Hyperliquid: Perps, Outcome Markets and USDC Yield

Introduction

State of the Network #368

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

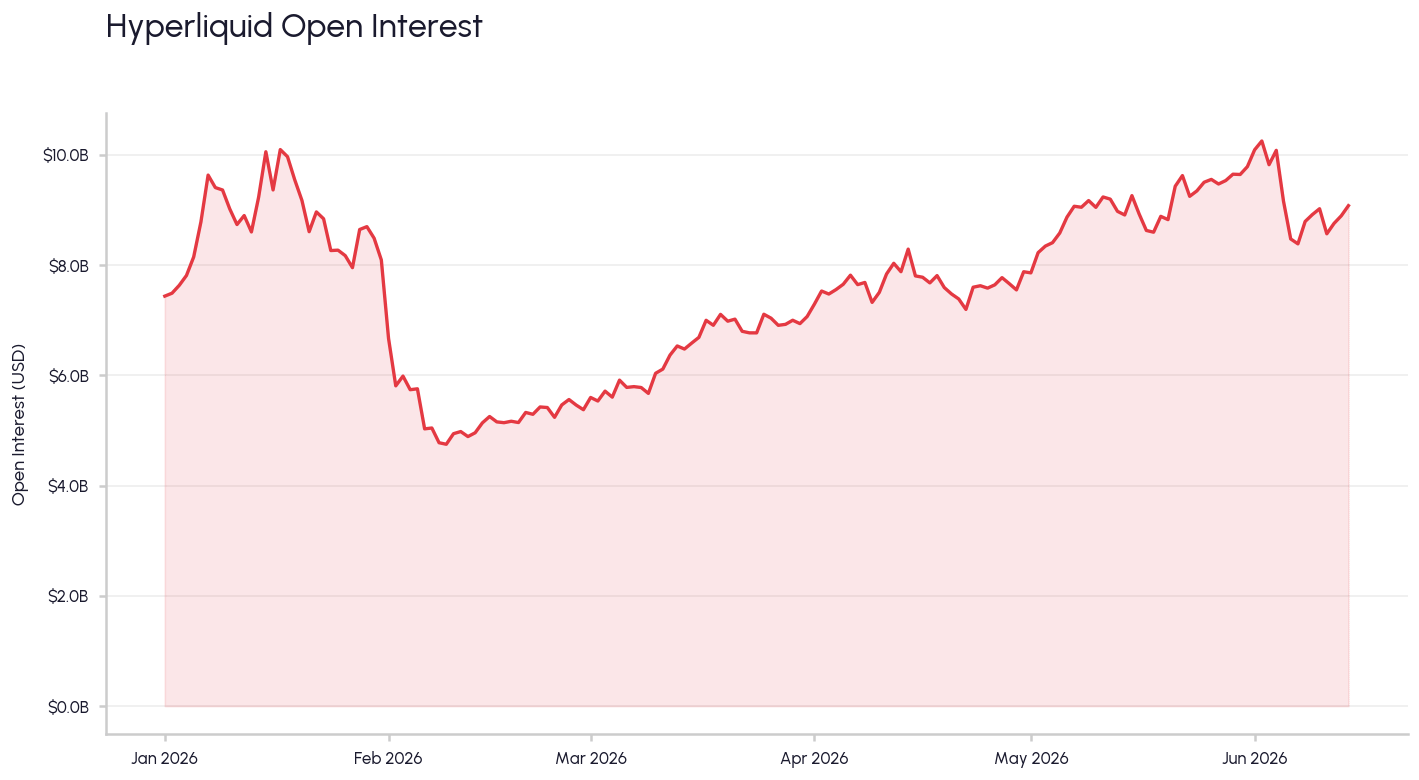

- Hyperliquid’s $10 billion in perpetual futures open interest highlights growth in asset classes including equities, commodities, and pre-IPO markets.

- Around $3 billion in daily volume is traded on HIP-3 builder deployed perpetuals, emphasizing trading expansion outside of crypto markets.

- USDC sharing a portion of the underlying reserve yield with Hyperliquid enables additional HYPE buy backs and aligns Coinbase and Circle as strategic partners in the ecosystem.

Introduction

With over $10 billion in perpetual futures open interest, growing exposure to equities, commodities, and synthetic pre‑IPO trading, and expanded stablecoin integration, Hyperliquid continues to evolve toward supporting any market for every investor.

Hyperliquid was launched in February 2023, providing an on-chain order book for perpetual futures. While many other blockchains rely on off‑chain matching engines and centralized sequencing to improve transaction speed and throughput, Hyperliquid brings these efficiencies on‑chain using a Central Limit Order Book (CLOB) similar to traditional exchanges.

In this State of the Network, we examine Hyperliquid’s funding rates relative to other exchanges, HIP‑3 DEXs and non‑crypto perpetuals, HIP‑4 outcome markets, and a growing partnership with USDC operators.

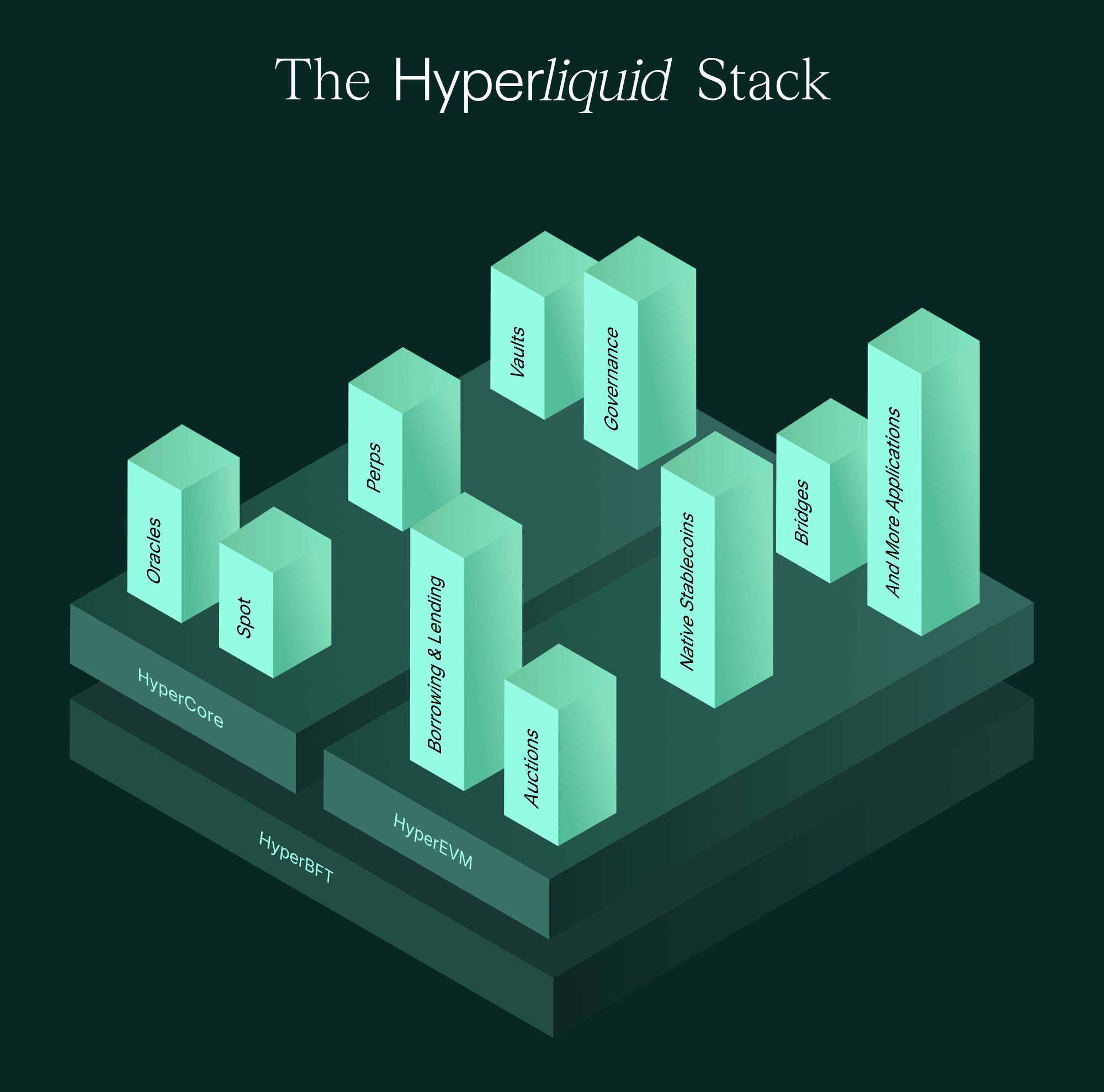

HyperCore and HyperEVM

Hyperliquid is composed of the HyperCore and general purpose HyperEVM. The custom consensus mechanism HyperBFT supports the on-chain order book infrastructure providing sub-second latency and the capacity to execute up to 200k orders / second. Every market deployed on HyperCore and HyperEVM benefits from this on-chain order book configuration.

Hyperliquid’s order book and matching engine has recently attracted around $10 billion in open interest, making it the third largest perpetual futures exchange. This has been driven by crypto-assets along with the introduction of equities, commodities, and indices trading through HIP-3. The HyperCore provides the trading infrastructure connected to the HyperEVM which extends the trading capabilities to other markets and financial services. $4 billion of open interest is attributable to HIP-3 builder deployed perpetual markets.

Source: Hyperliquid Documentation

The HyperEVM acts as a branch for developers to build with a familiar tech stack. Using the Ethereum Virtual Machine, builders can deploy new applications, lending protocols, and stablecoins to further develop the Hyperliquid ecosystem.

Competitive Funding Rates

Popularized by the crypto industry, perpetual contracts or “perps” are a form of futures contract with no expiration date. This reduces trading frictions like rolling over contracts. As futures approach expiration, their price trends towards the spot price. Perpetuals do not have an expiration, so how do they remain near the spot price?

Funding rates are used to prevent the future price from significantly deviating from the spot price. When funding is positive, long positions pay a percentage to short positions, and vice versa when funding is negative. This incentivizes traders to take opposing positions to align the future price with the spot price.

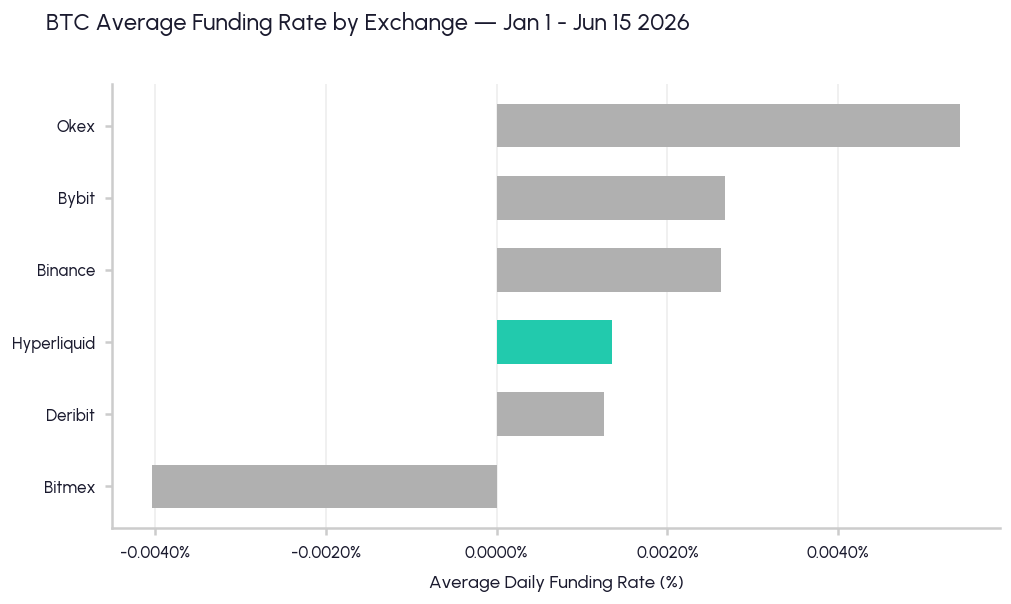

Shopping around for perpetual markets with the lowest funding rate can reduce trading costs. Large positive funding rates can erode gains from long positions; therefore, searching for small funding rates can help increase trader profits. Funding is paid every hour, so multi-day or monthly positions can become expensive.

Since January 2026, Hyperliquid funding rates on a weekly rolling standard deviation have been more volatile than other exchanges. The Hyperliquid-BTC perpetual funding rate is 1.95x more volatile than the Binance-BTC perpetual and 3.32x more volatile than the Deribit-BTC perpetual, impacting funding costs over shorter durations. While more volatile, over the last six months, Hyperliquid-BTC has the second lowest funding rate for long traders. On average, the Hyperliquid-BTC funding rate is 0.00135%, 0.01 basis points more than Deribit-BTC.

HIP-3: Expanding to Traditional Asset Classes

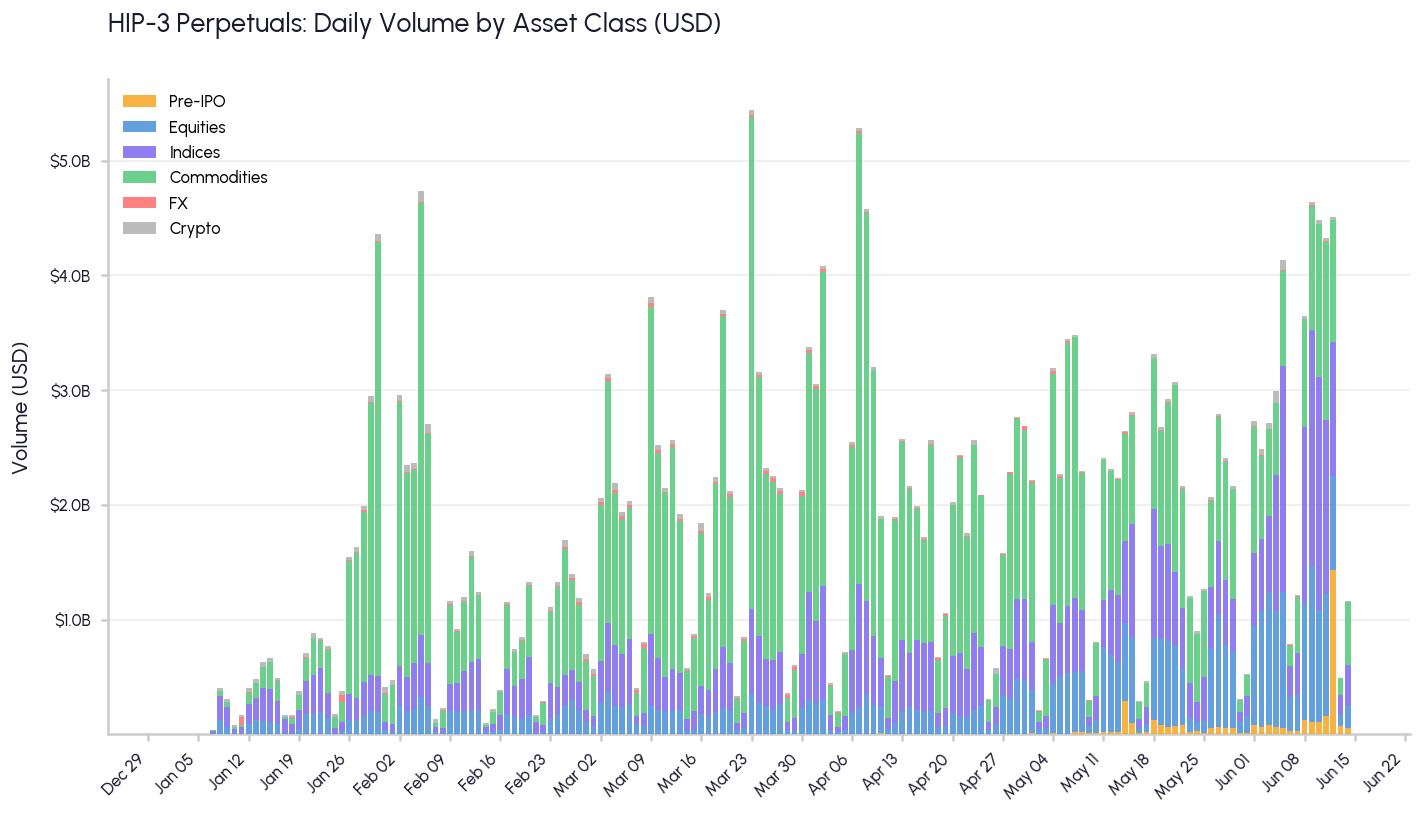

Hyperliquid Improvement Proposal (HIP)-3 enabled non-crypto markets and distributed market creation to the community. HIP-3 supports permissionless, builder-deployed DEXs. These DEXs such as trade.xyz manage their own listings, margin limits, and oracles. Perp DEXs must stake 500k HYPE or around $33.5 million to operate, ensuring economic security and high quality builders.

Today, equity and commodity markets are among the most actively traded markets across HIP‑3 DEXs. Oil, the Nasdaq 100, and technology stocks regularly see daily volumes over $100 million. While trading volume primarily occurs on days when traditional markets are open, nearly half of S&P 500 and over 60% of Oil perpetual volume still occurs outside U.S. market hours, allowing traders to react to earnings, macro data, or geopolitical events in real time. Trading on company valuations shortly before their IPO has also attracted attention with over $250m in perpetual open interest on June 12th in anticipation of the SpaceX (SPCX) IPO.

HIP-4: Outcome Markets

HIP-4 introduced “Outcome Markets” which offer fixed-returns based on external events. These Outcome Markets diversify the instruments available to traders. Traders can access Outcome Markets without managing margin or liquidations.

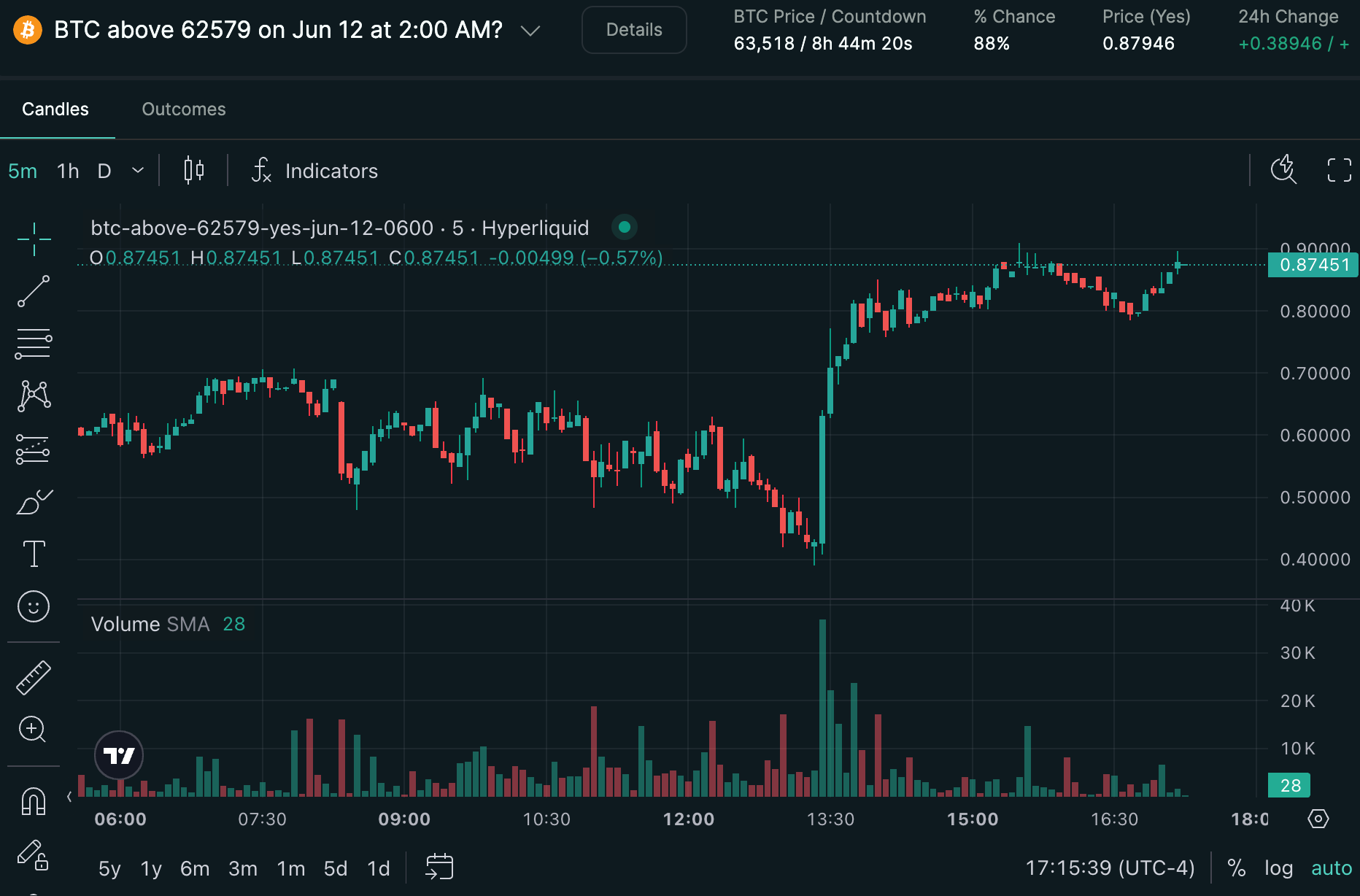

Outcome Markets provide alternative hedging strategies to perpetual contracts. For example, Hyperliquid hosted a market on whether BTC would end above $62,579 on June 12 at 2:00am EST. The market price at 5:15pm EST on June 11 indicated an 87% probability BTC would end above the designated price. If a trader was short BTC, they could hedge their short BTC with an Outcome Market position with an expiration in the near future.

Source: Hyperliquid App

USDH and USDC

In September 2025, Hyperliquid requested feedback for a native stablecoin deployment that would benefit both the markets and users. Native Markets was selected by stakers as the stablecoin issuer, winning the ‘USDH’ ticker and proposing a revenue-sharing system to become the default quote stablecoin for new markets.

In May 2026, Coinbase announced the acquisition of USDH brand assets and the migration from USDH to USDC. USDH holders can redeem their USDH 1:1 for USDC. USDC on Hyperliquid has become an Aligned Quote Asset (AQA), making it the primary asset for margin, spot and perpetual trading. As an AQA, Circle and Coinbase must stake $500k HYPE each which can be slashed if services are not consistently maintained.

Hyperliquid’s AQAv2 standards also require revenue sharing of the underlying collateral with the protocol. For every $1 of yield earned by treasuries and short-term assets backing USDC on Hyperliquid, Circle and Coinbase must share ~90% of the reserve yield with Hyperliquid. Assuming a stable $5 billion USDC on HyperEVM and steady interest rates, Hyperliquid is projected to receive around $160 million / year from Circle’s investments in Overnight Repurchase Agreements and short-term treasuries.

Before USDC could be natively minted and withdrawn from Hyperliquid, USDC was deposited through the Arbitrum-Hyperliquid bridge. The bridge is no longer required with native USDC minting and redemptions on Hyperliquid. Shortly after the acquisition announcement, the bridge now holds less than $1 billion USDC.

Revenue Use and HYPE token

USDC becoming an AQA and distributing yield to Hyperliquid leads to additional revenue earned by the protocol. Based on the new revenue sharing structure and current assumptions, Hyperliquid expects to buy back and burn an additional $450m of HYPE. Today, Hyperliquid primarily allocates trading fees to buy back outstanding HYPE tokens in the market which are then burned from supply. Burning tokens is similar to stock buy backs, reducing float to support token value.

HYPE is staked by market deployers and service providers to align incentives with Hyperliquid. Deployers must stake 500K HYPE to begin operating an HIP-3 market. HYPE is required to interact with the Hyperliquid ecosystem – staked by validators as economic collateral, by traders to earn fee discounts, and used to pay transaction fees on HyperEVM.

Conclusion

Hyperliquid’s builder-friendly environment and on-chain order book design enables rapid market expansion for various assets within a single unified venue. Perpetual futures for non-crypto assets and outcome markets provide more opportunities for traders to react to market changes, regardless of whether traditional markets are open.

Circle returning underlying reserve yield to Hyperliquid, with revenue used to buy back and burn HYPE tokens generates demand for a token that is necessary to operate in the ecosystem. Hyperliquid continues to build synergistic products that complete the financial service stack.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.