Is OpenUSD a Threat to the Dominance of Circle and USDC?

State of the Network #371

Is OpenUSD a Threat to the Dominance of Circle and USDC?

Introduction

State of the Network #371

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- OpenUSD challenges the traditional issuer model by redistributing reserve income to a 140+ partner network, putting pressure on Circle’s margin rather than immediately displacing USDC supply.

- USDC remains deeply embedded as a high‑velocity stablecoin, settling around 79% of roughly $38T in on‑chain transfer volume in 2026 while anchoring liquidity across major exchanges, DeFi money markets, and perp venues.

- Circle’s distribution partnerships (e.g., Coinbase, Hyperliquid) and regulatory positioning reinforce USDC’s network effects, making it the preferred dollar rail for many venues and use-cases.

Introduction

On June 30th, Open Standard, a consortium of 140 payments companies and banks including Stripe, BlackRock and Coinbase announced the launch of Open USD (OUSD), a stablecoin backed 1:1 with USD reserves. Notably, Open USD distributes nearly all reserve interest back to the network of 140+ corporate partners rather than accruing to a single issuer such as Tether or Circle.

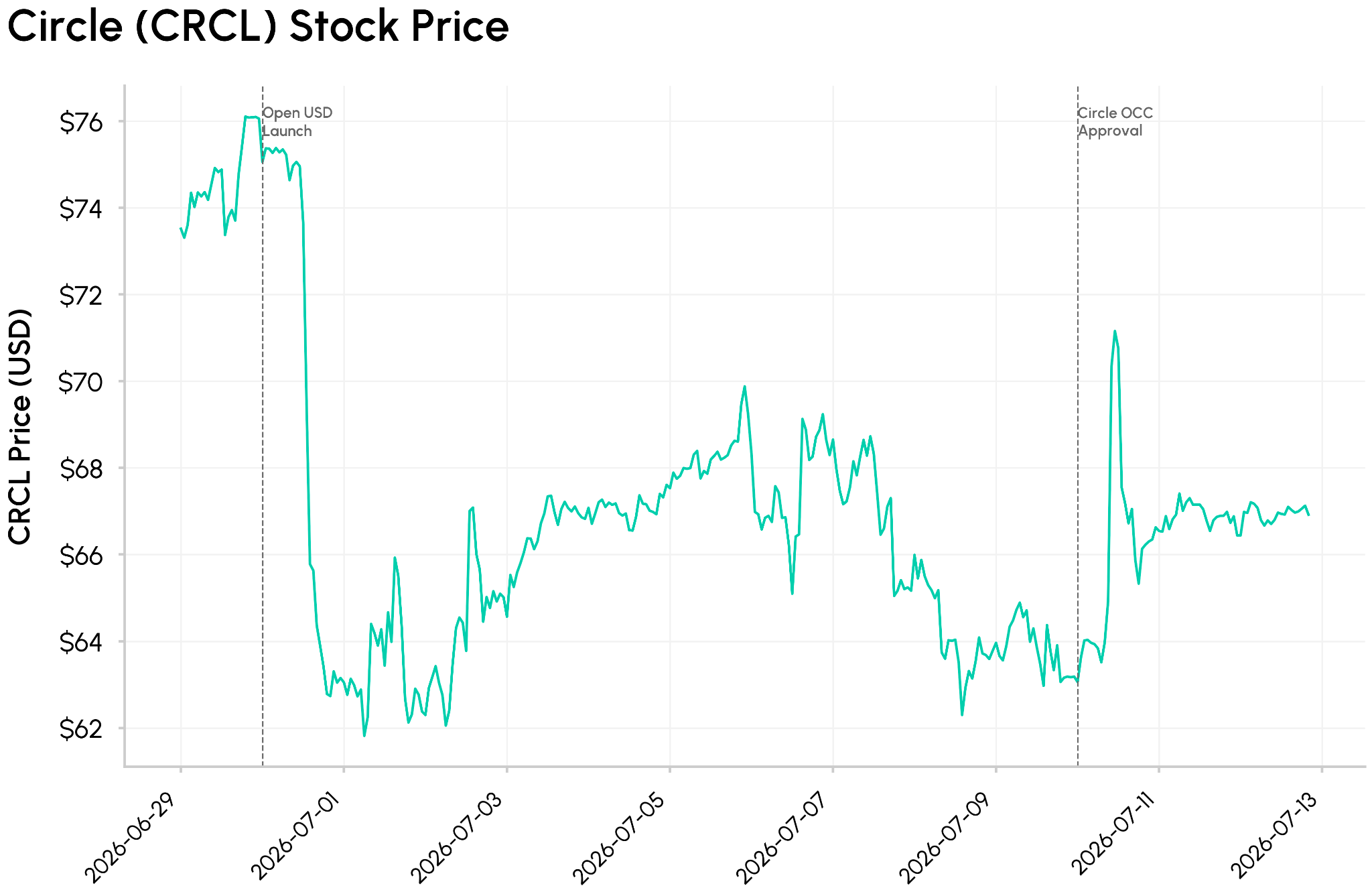

The news triggered a sharp selloff in Circle’s stock, with CRCL falling 17% on June 30th. More than a new stablecoin launch, OUSD represents a direct challenge to the traditional issuer model in which reserve income accrues primarily to the stablecoin issuer. Does OUSD pose a real threat to Circle’s margins and the entrenched network effects behind USDC’s dominance?

Source: Talos CM Market Data Feed

In this issue of State of the Network, we explore whether the launch of Open USD presents a structural threat to Circle’s business model and USDC network effects, or whether onchain data tells a different story than the equity market’s reaction.

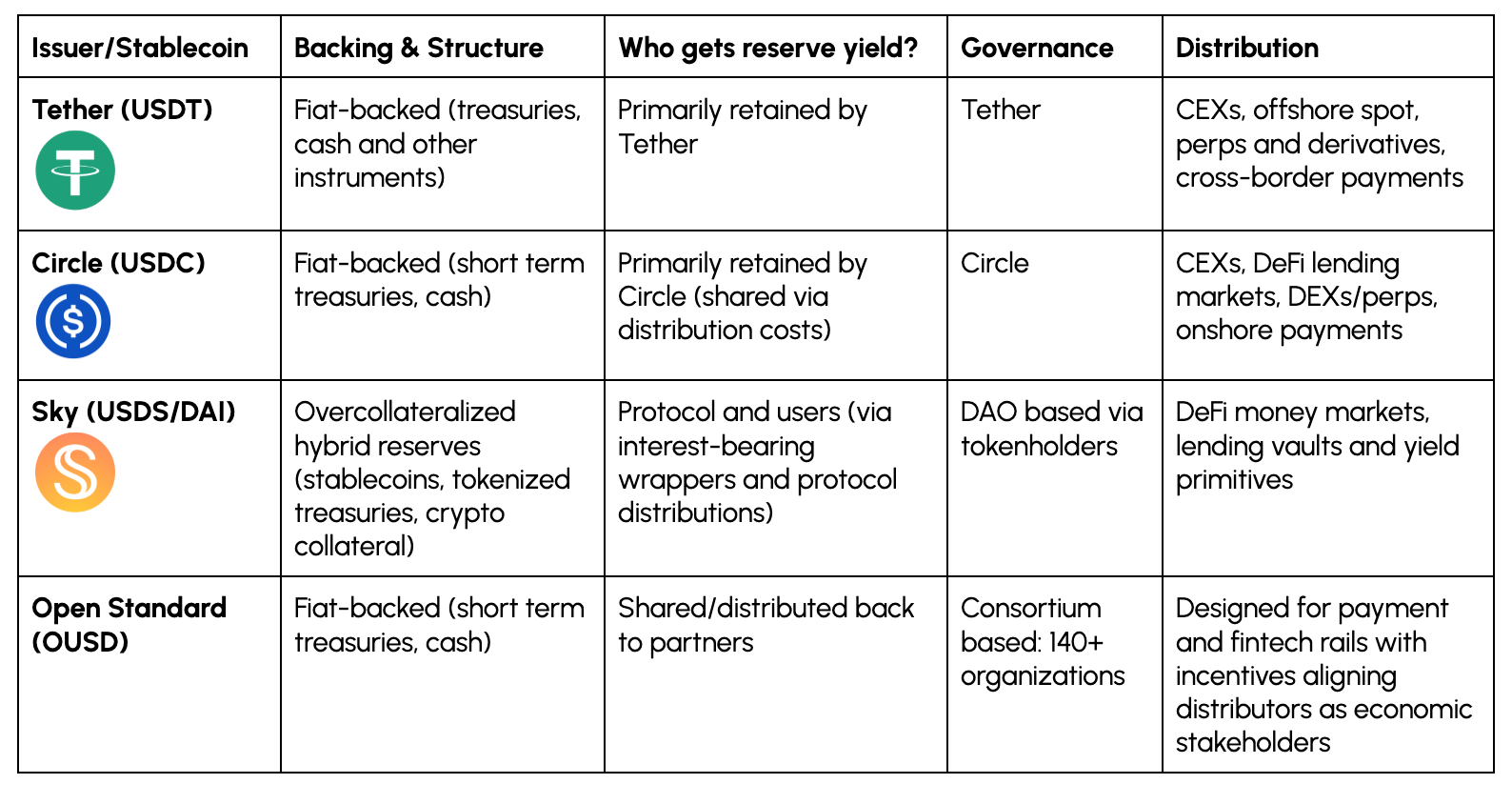

Stablecoin Issuer Models: Who Captures the Float?

Below, we map the economic models behind major stablecoins. One of the key differentiating factors among them is who captures the float or the interest income generated by their reserves.

For issuers like Tether and Circle, reserve income largely accrues to the issuer and drives the vast majority of their revenue. For Sky and Ethena, more of that value is passed through to users. OUSD introduces a third model, where reserve income is pushed out to the distribution network itself or companies that control the end-user distribution like fintech apps, exchanges, wallets, merchants and payment processors.

This distinction is becoming important as distribution emerges as one of key differentiators for stablecoins. Circle’s model is an example of how issuers share economics with key partners, most notably Coinbase, while OUSD makes this native to the model.

As we covered in our previous scenario analysis, Circle’s revenue is primarily driven by interest income on USDC balances. In FY 2025, 96% of Circle’s $2.7B in revenue came from reserve income. A large portion of this is shared in the form of distribution costs to partners like Coinbase. As a result, Circle’s Revenue Less Distribution Costs (RDLC) was around $1.08B, a useful measure of how much it retains after paying for distribution.

The Coinbase relationship is a clear example of how stablecoin value increasingly accrues to platforms that own the float rather than the issuer alone. This raises the question of whether the economic power dynamic is shifting from the issuer to the distributor network.

The Network Effects & Distribution Behind USDC

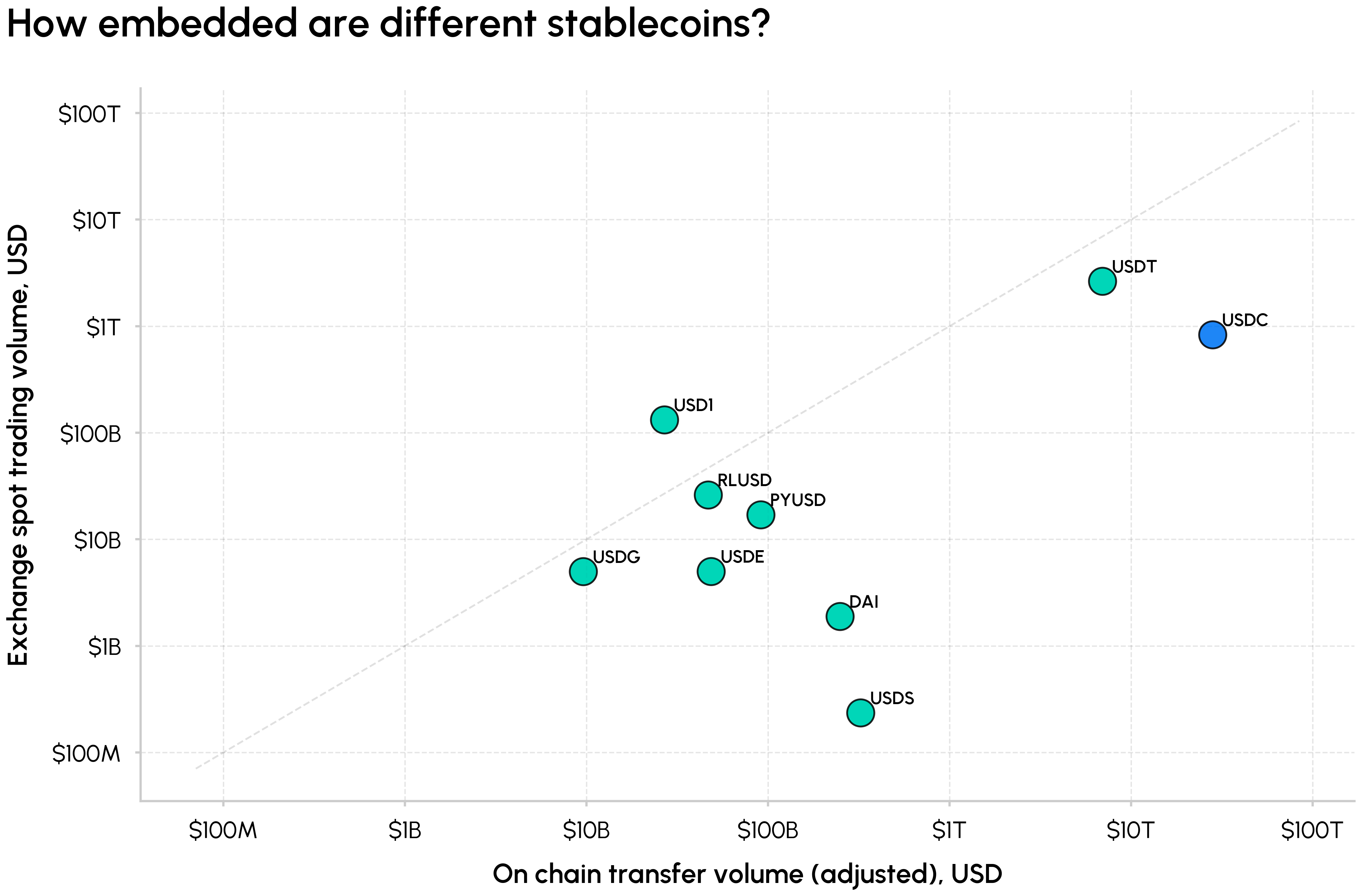

While dozens of stablecoins have flooded onto the market in recent years, it remains a duopoly with USDT and USDC commanding a ~86% share. Circle’s USDC accounts for ~23% of this, with a market cap of $73B. This scale was not achieved overnight, but as a byproduct of deep liquidity, regulatory edge and a wide footprint across chains and trading venues.

The chart below captures the scale of different stablecoins across two dimensions: (adjusted) on-chain transfer volume and exchange trading volume as of June 2026. USDT and USDC stand out with high settlement usage and deep trading activity, while USDS, USDe and PYUSD occupy more niche positions in the grid. Global Dollar (USDG), another consortium based stablecoin, has failed to gain similar traction so far.

Source: Talos CM Network Data Pro & Market Data Pro

USDC also settles the majority of on-chain transfer volume. In the first half of 2026, USDC settled ~79% of $38T in adjusted onchain transfer volume, with Base accounting for 69%. USDT accounted for $7T (~18%), showing that USDC turns over at a higher velocity than USDT despite its lower circulating supply.

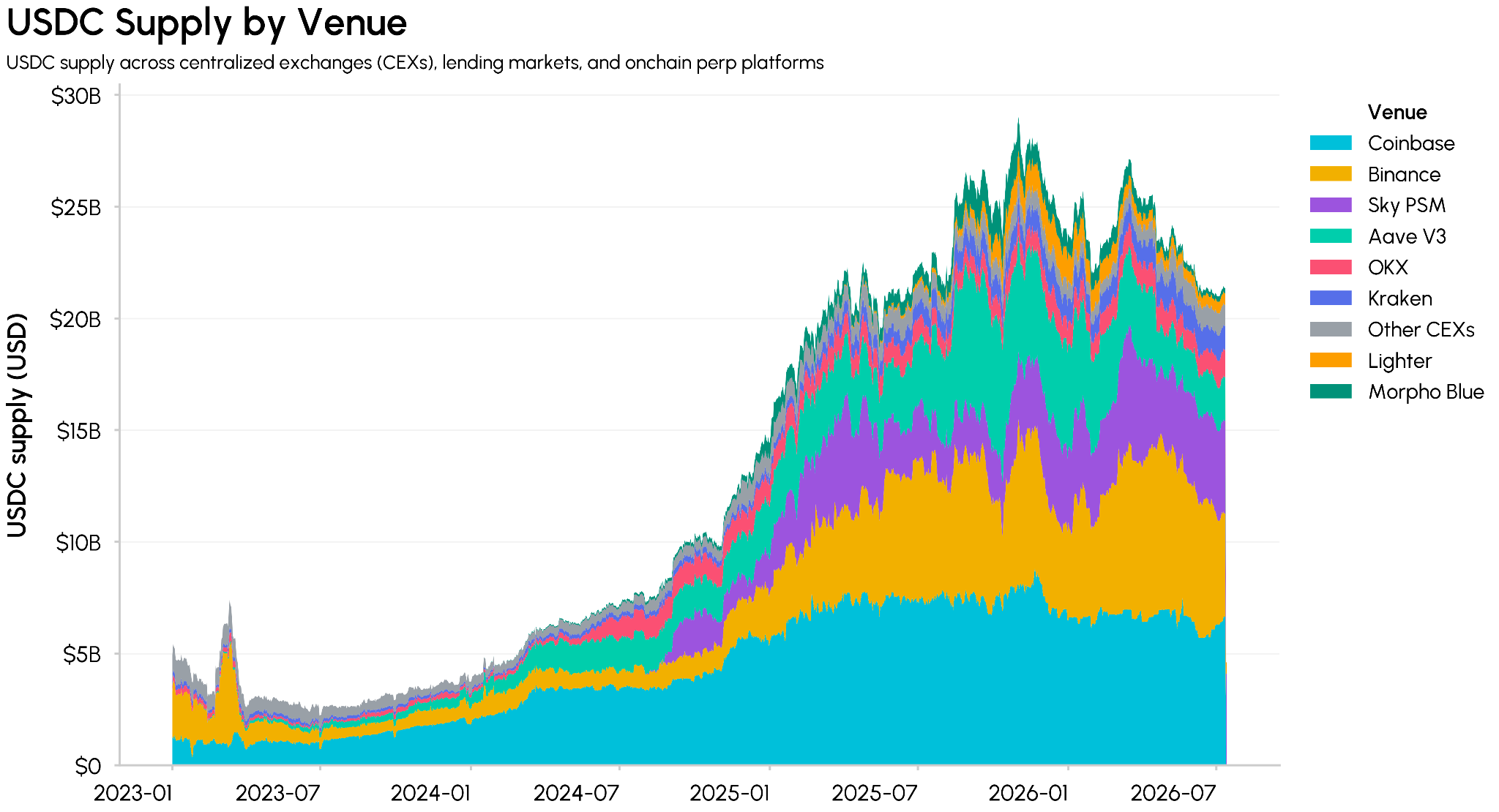

Where does USDC Supply Sit?

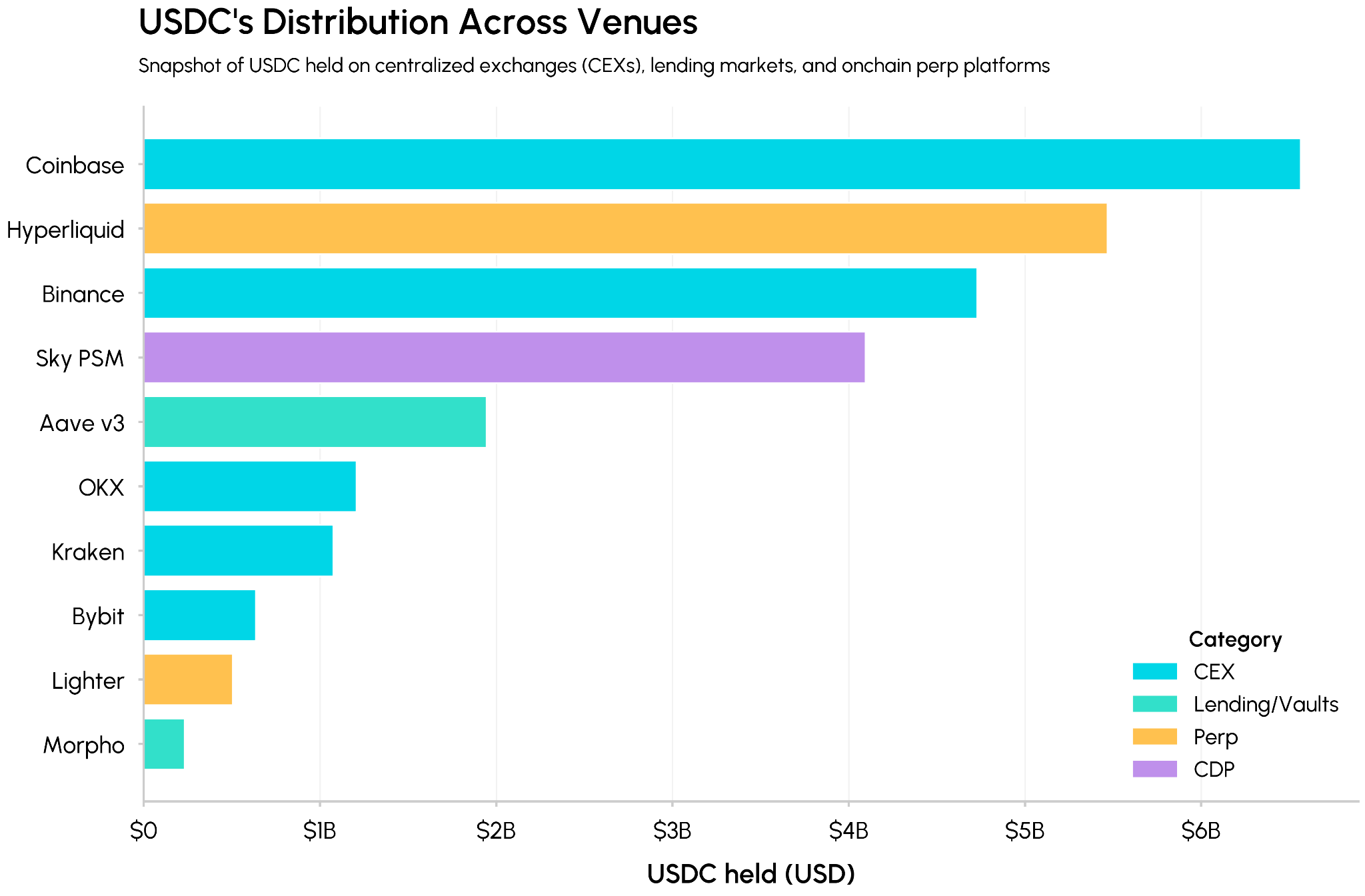

Below we look at where this USDC is actually held. On centralized exchanges, USDC serves as a major quote and settlement asset, while in DeFi it sits inside money markets, vaults, DEX liquidity pools and a collateral asset backing other stablecoins. Exchanges like Coinbase, and Binance hold several billions of USDC, with Hyperliquid, the Sky PSM and Aave v3 accounting for substantial on‑chain balances.

From the lens of Circle’s relationship with Coinbase, the shift in issuer economics becomes clearer. As Coinbase reported in its Q1 2026 earnings, roughly 25% of USDC’s circulating supply sits in Coinbase products. That footprint has allowed Coinbase to capture around half of USDC’s economics by driving deeper integration and adoption, rather than ceding most of value to Circle.

Source: Talos CM Network Data Pro (*note: Centralized exchange balances include tagged Ethereum and Base exchange wallets)

Hyperliquid is one of the clearest recent examples. In May 2026, Coinbase became the official USDC treasury deployer on Hyperliquid and Circle became the technical deployer, reinforcing USDC as the platform’s native stablecoin. Under AQAv2, Hyperliquid can capture up to 90% of the reserve yield generated by USDC balances on its platform, redirecting an estimated $135–$160M in annual income away from Circle and Coinbase and into HYPE token buybacks and the protocol’s ecosystem.

This shows how USDC is embedded in fast growing centers of market activity including on-chain perp DEXs like Hyperliquid and Lighter where the default quote asset can shape liquidity, collateral preferences, and other integrations. It also illustrates how issuer and distributor economics are already intertwined: platforms like Coinbase and Hyperliquid are no longer just venues that hold USDC, but key economic participants in the USDC float.

Source: Talos CM Network Data Pro & ATLAS

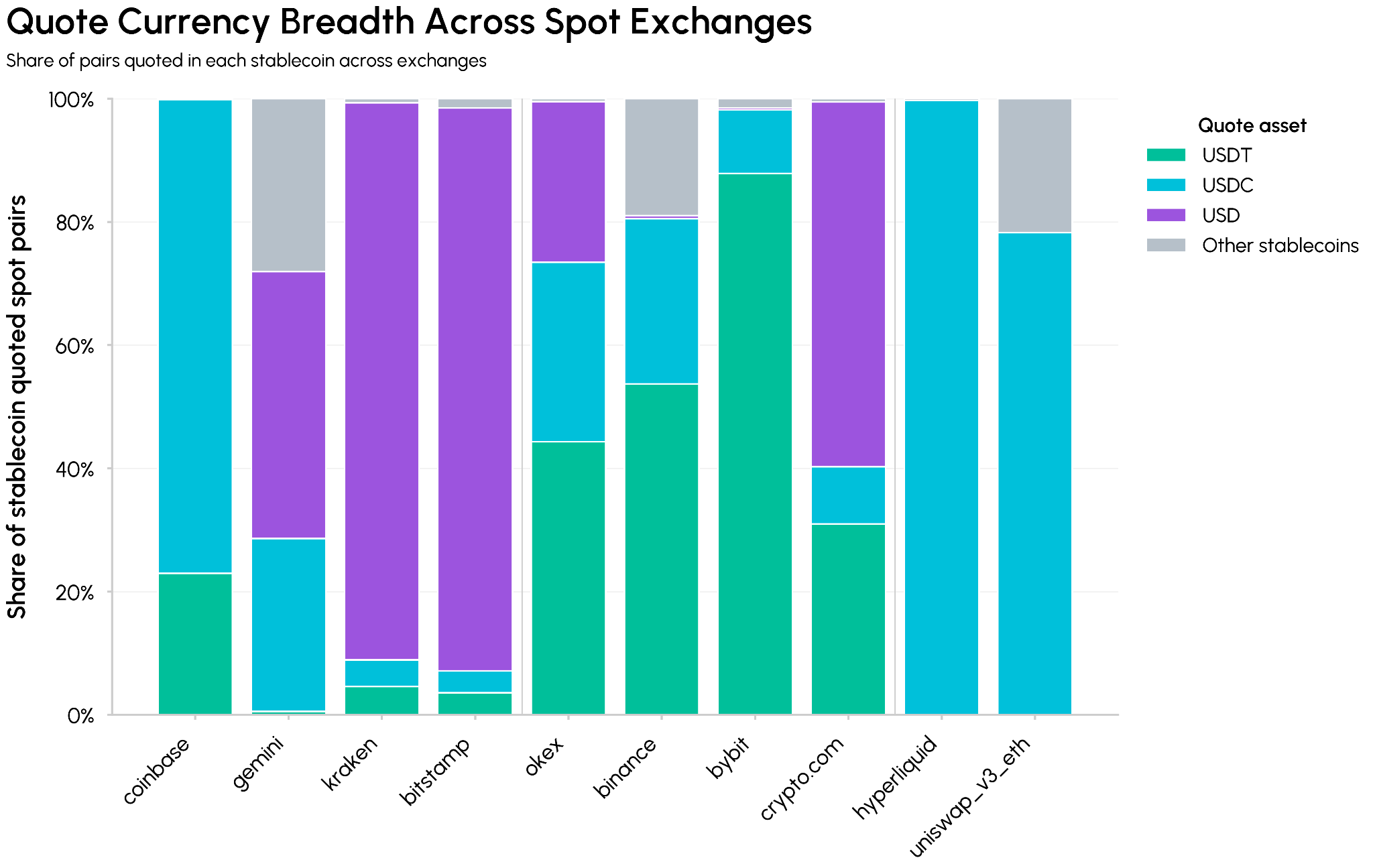

Onshore Dominance & Regulatory Edge

Stablecoin dominance is also a result of depth and breadth of liquidity. The chart below compares quote‑asset breadth across spot exchanges for USDT, USDC, and other stablecoins. On offshore venues like Binance, Bybit, and OKX, USDT still anchors the vast majority of stablecoin‑quoted markets.

Onshore and regulated exchanges like Coinbase, Gemini, Kraken, Bitstamp, and Crypto.com lean heavily on USD and USDC pairs, with Coinbase unifying USD/USDC books. USDC is also the dominant quote asset in onchain venues like Hyperliquid and Uniswap v3, integrating it directly into perp and DeFi liquidity.

In parallel, Circle has now received approval from the OCC to open Circle National Trust, a national trust bank that can ultimately hold and manage USDC reserves under federal oversight. This further cements Circle’s regulatory edge of being a dollar rail that exchanges, protocols, and payment providers are comfortable building around.

Conclusion

The competitive landscape for stablecoins is evolving around who earns reserve income, how deeply different stablecoins are embedded in market infrastructure, and the regulatory frameworks around them. Open USD is best understood as a consortium governed shared‑yield network rather than a direct attack on USDC’s existing supply, putting pressure on the economics that support that supply.

The core idea is that reserve income will shift from issuers to payments networks, wallets, exchanges and other distribution channels that drive adoption. Whether that shift is strong enough to overcome USDC’s deep liquidity, wide footprint and regulatory edge remains to be seen.

Subscribe and Past Issues

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.