Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- Strategy sold 3,588 BTC between June 29 and July 5 to pay preferred share dividends and build up its USD Reserves. This is only the third and fourth sale of BTC since they began buying BTC in August 2020.

- Strategy’s STRC preferred share structure can cost Strategy $1.26B in annual dividends. STRC is currently around 10% below par and earns a variable 12% dividend rate, incentivizing increased dividend rates and making payouts more expensive.

- Strategy’s BTC purchase and sale price can be improved by executing trades across exchanges and markets. Binance-USDT market has the deepest order book with 2,900 BTC within 10% of the midprice.

Introduction

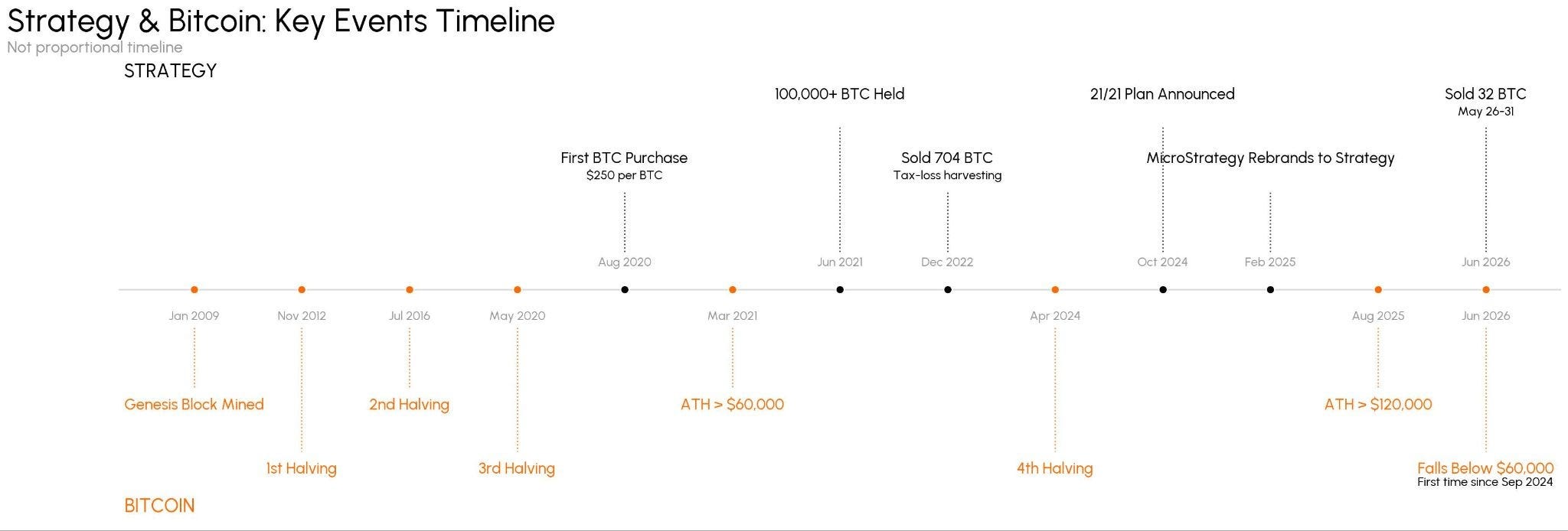

MicroStrategy was founded in 1989 as an enterprise software company. In 2020, MicroStrategy recognized its cash reserves were at risk of devaluation due to rapid inflation. It decided to hedge against the inflation risk by investing its cash in BTC.

In an 8K filing on July 6, Strategy sold BTC for only the third and fourth time since buying BTC in 2020. Strategy’s complex capital structure requires dividends payments to preferred shareholders and managing convertible debt while continuing to stockpile BTC. In this State of the Network, we dive into STRC’s role within Strategy’s preferred share capital structure, why Strategy is selling BTC, and how Strategy can improve trade execution to maximize BTC value.

Strategy’s Strategy

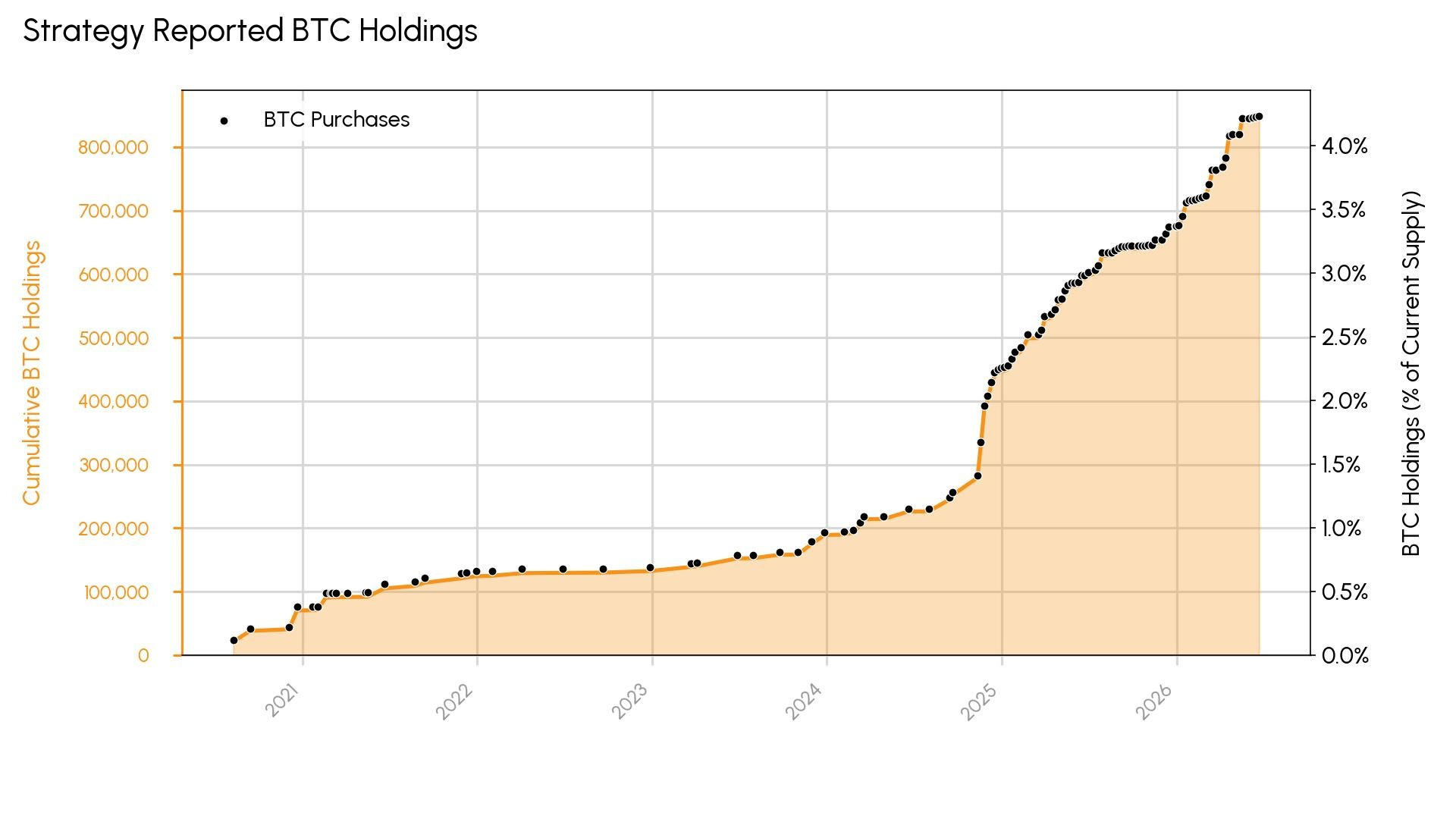

MicroStrategy rebranded to Strategy in 2025. Since their initial investment, Strategy has accumulated 843,775 BTC through debt and equity financing. Because Strategy finances its BTC purchases, the company acts as leveraged exposure to BTC. The company pioneered the strategy of acquiring a significant supply of a cryptoasset – others today are known as Digital Asset Treasuries or DATs.

Source: Talos CM Asset Profiles & SEC Filings

MSTR’s Layered Capital Stack

Strategy has multiple structured products that finance BTC purchases. Issuing convertible bonds enables MSTR to finance BTC purchases without immediately diluting common equity. Convertible bonds are priced as a combination of fixed-income security and upside from equity conversion. This functions as a call option; if MSTR price increases above the strike price, bondholders can convert to shares, earning additional returns. Only the 2032 bonds have a coupon payment greater than 1% at 2.25%. The other five convertible bonds have an interest rate of less than 1% or zero. This limits Strategy’s costs to focus on accumulating BTC.

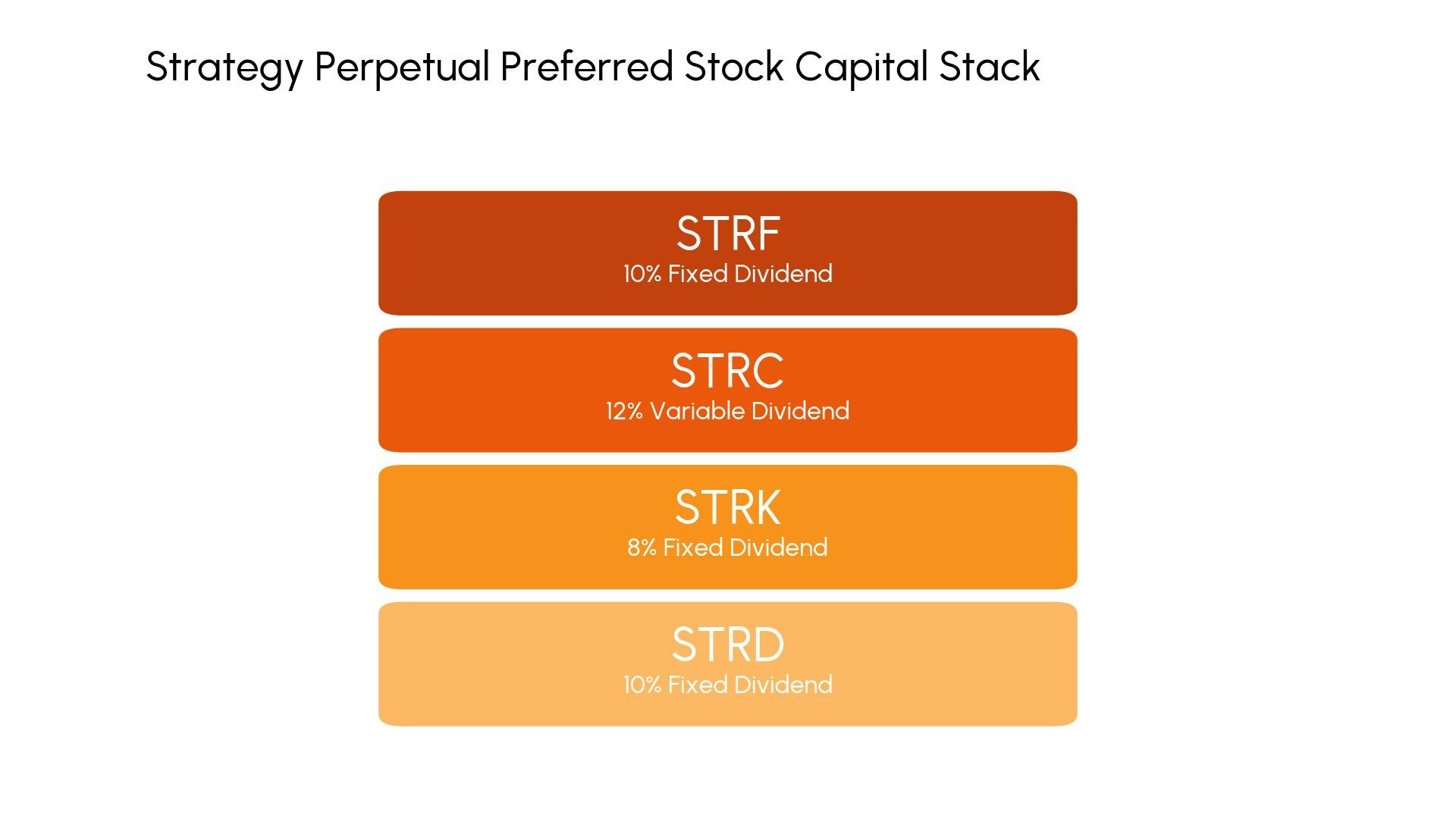

In October 2024, Strategy announced its “21/21 Plan” to finance BTC purchases by issuing $21 billion of debt and $21 billion of equity. This financing, over time, has led to Strategy offering four different types of U.S.-denominated perpetual preferred stock: STRF, STRC, STRK, STRD.

Source: Strategy

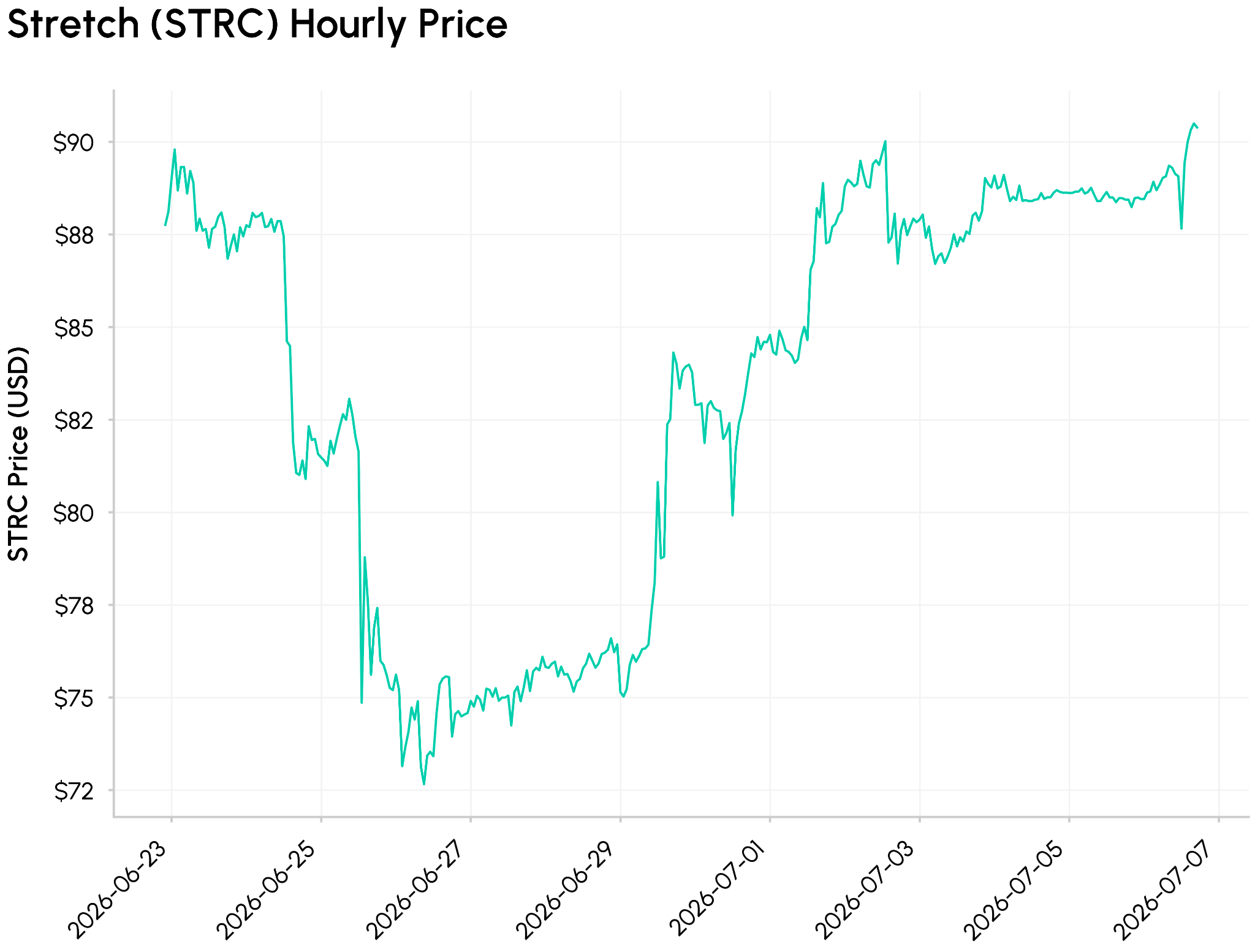

Strategy’s STRC stock, known as “Stretch”, has gained attention for its variable dividend. STRC is a perpetual preferred stock providing semi-monthly dividends. STRC dividend rate adjustments are considered on a monthly basis to incentivize STRC trading around par value of $100.

Source: Talos CM Market Data Pro Hyperliquid Candles

If STRC trades below $95, Strategy recommends a 50 bps increase in dividend rate. Trading between $95 and $99, Strategy recommends a 25 bps increase in dividend rate. Trading above $101, Strategy recommends a 25 bps decrease in dividend rate.

Source: SEC Filings

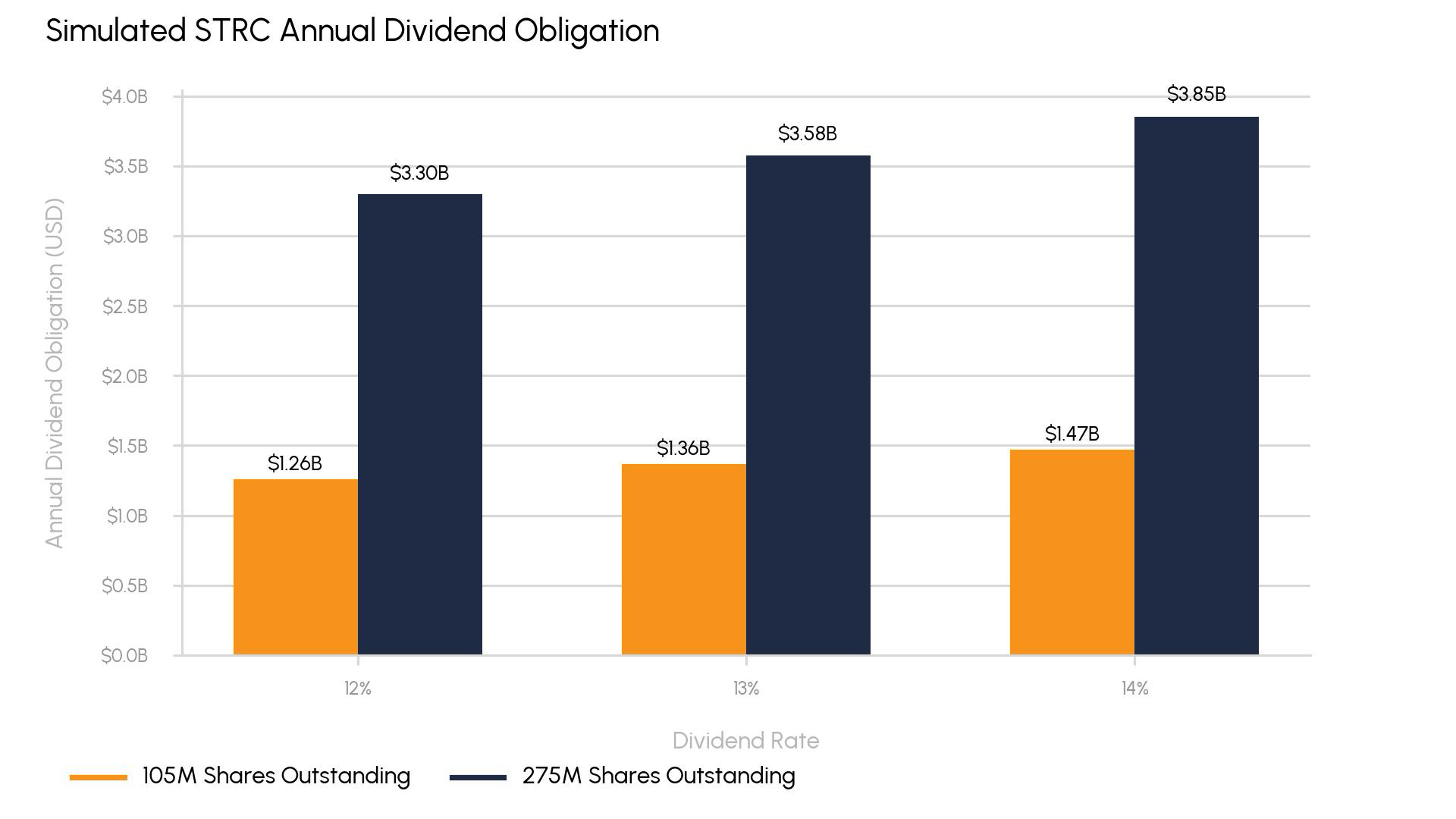

Most recently, the annualized dividend rate was raised to 12.00% after STRC fell to a low of ~$73, about 27% below par in late June. Assuming stable shares outstanding of 105 million shares, this costs Strategy $1.26B per year. The 275M share scenario reflects STRC’s remaining issuance capacity being fully used. STRC faces competition from Strive’s SATA preferred shares which currently pays an annualized 13% dividend rate. This competition could lead to more dividends paid by Strategy to retain investor interest.

Convertible bonds and preferred shares have priority of assets in the event of bankruptcy. Because these products have greater protection in such an event, they take on less risk and are compensated less. MSTR stock has the biggest potential upside due to Strategy’s leveraged exposure to BTC: investors are taking on the most risk and are at the bottom of the capital stack.

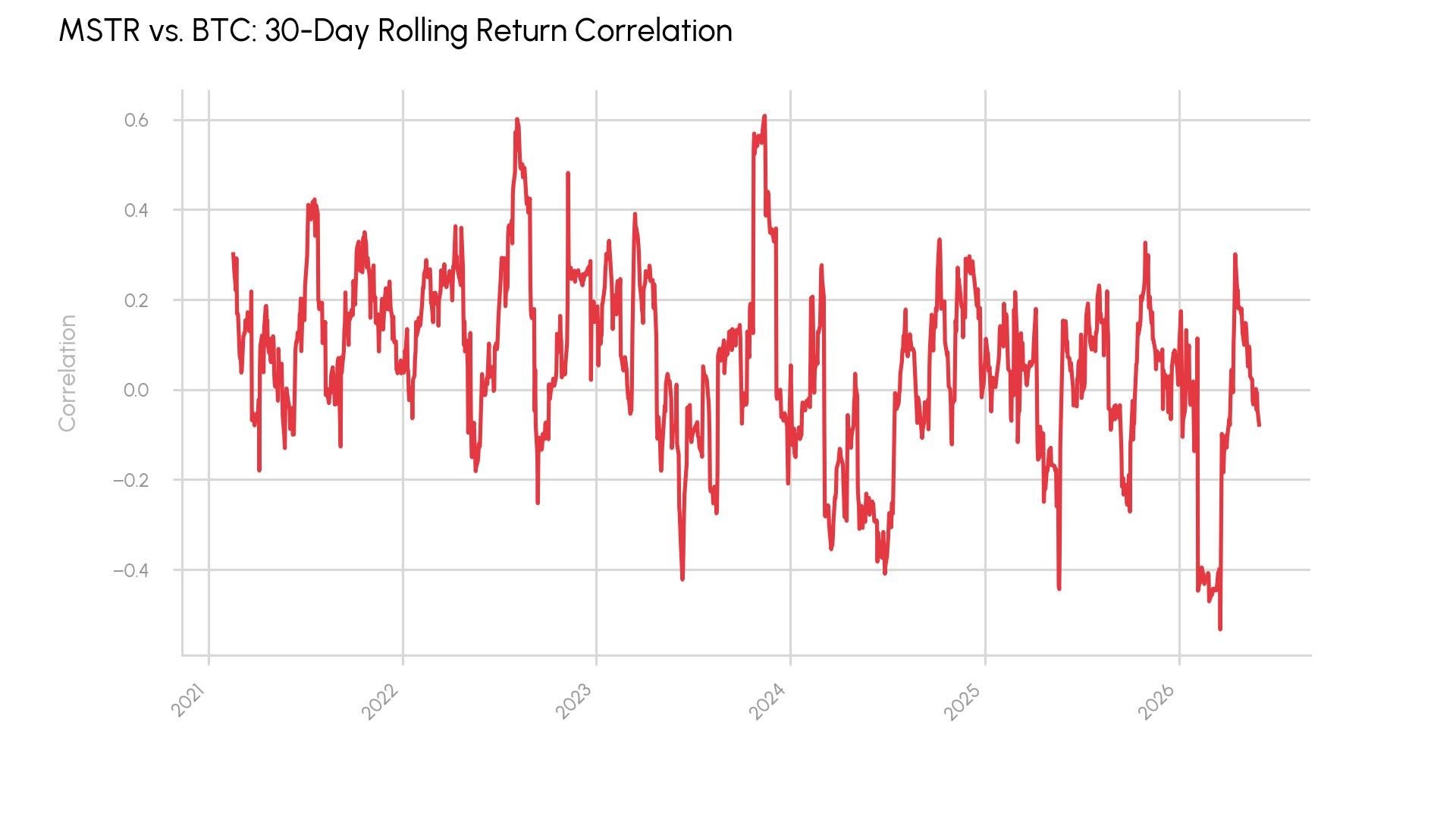

Source: Talos CM Network Data Pro & Yahoo Finance

Strategy focuses on the metric Bitcoin per Share (BPS). BPS calculates the total BTC in sats per share outstanding assuming all convertible bonds, convertible preferred shares, stock options, and other stock incentives are exercised.

MSTR returns show a weak positive correlation of 0.09 with BTC returns. This weak correlation does not reflect MSTR’s exposure to BTC, so there must be other factors driving the stock price.

One of these factors is the company’s operational risk. Strategy must continue to pay dividends on preferred shares in perpetuity and settle its outstanding convertible notes. Strategy’s primary focus is acquiring Bitcoin, but holding the asset does not generate revenue to consistently pay a growing number of creditors. Strategy’s software services only generated $124m in revenue in Q1 2026. How can Strategy pay back creditors while it focuses on financing BTC purchases?

“Never sell your Bitcoin.”

In February 2025, Strategy CEO Michael Saylor posted on X to “Never sell your Bitcoin.”. Up until then, Strategy had only sold 704 BTC once in December 2022 to offset capital gains. Between May 26 and May 31, 2026, however, Strategy announced the sale of 32 BTC. Between June 29 and July 5, 2026, Strategy sold 3,588 BTC. These sales are 0.42% of MSTR’s total BTC holdings and generated $218.5 million. Selling BTC is uncharacteristic of Strategy, why is it selling?

Source: Strategy Purchases & SEC Filings

The proceeds of these sales were used to pay dividends to preferred shareholders and refill the USD Reserve, a cash buffer Strategy holds to cover preferred dividend payments. The BTC sale is minimal and not necessarily a sign of distress. Strategy reported three BTC purchases totalling 3,657 BTC in June.

BTC Monetization

The USD Reserve was established in December 2025 to pay dividends on preferred shares. The USD Reserve is primarily funded by issuing MSTR stock through its at-the-market offering program. As of June 28, Strategy projects its USD Reserves of $2.55B provide 17.4 months of coverage on all preferred stock dividends and coupon payments. Last week, Strategy approved its Bitcoin Monetization Program which allows selling up to $1.25 billion BTC to fund the USD Reserve. This suggests Strategy will need to actively manage its balance sheet, using BTC sales alongside share issuance.

In June 2026, Michael Saylor spoke at Goldman Sachs’ Digital Asset Conference in London and highlighted BTC’s growing role as collateral to create “digital credit”. Saylor said using BTC as collateral has financed the purchase of 175,000 BTC throughout market downturns. Strategy is developing ways to use BTC as a collateral asset or resource for dividends to shareholders.

How Can Strategy Maximize its BTC Purchases and Sales

If Strategy continues to fund dividends by selling BTC, gradual selling over time and across exchanges can improve realized profit. This Bitcoin Monetization Program enables Strategy to sell up to $1.25B in BTC, which at BTC’s price of $63,500 is ~20,000 BTC or 2% of its current holdings.

Selling Across Exchanges Reduces Price Impact

Trading BTC across exchanges can reduce price impact and prevent slippage. Exchanges can vary in midprice and order book depth, enabling arbitrage opportunities. Arbitrageurs can buy BTC low at one exchange and sell at a higher price at another to capture this spread.

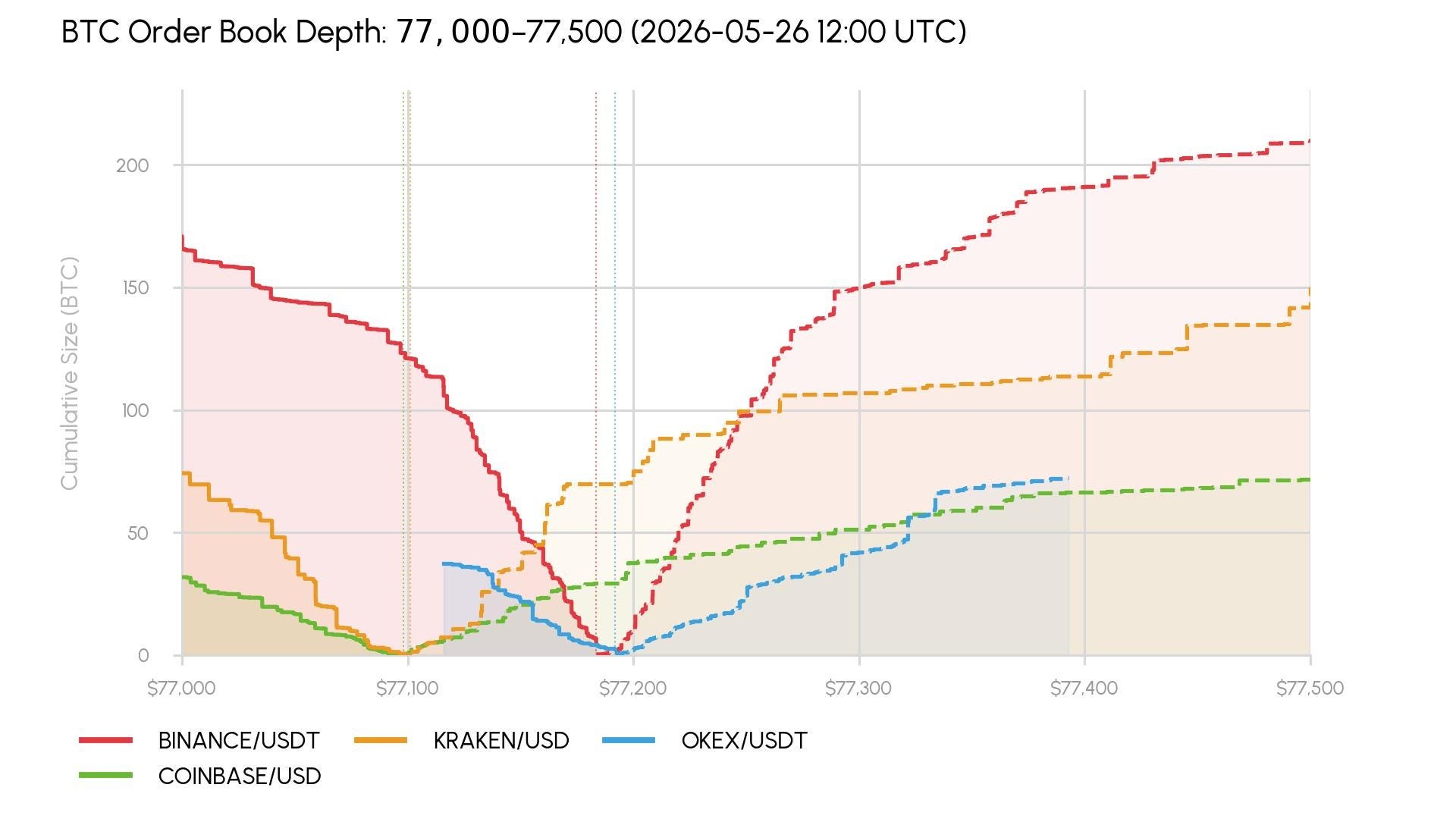

Source: Talos CM Market Data Pro

Examining around the time Strategy could have sold its 32 BTC, reporting an average price of $77,135, we took a snapshot of four BTC order books with the deepest liquidity around 1% from their midprice. All four are very different. The Binance-USDT order book has 2,900 BTC, twice as much as Coinbase, the second deepest order book. To move BTC from 0.1% to 1% from the midprice, Binance-USDT requires 300 BTC whereas OKEX-USDT only requires 40 BTC.

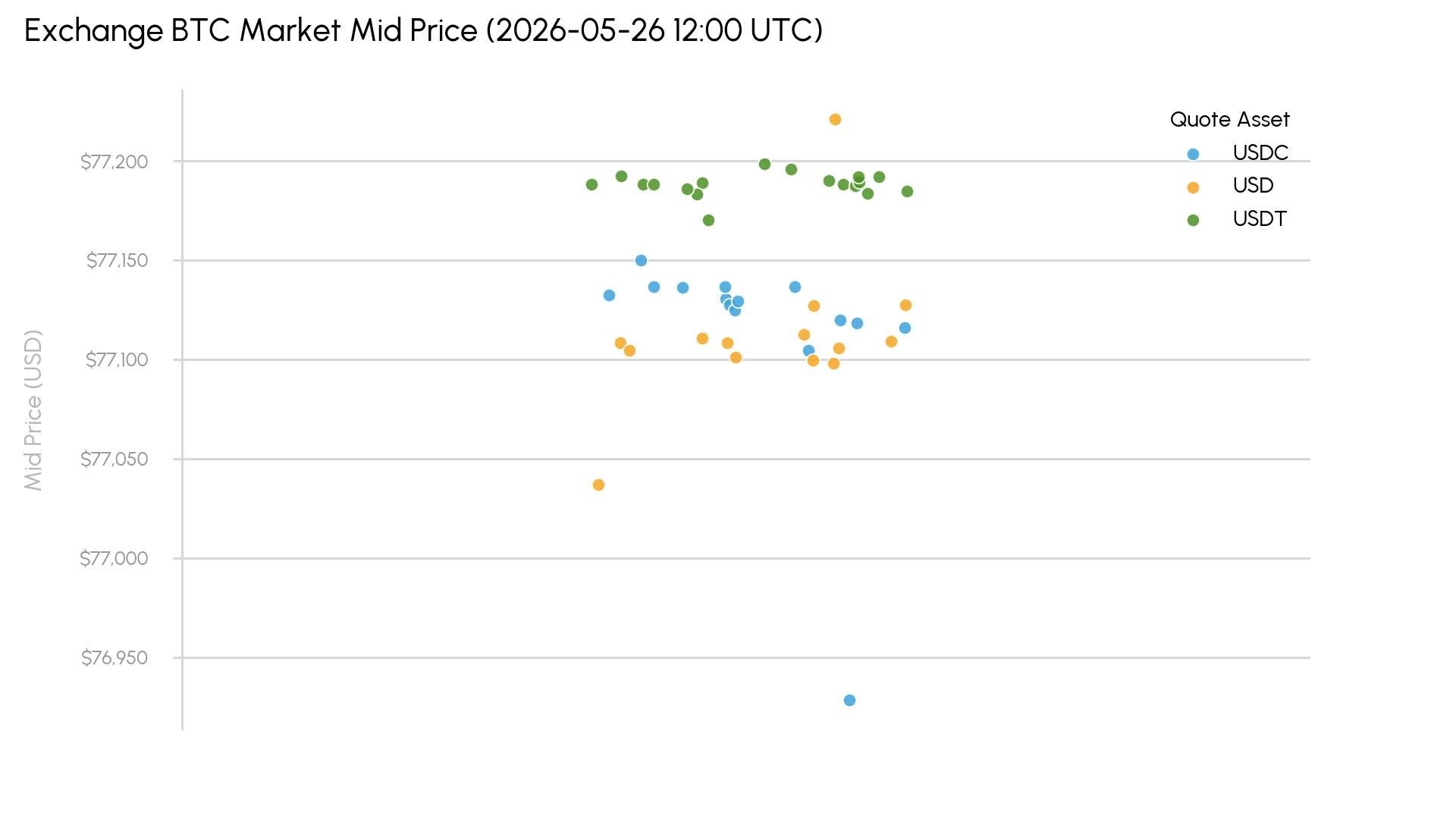

Source: Talos CM Market Data Pro

Examining the midprice across exchanges, USDT quote markets trade around $77,188 whereas USD and USDC quote markets trade around $77,112 and $77,115 respectively. Both BTC and quote asset price matter which can impact trade execution. Having unified liquidity across venues and identifying order books with minimal price change can improve selling large amounts of BTC like the 3,588 BTC sold in the most recent 8K filing.

Can Strategy Sustain its Payments?

Strategy’s creditor payments are growing, and BTC sales are becoming a part of how it meets them. STRC issuance and variable dividends can alone cost up to $3B annually, so maximizing the sale value helps limit how much BTC is sold to cover it. In the near term, the USD Reserve, Bitcoin Monetization Program and shift towards more active balance sheet management give Strategy the buffer to meet these obligations. Longer term, developing BTC as collateral and other financial products that integrate Strategy’s BTC holdings can reduce the need for large BTC sales or dilution of Strategy shareholders. Consequently, the economics of Strategy’s capital structure depend as much on the maturation of BTC-backed financial markets as on the appreciation of BTC itself.

Subscribe and Past Issues

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.