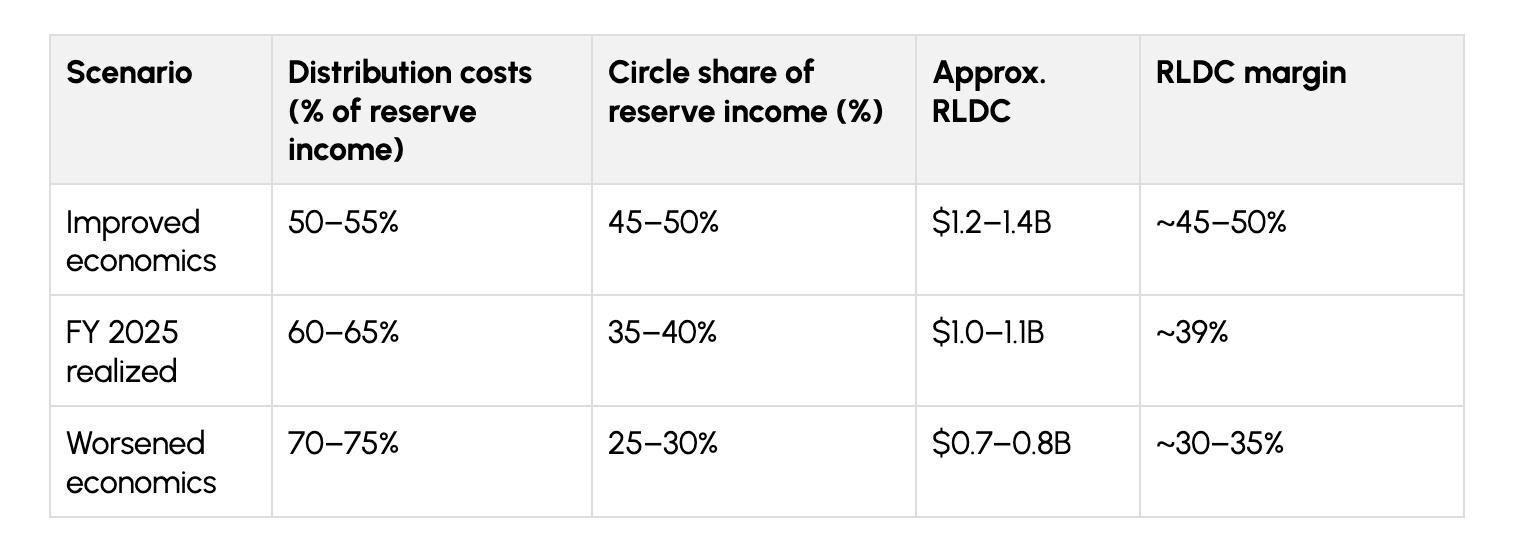

With this revenue‑sharing agreement up for renewal in August 2026, small changes in Circle’s take‑rate on USDC reserve income could compound with the rate and supply scenarios above. Using FY 2025 as a base, we can summarize the impact of different distribution outcomes as follows:

In the improved economics case, renewal terms and distribution diversification push costs down, raising Circle’s take‑rate and RLDC margins. The FY 2025 realized reflects where we are today, where Circle keeps roughly $0.37 of each dollar of reserve income and remains dependent on elevated rates and a ~$75B USDC base. The worsened economics case is a risk scenario in which Coinbase and other partners capture a larger share of USDC reserve income, pushing RLDC margins lower and leaving CRCL more exposed to any combination of lower yields and weaker USDC growth.

Other Revenue Streams & Potential Risks

Beyond reserve income and distribution costs, a handful of emerging factors will shape Circle’s longer-term revenue profile and competitive positioning. Other Revenue, which includes subscription and services fees, transaction revenue, and validator income, grew from just $15M in FY2024 to $110M in FY2025, and is guided to $150–170M in FY2026. At roughly 4% of total revenue today, it remains small, but its trajectory matters for how the market eventually values Circle. Key factors to watch include:

- CLARITY Act Yield prohibition: A draft provision in the CLARITY Act would prohibit stablecoin issuers from paying yield directly to holders, instead allowing “activity-based rewards”. This is a nuanced risk for Circle as the yield from USDC is not paid out to holders, so it may not directly impair Circle’s model and help them retain interest income. The indirect risk is Coinbase’s ability to attract USDC balances through its own yield-sharing programs becoming constrained, which could shift the on-platform/off-platform mix in ways that affect Circle’s distribution costs and overall USDC demand.

- Circle Payments Network (CPN) & CCTP: Circle Payments Network launched in May 2025 and reached an annualized TPV of $5.7B by February 2026, with 55 institutions live and 500+ in the pipeline across 14 markets. CCTP, Circle’s cross-chain transfer protocol, processed $41.3B in Q4 2025 alone and now holds 62% of the USDC cross-chain market. Both are early-stage but show evidence that USDC velocity is growing faster than supply, and that Circle is building a fee-based layer on top of its reserve income foundation.

- Arc (L1 Settlement Chain): Arc is Circle’s stablecoin optimized blockchain planned for mainnet launch in 2026, with USDC as the native gas token. Arc remains nascent in monetization until real capital moves on-chain. But if it starts gaining adoption in areas like cross-border payments, agentic commerce or tokenization, it could shift Circle’s value proposition from a rate-sensitive business to a platform warranting a different valuation lens.

For market participants, the main variables are the pace of USDC circulation growth, the economics of the August 2026 Coinbase renewal, and how quickly non‑reserve “Other Revenue” scales through CPN, CCTP, and Arc. At a roughly $25–30B valuation on about $2.7B of trailing revenue, CRCL is being priced as a rate‑sensitive infrastructure platform and one of the few liquid ways to gain exposure to secular stablecoin growth, with its valuation likely to move alongside confidence in those levers.

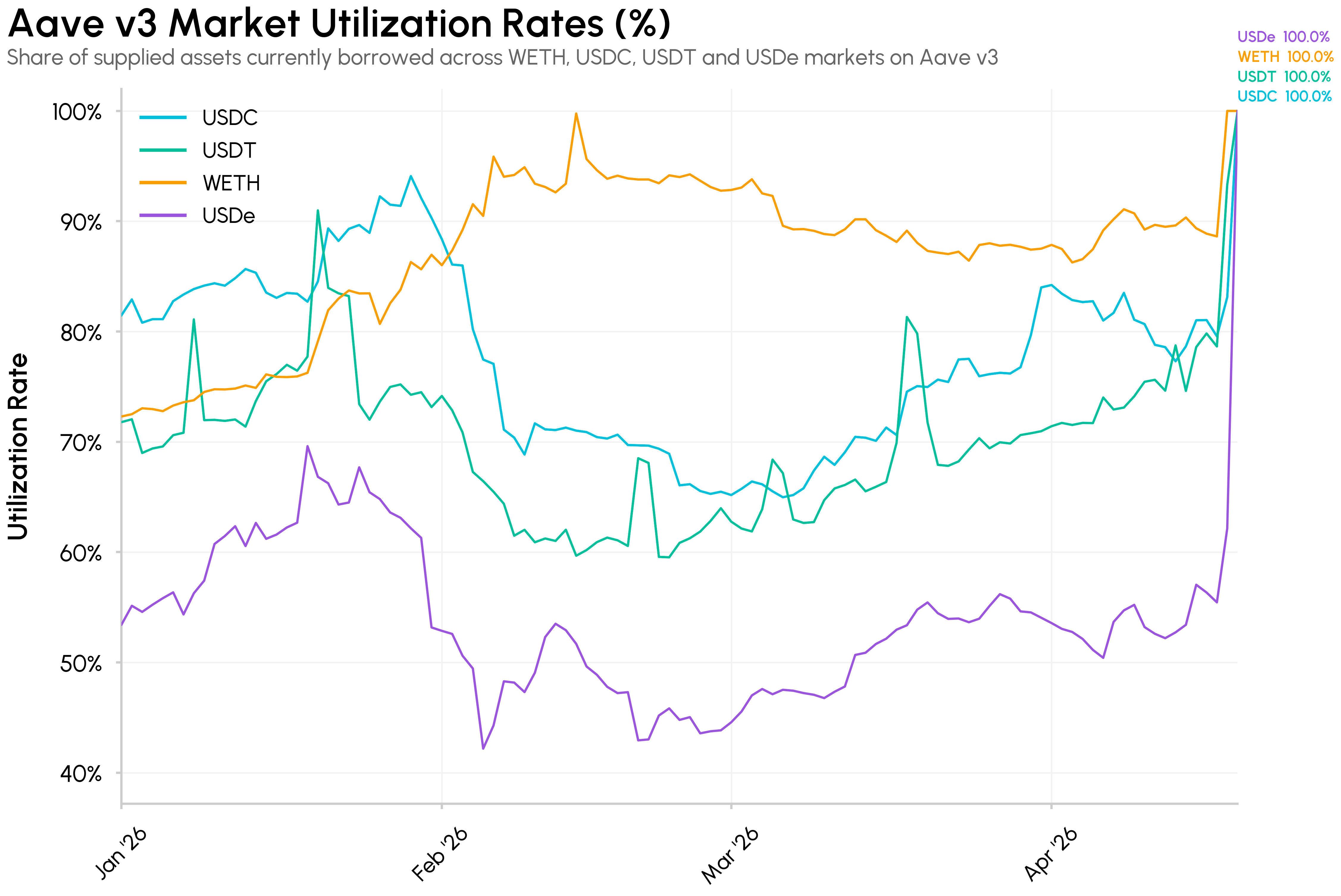

KelpDAO Exploit Sets off DeFi Liquidity Shock

This week, we witnessed the largest hack of 2026 from which contagion has spread across DeFi. On April 18th, an attacker exploited KelpDAO’s rsETH cross‑chain bridge configuration, draining around 116,500 rsETH (worth roughly $290M and 18% of supply) by targeting a LayerZero DVN setup that relied on a single verifier.

rsETH is a liquid restaking token that represents claims on restaked ETH. The attacker was able to mint “fake” rsETH on one side of the bridge without backing. The stolen rsETH was then deposited as collateral across lending markets, most notably Aave, to borrow WETH.

This has caused the Aave v3 WETH market to be drained, reaching 100% utilization and leaving no liquidity available for immediate withdrawals. Due to the risk of bad debt, the shock in WETH quickly evolved into a broader liquidity run, with spiking utilization rates across USDC and USDT markets and over $9B in deposits pulled from Aave.

Source: Coin Metrics Network Data Pro

The incident is a stark example of how DeFi’s interconnectedness can be both beneficial and dangerous. A single compromised verifier in the cross‑chain stack cascaded through the bridge, into a restaking token, and into lending markets and other DeFi protocols, ultimately draining on‑chain liquidity far beyond the original exploit.

It also highlights how risks can stack up with derivative collateral like rsETH, which bundles Ethereum staking, restaking protocol risk, bridge infrastructure, and lending‑market risk into one. As we covered in our previous issue on vaults, collateral selection, curation and safeguards in lending markets becomes critical in this environment, because one misconfigured asset can ripple across the entire ecosystem.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

.jpg)

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.