Does Timing Matter When Trading BTC?

Introduction

Evidence from Market Impact Modeling

Tl;dr

If you’re executing, say, a 5 BTC order and have flexibility on timing, here’s what 90 days of simulation data tells us: Trade between 11 AM and 1 PM UTC, use a 10- to 15-minute VWAP duration, and avoid late-night hours. This optimal combination can reduce expected market impact by several basis points compared to suboptimal timing. For larger positions, that translates to meaningful cost savings. Moreover, with passive-first execution strategies, you can trade more cheaply than simply crossing the spread. The data shows a clear pattern: for a 5 BTC order on the consolidated BTC-USDT orderbook, timing decisions have measurable impact on execution costs.

Introduction: The hidden cost of timing

Institutional cryptocurrency traders managing billions of dollars face a deceptively simple question with billion-dollar implications: When should I trade, and for how long? The answer matters more than you might think. A 5 BTC order executed at 2 AM versus 2 PM can differ by several basis points in expected market impact. For a $10 million position, that’s thousands of dollars in execution costs—money left on the table simply because of timing decisions.

Consider a few common scenarios: a risk manager needs to unwind flow during a settlement cycle with a fixed window; a trader has balance sheet capacity to accumulate risk but needs to unwind it “at some point over the next few hours”; or an execution trader receives a portfolio manager’s instruction to “buy 5 BTC today” with the only constraint being “lowest expected impact.” In each case, the trader has creative freedom but needs data-driven guidance to exercise it effectively.

The question becomes: Given a trade size (say, buy 5 BTC), and given the freedom to trade anytime in the next 24 hours, what is the optimal time of day to trade, and what is the optimal duration? Should you trade at 5 AM or 7 AM? Should you use a duration algorithm like VWAP or TWAP? Over 5 minutes or 35 minutes? Should you just cross the spread? These decisions matter, and the difference can be measured in basis points and dollars. To answer this question, we leverage the Talos Market Impact (TMI) model, which decomposes execution costs into physical impact and time risk components. As detailed in our previous work, the TMI model is empirically calibrated on over 50,000 parent orders and 50 million child orders across the top 60 spot and perpetual contracts, providing institutional-grade estimates of expected slippage from arrival price (the time at which an order is submitted for trading, see more in this article). The model uses execution alphas – forward-looking predictions of spread, volume, and volatility – to estimate impact before committing capital.

In this blog post, we combine the TMI model with historical BTC-USDT market data to simulate tens of thousands of execution scenarios, empirically estimating a 5 BTC order’s expected impact across different time-of-day windows and execution durations. What we found was surprising..

1. What we found: The impact profile

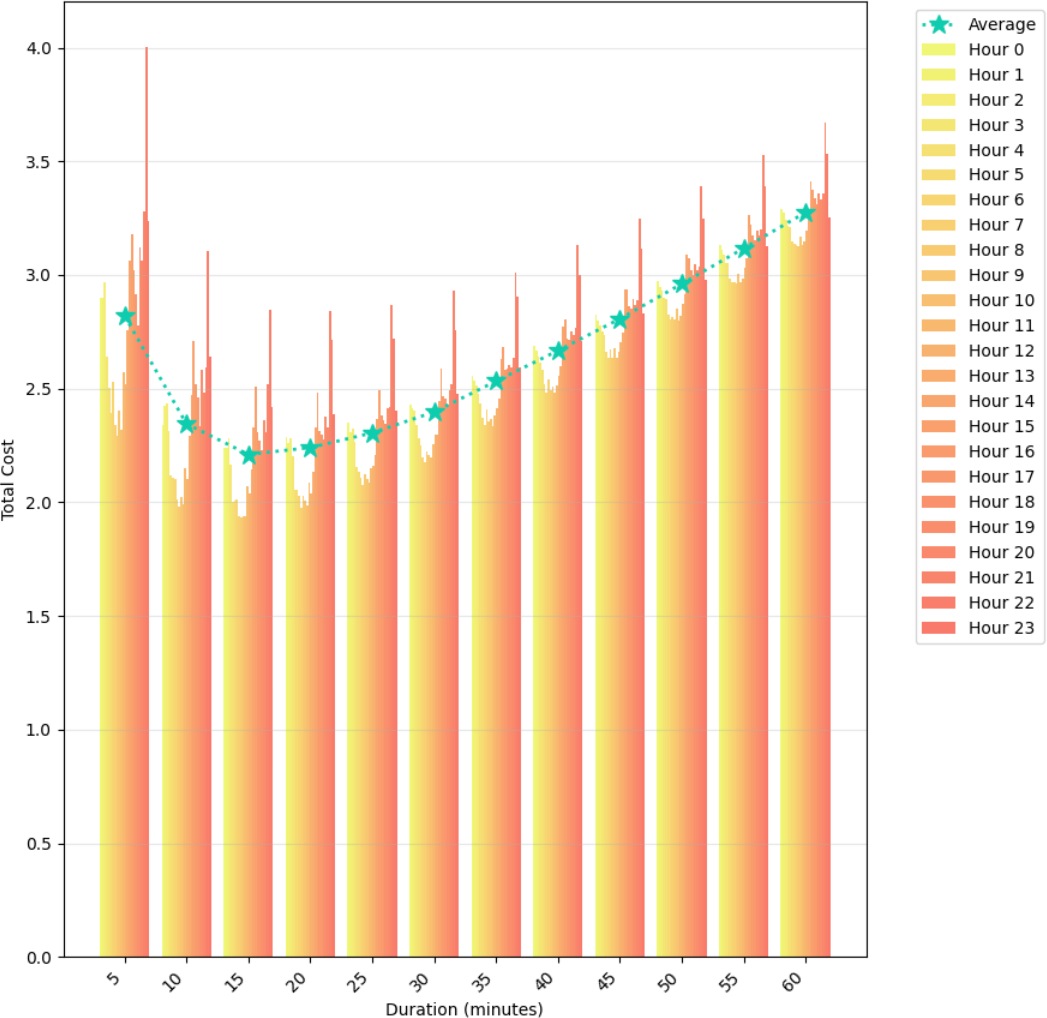

Before diving into the methodology, let’s look at what the data reveals. Figure 1 shows the results of simulating tens of thousands of execution scenarios over a 90-day period, using consolidated BTC-USDT tape market data across 50+ public exchanges.

The x-axis represents VWAP trade duration, ranging from 5 minutes to 60 minutes in 5-minute increments. The y-axis shows expected impact in basis points. Each colored bar represents the average impact, as measured by the Talos Market Impact (TMI) model, for executing 5 BTC at a specific hour-of-day (color-coded) over a given trade duration, aggregated over a 90-day historical period. The green line represents the average impact across all hours-of-day for each trade duration bucket.

The visualization reveals something immediately striking: a Nike-like pattern in the green average line, with a clear optimal duration around 10–15 minutes. But that’s just the beginning. The color gradient tells another story; time-of-day matters dramatically, with midnight to 3 AM UTC and late evening hours (UTC) showing systematically higher impact than midday periods.

Methodology

For those interested in the methodology: We ran a simulation using consolidated BTC-USDT tape market data, including impact coefficients and execution alphas, across our 50+ public exchanges. Over a 90-day period, we computed for every time-of-day (UTC) and every trade horizon (5 to 60 minutes) the expected impact, assuming execution using the Talos VWAP algorithm. For example, trading 5 BTC-USDT between 10:00 AM to 10:15 AM UTC yields 90 samples over 90 days, which we average to get a single data point. We repeated this across all time-of-day windows and duration options, creating a comprehensive map of expected impact.

2. Key insights: What the data reveals

There are several key intuitions that can be drawn from this visualization:

1. Time-of-Day impact ( yellow to dark orange bars):

For a given VWAP execution duration, there’s a strong emerging pattern: trading is more expensive during midnight to 3 AM UTC or from 5 to 6 PM UTC to end-of-day, versus cheaper near midday (specifically 11 AM to 1 PM UTC). This creates a “smiley” curve that doesn’t directly follow the intraday volume pattern.

Here’s what’s interesting: The volume around the US equities market open (14:30 PM UTC) is on average twice as large versus any other time of day. You’d typically expect that to mean lower impact, but our analysis shows otherwise. Why? Volatility is also at its peak during that window and known in equities markets to be more “idiosyncratic” in nature – market opens, information dissemination, and the ability to express opinions tend to cause such volatility. Simply put: the volatility increase around that time supersedes the benefits of higher volume.

The lowest impact is typically found between 11 AM and 1 PM UTC.

2. Execution duration impact (green line): The 10- to 15-minute sweet spot

Going from left to right of the plot reveals something rather surprising: a Nike-like pattern with a clear convexity to the optimal duration, near the 10- to 15-minute range (lowest point approximately on the green curve).

This is the sweet spot. Why? It’s the interplay between expected participation rate (higher in shorter horizons on average) and volatility over the trade duration (time risk in our TMI model). When duration is low, participation rate influences temporary impact faster than the reduction in time risk. When duration is high, participation rate reduces but trade horizon risk rises faster, meaning larger risk impact versus the reduction in temporary impact.

The lowest impact is typically found at the 10- to 15-minute duration.

3. Peak impact: The late-night penalty

Trading during the last hours of the (UTC) day, denoted in the darkest orange bars of Figure 1, is systematically associated with larger market impact. The statistical conclusion is clear: trading relatively small order sizes at a dramatically larger proportion of expected volume may cause dramatic risk impact versus alternatives.

Avoid the late-night hours if you can. The data shows it consistently costs more.

4. You can trade more cheaply than crossing the spread!

The Talos Market Impact model is calibrated to include fees – our clients’ taker fees range from low single-digit to 10 bps, with 3 bps on average. Considering 3 bps taker fees, the analysis shows opportunities on the order of less than 2 bps, which include both the trade impact as well as the expected maker and taker fees. How’s that possible? Because maker fees are typically lower, and our duration algos (VWAP, TWAP, Quantizer and others) are designed to use a passive-first approach, which statistically does not require crossing the spread much, if at all.

You can trade more cheaply than crossing the spread!

3. Caveats and remarks

Several important caveats and remarks need to be outlined:

- Asset and order size specificity: It is likely to assume that these patterns and shapes are not consistent with every crypto asset, or any order size. This is why we developed a Pre-Trade tool that would allow you to evaluate expected impact scenarios in real time, at the point of trade time (see video in this blog).

- Further analysis opportunities: Further analysis could examine larger time windows, further idiosyncratic filters, and further decomposition of such metrics (expected participation rate, impact decompositions and more). This analysis just scratches the surface of our capabilities, which we are building and quickly incorporating into our platform.

- Bespoke venue analysis: Another more bespoke analysis can be done on a curated sublist of liquidity venues, tailoring such metrics to your exact liquidity spectrum (reach out to your Talos representative or to me directly to learn more).

Conclusion: From insight to execution

This simulation analysis demonstrates something powerful: when you have the freedom to choose when and how long to trade, data-driven optimization can meaningfully reduce execution costs. The difference between trading at 2 AM versus 2 PM, or using a 5-minute versus 35-minute duration, isn’t just academic – it’s measurable in basis points, and for large positions, that translates to real dollars.

The key takeaway: The 10 to 15-minute window, executed during midday hours (11 AM–1 PM UTC), represents the optimal timing for minimizing expected market impact, assuming a 5 BTC order executed against the BTC-USDT consolidated orderbook. But more importantly, this analysis shows that timing decisions shouldn’t be left to intuition or guesswork. The Talos Market Impact model, combined with execution alphas and consolidated tape data, provides the foundation for making these decisions with confidence.

At Talos, we’re building these capabilities directly into our execution infrastructure. Our Pre-Trade tool will make sophisticated scenario analysis accessible to institutional traders in real time, allowing you to evaluate expected impact scenarios before committing capital. The future of crypto execution isn’t just about speed or shiny UIs (we have those too) – it’s about informed decision-making that balances cost, risk and the creative freedom that comes with quantitative guidance.

The $3 trillion crypto market is maturing. It’s time execution decisions caught up with the data. At Talos, we believe you should focus on what to trade. Let us help you with the how.

➡️ For more information about the Talos Market Impact Model, download the full research paper here or read the summary blog here.

➡️ To learn more about Talos’s Quantitative Execution Services, contact us.

About the Author

Eliad Hoch is the Head of Quantitative Execution Services at Talos, the premier provider of institutional digital asset technology and data for trading and portfolio management. Based in London, he oversees the front-office lifecycle of algorithmic trading, guiding clients through slippage minimization tactics, trade scenario analysis and TCA, while overseeing the quantitative trading strategies offered by the firm. Prior to Talos, Eliad spent 2 years as the Founder of GONLabs, a systematic crypto trading hedge fund, focused on quant and machine learning-driven crypto strategies. Before that, he spent 12 years in the equities, futures and FX markets at Bank Of America Merrill Lynch and Goldman Sachs in portfolio algorithmic execution, quant modeling, central risk trading and systematic internalization market making. Eliad has co-authored several papers on systematic trading strategies and market impact, and published a 2024 paper exploring tokenomics design and DeFi value propositions. He is a guest lecturer at various UK universities on algo trading and quant modeling. Eliad holds a masters in computational finance and artificial intelligence from the University of Southampton, where he received first class honors and the top independent research award.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.