Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- Tokenized stocks today fall into three broad buckets: issuer‑native equity, custodial wrapped equity, and derivative exposure, each representing a different onchain claim on the same underlying stock.

- Moving along this spectrum trades off direct ownership and shareholder rights for greater accessibility, capital efficiency, and simplicity of execution.

- These structural differences translate directly into how markets behave. Taking Nvidia as an example, exposure through Backed’s NVDAx, Ondo’s NVDAon, and NVDA perpetual futures leads to occasional price gaps and fragmented liquidity.

Introduction

The tokenization of equities has seen significant momentum since we last explored the rise of xStocks in December. The Depository Trust & Clearing Corporation (DTCC) has announced its tokenized securities pilot, the New York Stock Exchange (NYSE) is developing a platform for tokenized stock trading, and Coinbase revealed the launch of 1:1 backed tokenized U.S. equities last week. While these are all lumped into the same category, they carry different properties.

The SEC has also started to formalize how they view the sector, mapping out the main models for tokenizing securities. With this expansion in issuers, structures, and exchange access, it is becoming increasingly difficult to understand what each form of tokenized equity exposure actually provides.

In this issue of State of the Network, we map the spectrum of tokenized equity models and show how those structures shape pricing and trading through the lens of Nvidia. Throughout this, we refer to tokenized equity and tokenized stock as blockchain-based instruments tracking publicly traded company shares.

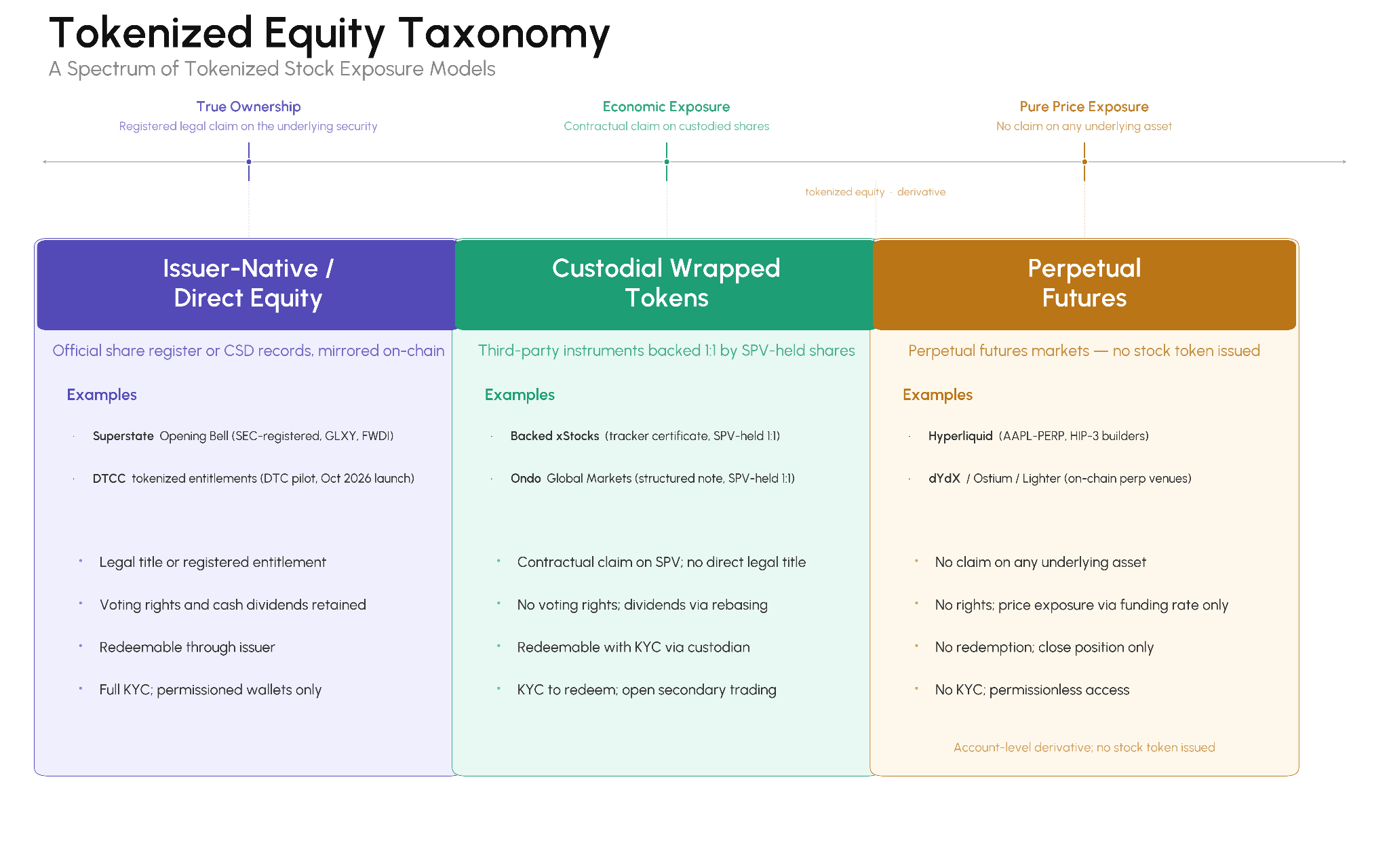

The Different Models of Stock Tokenization

Not all tokenized equity is the same. A “tokenized” stock can mean a range of instruments with different legal structures, shareholder rights and risk profiles. A natively issued stock is different from a custodial wrapper that provides economic exposure, which itself differs from a perpetual futures contract with no claim on the underlying asset.

While perpetual futures are not tokenized equity, we include them because they are the most widely used form of onchain stock exposure today, and provide a useful point of comparison for true tokenized products. The examples shown reflect where each product broadly falls based on the nature of the exposure they provide. Some products sit closer to the boundary between categories. DTCC’s tokenized entitlements model, for instance, mirrors existing DTC-held securities onchain rather than issuing native equity directly. As the market develops, these boundaries will continue to evolve.

These models are best understood as a spectrum across three major categories, from true ownership of a registered security, to economic exposure via a custodial wrapper, and pure price exposure through a derivative contract. In the rest of this report, we refer to these three buckets as issuer‑native equity, custodial wrapped equity, and derivative exposure.

Source: Talos Research

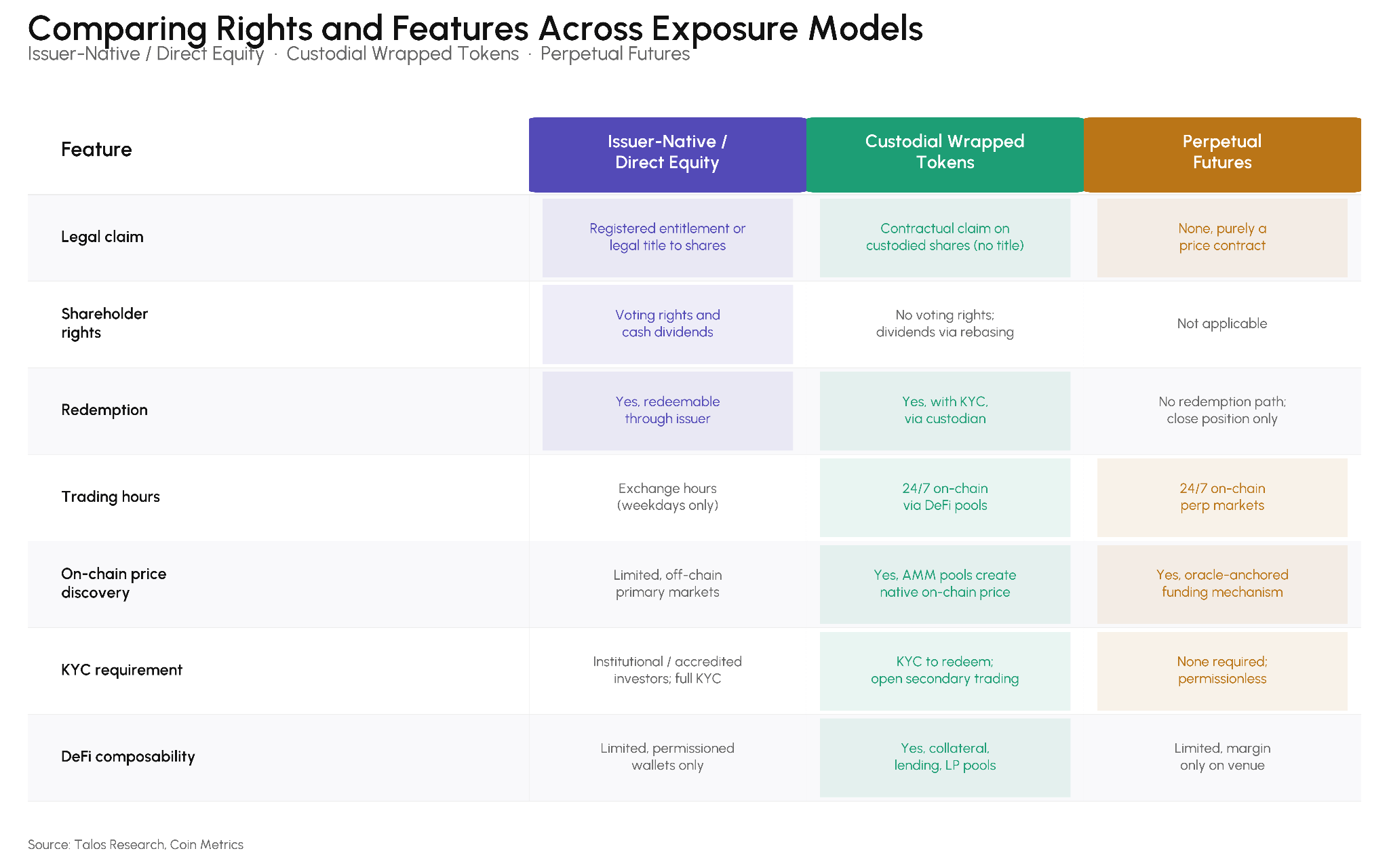

The structural differences between these models determine what a holder actually owns and what they can do with it. The table below maps the key features across each model, from legal claim and shareholder rights to trading hours, KYC requirements, and DeFi composibility. The tradeoff is, as you move from true ownership toward pure price exposure, you gain accessibility and flexibility but own less of the underlying and the rights that come with it.

Source: Talos Research

An advantage that all models share over traditional direct equity is onchain price discovery. Previously, blockchains could only receive equity pricing through external oracles tied to traditional market hours. A tokenized or derivative version of an equity enables continuous onchain pricing, supporting composability with other protocols, collateral use cases, and price feeds independent of traditional market hours.

One Company, Different Exposures: Nvidia

Taking Nvidia (NVDA) as an example, a company with a ~$5T market cap now exists onchain in 3 different forms. While not yet directly issued onchain, it is available as custodial wrapped tokens (Backed NVDAx, Ondo NVDAon) and as perpetual futures markets (Hyperliquid, Binance). This makes it a useful lens to see how differences in the models play out in the data.

Backed xStocks (NVDAx)

Backed Assets (JE) Limited, a Jersey-registered special-purpose vehicle (SPV), focuses on the issuance and redemption of tokenized xStocks. These tokens are legally structured as “tracker certificates” issued by the SPV under Liechtenstein regulation. Backed 1:1 by the underlying asset, over 431,000 shares ($90M in market cap) of Nvidia are tokenized as NVDAx onchain.

When an investor buys NVDAx, they don’t own Nvidia shares. They own a claim on Backed Assets (JE) Limited, which holds the Nvidia shares. This means holders have no direct shareholder voting rights, but gain economic exposure that is freely transferable and composable with DeFi protocols as an ERC-20 or SPL token.

The NVDAx token represents the stock’s total return and is accessible across blockchains like Ethereum and Solana. These tokens are rebasing, meaning when a stock splits or pays dividends to shareholders, more tokens are minted to holders instead of paid out as cash. Users who complete KYC/AML onboarding with the issuer and brokerage can use the xPort service to redeem tokenized stocks for the underlying assets.

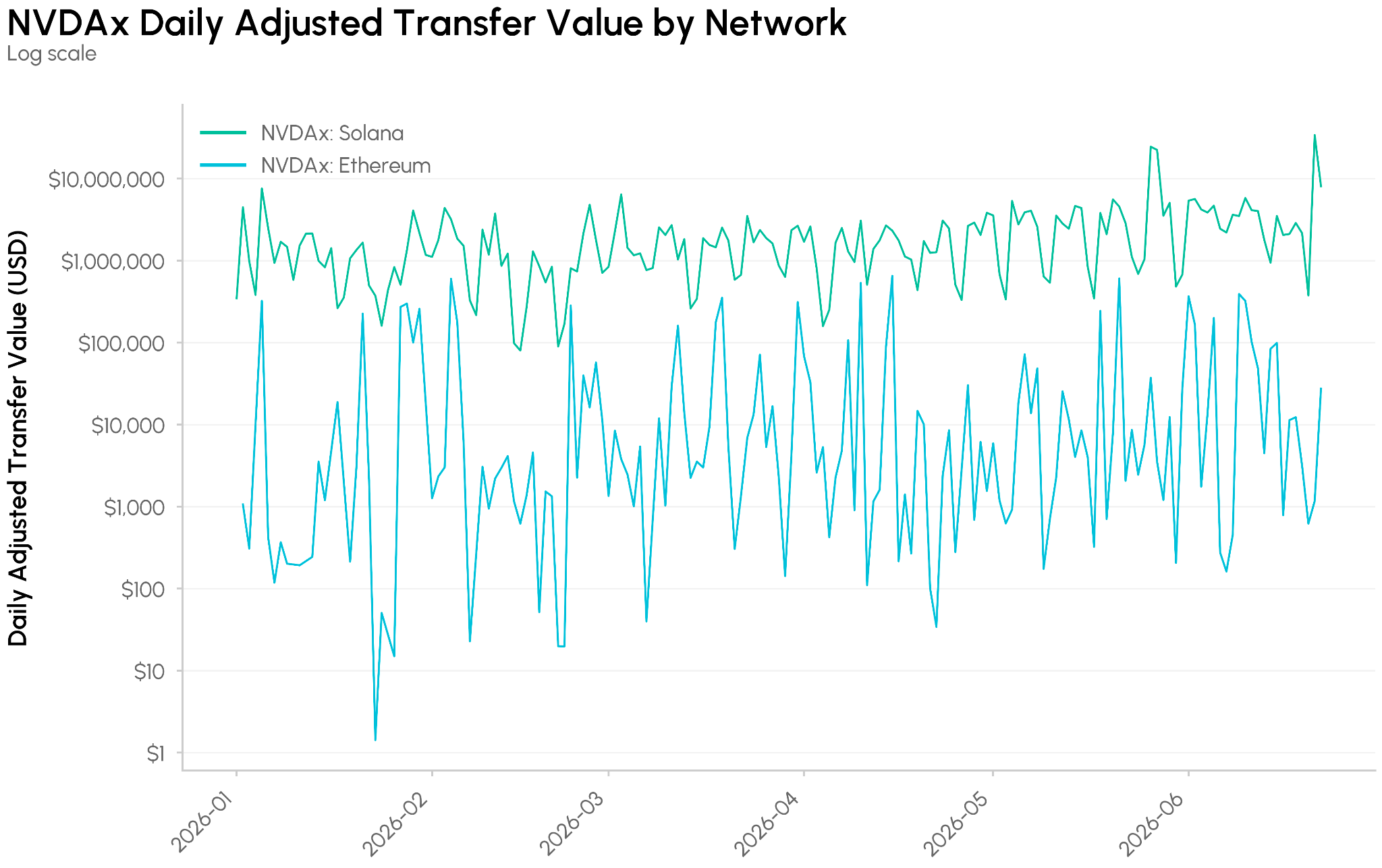

Source: Talos CM Network Data Pro

Transfer activity for an individual tokenized stock varies on chain. xStocks initially launched on Solana, where the median value of NVDAx transferred is $1.7M. On Ethereum, activity remains considerably lower at a median of $4k per day.

Ondo Tokenized Stock (NVDAON)

Ondo’s tokenized Nvidia stock (NVDAON) functions similarly but carries some structural differences to xStocks. NVDAON is also backed 1:1 with the underlying stock, with around 95K Nvidia shares tokenized via Ondo on Ethereum. NVDAON represents Nvidia stock’s total return, rebasing when dividends are paid or the stock is split.

While Backed operates through a Jersey SPV under Liechtenstein regulation, Ondo issues structured notes through a British Virgin Islands SPV, with the underlying shares held at U.S.-registered broker-dealers. The token is a total-return note rather than a tracker certificate, but the economic exposure is broadly similar.

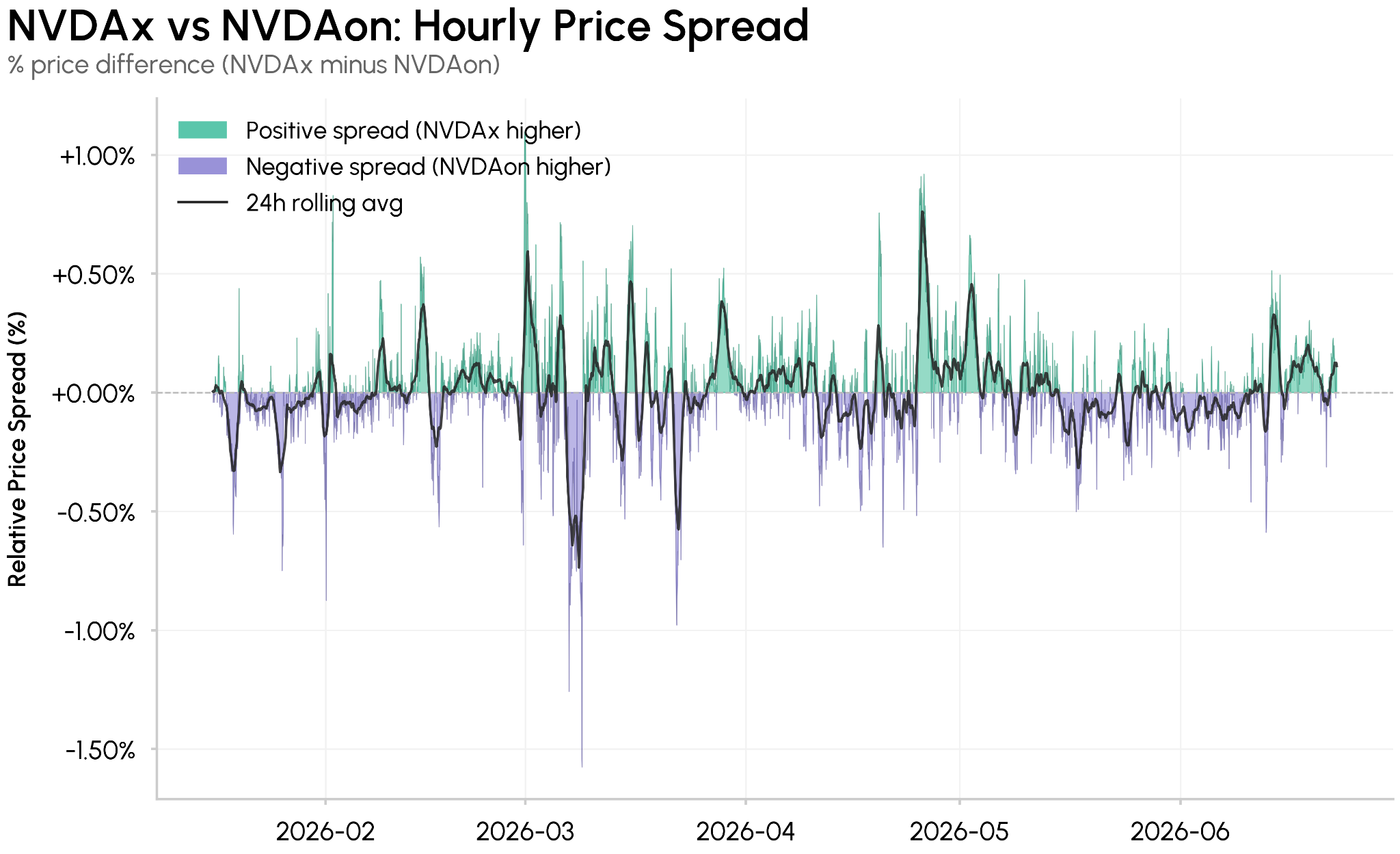

Source: Talos CM Reference Rates

Despite both products being backed 1:1 by the same company’s shares, the prices are not always aligned. They are issued by different legal entities, held in different custodial arrangements, and trade in separate liquidity pools, resulting in pricing differences and arbitrage opportunities. When NVDAx trades at a premium or discount to NVDAon, traders can buy the cheaper token and sell the more expensive one, helping narrow the gap.

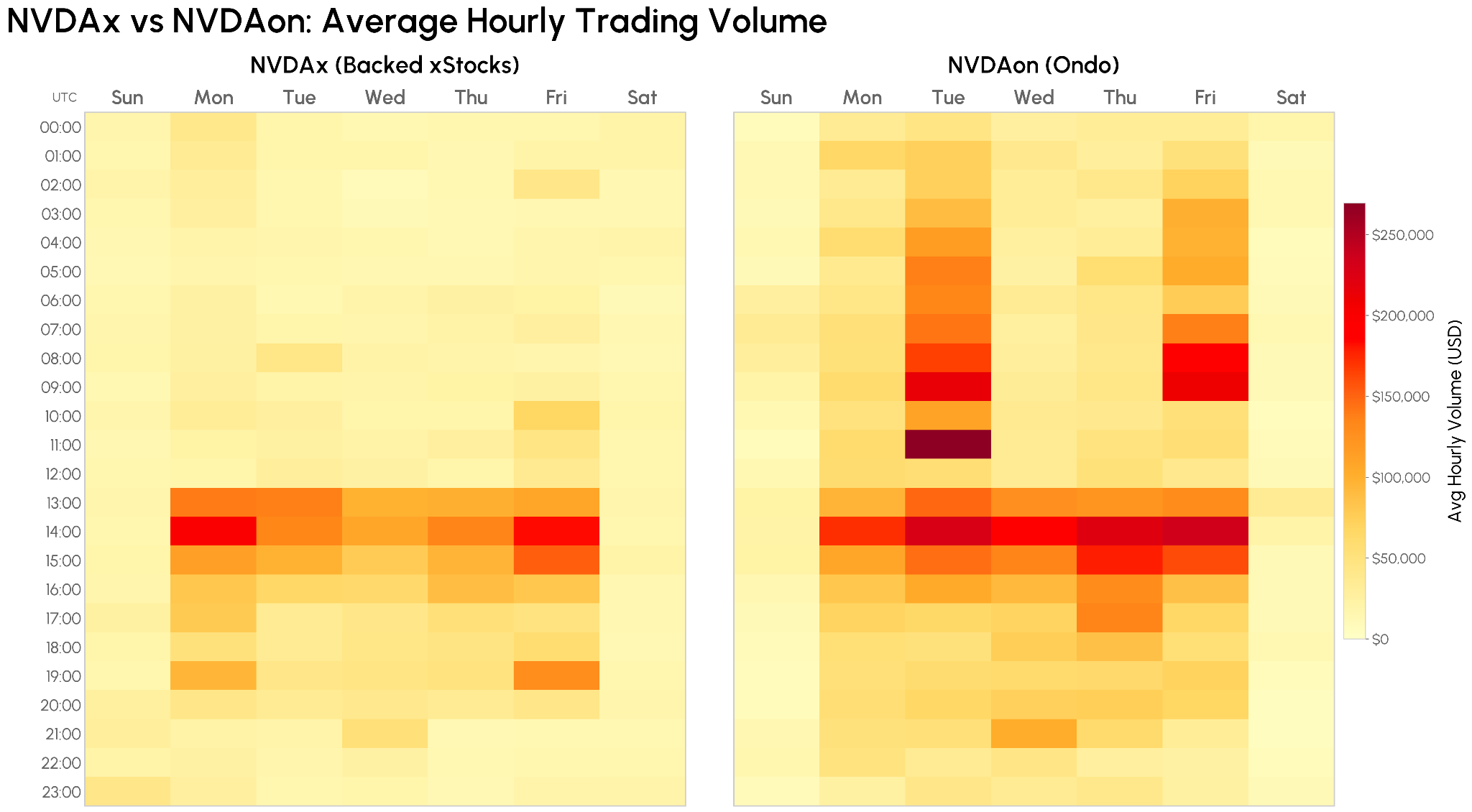

The trading patterns for each tokenized stock also differ when bucketed by hour of day. Across centralized exchanges, NVDAx and NVDAon activity is heaviest between 13:00 and 15:00 UTC, near the U.S. market open. This coincides with when the underlying NVDA liquidity is deepest, making cross-venue arbitrage easiest to execute.

Source: Talos CM Market Data Pro

However, NVDAon shows notably stronger European and Asian hours activity, with volume in those windows reaching 105% and 79% of its overall hourly average respectively. NVDAx also sees relatively more weekend activity, averaging 41% of its weekday volume compared to 17% for NVDAon. During peak weekday hours, NVDAon reaches average volumes of around $209,000 compared to $151,000 for NVDAx.

Nvidia Perpetual Futures

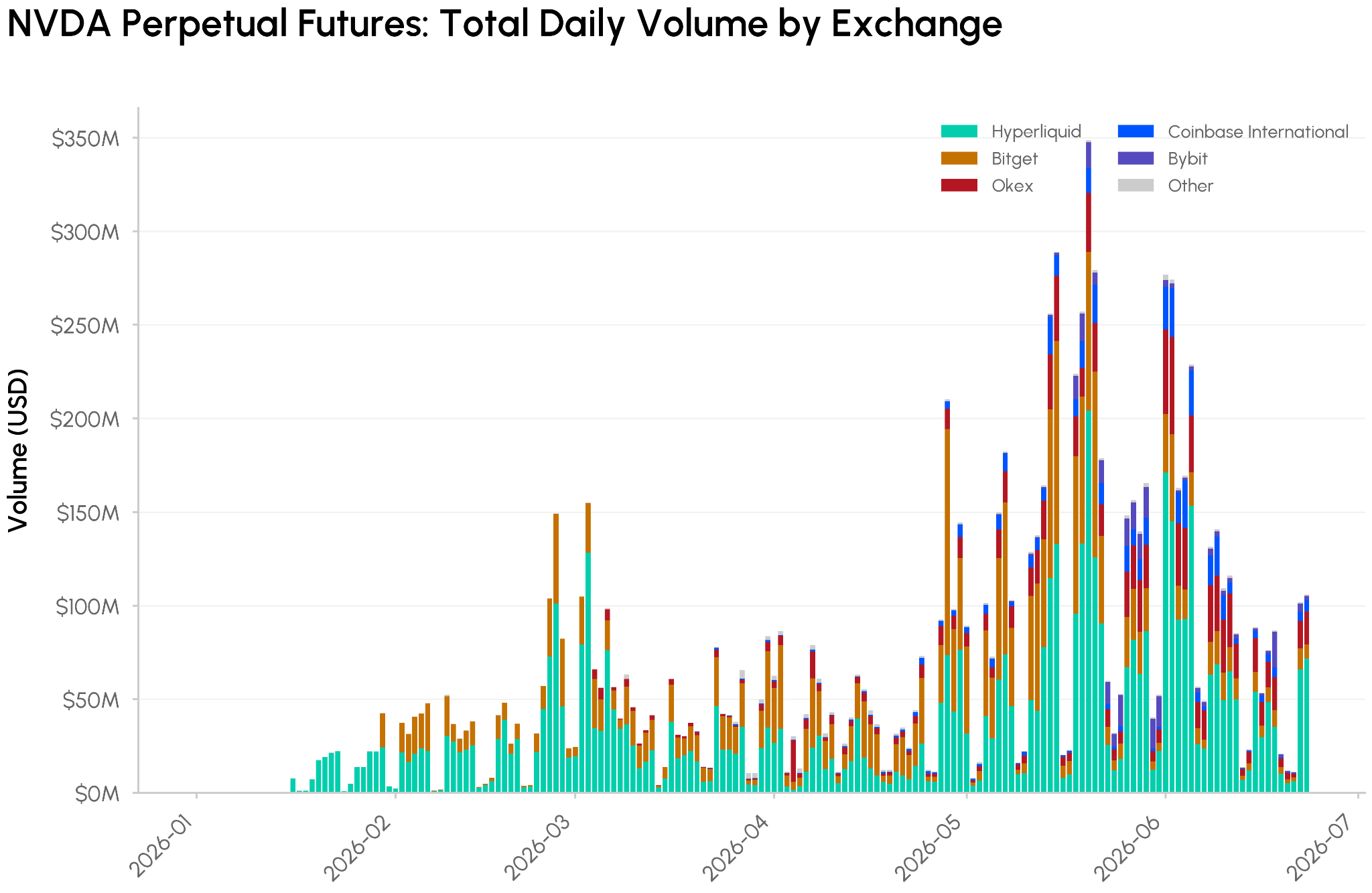

When compared with perpetual futures, the complexities of tokenized spot markets become clearer. Building a spot market for an asset requires the exchange or pool to hold the underlying asset as inventory for settlement. Perpetual futures, by contrast, are cash or stablecoin settled and do not require custody of the underlying stock, making it faster and cheaper to bootstrap liquid markets.

Source: Talos CM Market Data Pro

Perpetual futures experience significantly more trading volume than tokenized spot markets. For Nvidia, the average Mon–Fri trading volume is around $154M and the average weekend trading volume is around $29M, with around $6.3B in total trading volume across these venues. This is more than 40x the volume of spot markets. Traders seeking short‑term price exposure to Nvidia can trade these contracts without navigating issuer structures, custody models, or redemption mechanics, which helps explain why perp markets currently dominate onchain NVDA activity.

Conclusion

The market for tokenized stocks is still early, but the diversity of models already visible onchain reflects how quickly the landscape is developing. The same stock can now be held as a registered security entitlement, a custodial wrapped token, or a perpetual futures contract, each offering a different combination of legal rights, market access, and capital efficiency.

As the data shows, these differences are not theoretical. They show up in pricing, liquidity, trading patterns, and redemption rights. For market participants, the key question is no longer whether a stock is available onchain, but what kind of claim a given instrument represents, and how that structure shapes its liquidity, pricing, and trading dynamics.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.