Q2 2026 Market Update: Reversals, Rotations & Rates

State of the Network #370

Q2 2026 Market Update: Reversals, Rotations & Rates

Introduction

State of the Network #370

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways:

- Bitcoin gave back its entire April rally, ending Q2 down roughly 11% against a backdrop of shifting rate expectations, ETF outflows and capital rotation into AI equities.

- The three major liquidity channels, ETFs, Strategy, and stablecoins weakened in Q2, with spot Bitcoin ETFs alone seeing -$4.08B in net outflows.

- $8.35B in BTC and ETH long liquidations resulting in a meaningful deleveraging in Q2, leaving the market thinner but more stable heading into Q3.

Re-(Introducing) State of the Market

Alongside our weekly State of the Network research deep diving into themes and market trends across the onchain ecosystem, we’re excited to be re-launching State of the Market: a dashboard and upcoming weekly newsletter built to track digital asset price action, flows, liquidity, and derivatives activity in one place.

In this issue, we use the dashboard to break down Q2 2026 across performance, flows, exchange activity, and the themes shaping the quarter.

Get State of the Market delivered to your inbox each week. Sign up here.

Market Overview & Performance

Digital assets entered Q2 2026 with momentum. Coming out of a difficult Q1, Bitcoin staged a broad based recovery through April, rallying to ~$82K alongside equities as geopolitical anxiety briefly eased and institutional demand improved. However, this recovery did not sustain.

The reversal was driven by three converging forces: higher oil prices as Brent crude hit a high of $126.41 on oscillating U.S.-Iran diplomatic talks, a hawkish shift in Fed rate outlook, and a rotation of capital into the AI trade where earnings momentum remained intact.

Source: Talos State of the Market Dashboard

Through mid-May, crypto and equities had moved broadly in tandem, with BTC and ETH both gaining ~20% from early April. The divergence came towards the end of May, when crypto pulled back while equities held their ground. The S&P 500 and Nasdaq 100 ended the quarter up ~16% and ~28% respectively, while BTC declined around 10%, ETH down ~20%, and SOL down ~13%.

Source: Talos State of the Market Dashboard

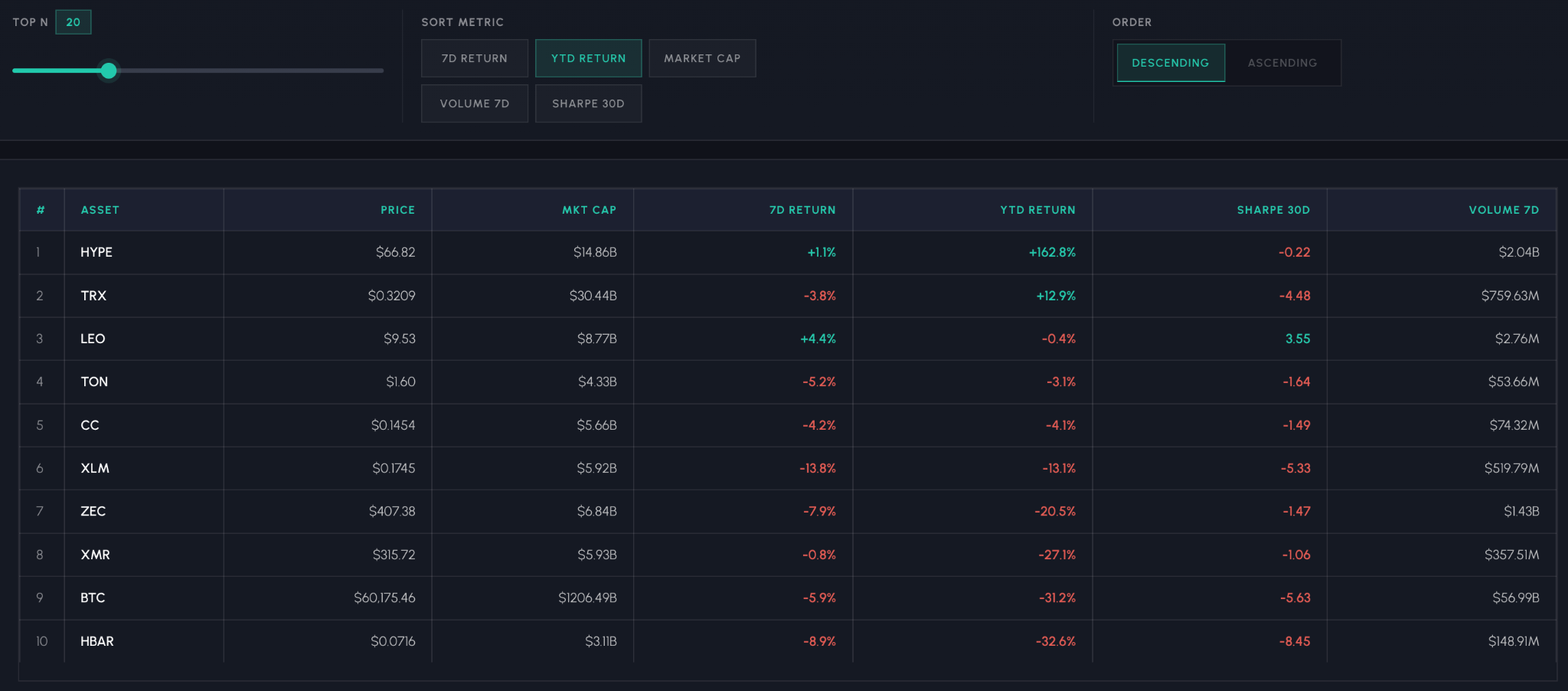

Bitcoin now sits near $60K, roughly 52% below its all time high of $126K set in late 2025. Altcoin performance tells a similar story with a narrow breadth of gainers. Year to date, Hyperliquid (HYPE) remains the lone standout among the top 20 crypto-assets by market cap (+142%), on the back of surging demand for onchain perpetuals trading in equities and commodities.

Flows

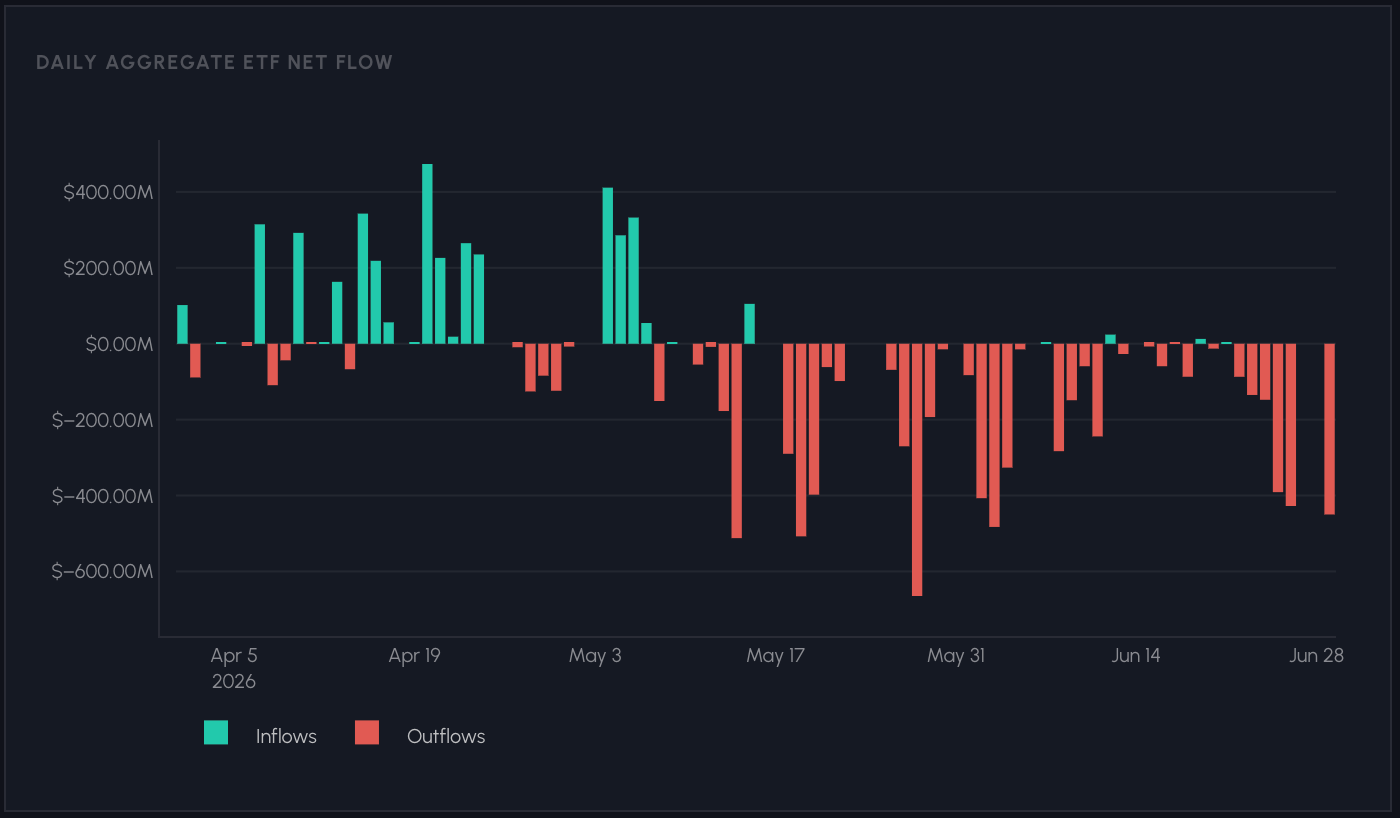

The quarters weakness was amplified by the deterioration of three major demand channels: spot ETFs, digital asset treasuries like Strategy, and stablecoin supply.

Spot Bitcoin ETFs: April was a strong start for spot Bitcoin ETFs with inflows dominating. The highest single day peak of $474M in inflows came on April 20th, after which flows flipped. Outflows dominated the remainder of the quarter, with 53 outflow days against just 30 inflow days across Q2. June drove the bulk of the damage, accounting for -$3.84B of the quarter’s -$4.08B total net outflow across tracked issuers.

Source: Talos State of the Market Dashboard

Digital Asset Treasuries (Strategy): Strategy’s Bitcoin acquisition pace slowed materially through the quarter. STRC, its preferred stock designed to trade near $100, fell to a record low near $74, while Strategy’s mNAV compressed towards 1.0, impacting the funding channel behind its accumulation. The 32 BTC sale in early June caught markets off guard and put a dent in the “never sell” sentiment. As a response, Strategy has established a new Digital Credit Capital Framework, raising the STRC dividend to 12%, authorizing up to $1.25B in BTC sales, and setting a $2.55B USD reserve covering roughly 17 months of obligations.

Stablecoins: The total stablecoin market cap contracted by ~$4.2B across Q2, removing a layer of dry powder that supports onchain activity and liquidity. USDT grew modestly by $1.8B while USDC shed $3.4B. Ethena’s USDe fell $1.4B as the risk-off environment reduced appetite for yield bearing stablecoin strategies.

With all three major demand channels weakening simultaneously, the liquidity backdrop heading into Q3 is materially thinner than where Q2 began. Whether that demand returns to crypto-assets or continues flowing into AI equities remains a dynamic to watch.

Exchange Activity & Derivatives

Total spot volume across exchanges fell 28% QoQ to $2.32T, continuing a decline that began in January. Futures volume held up better at $12.32T, down 11.6% QoQ, but the spot/futures ratio compressed from 0.23x to 0.19x, pointing to increased derivatives positioning rather than spot demand.

Hyperliquid was a notable standout, growing its futures volume market share to ~4.5% as onchain perpetuals continued to gain ground against centralized venues.

Source: Talos State of the Market Dashboard

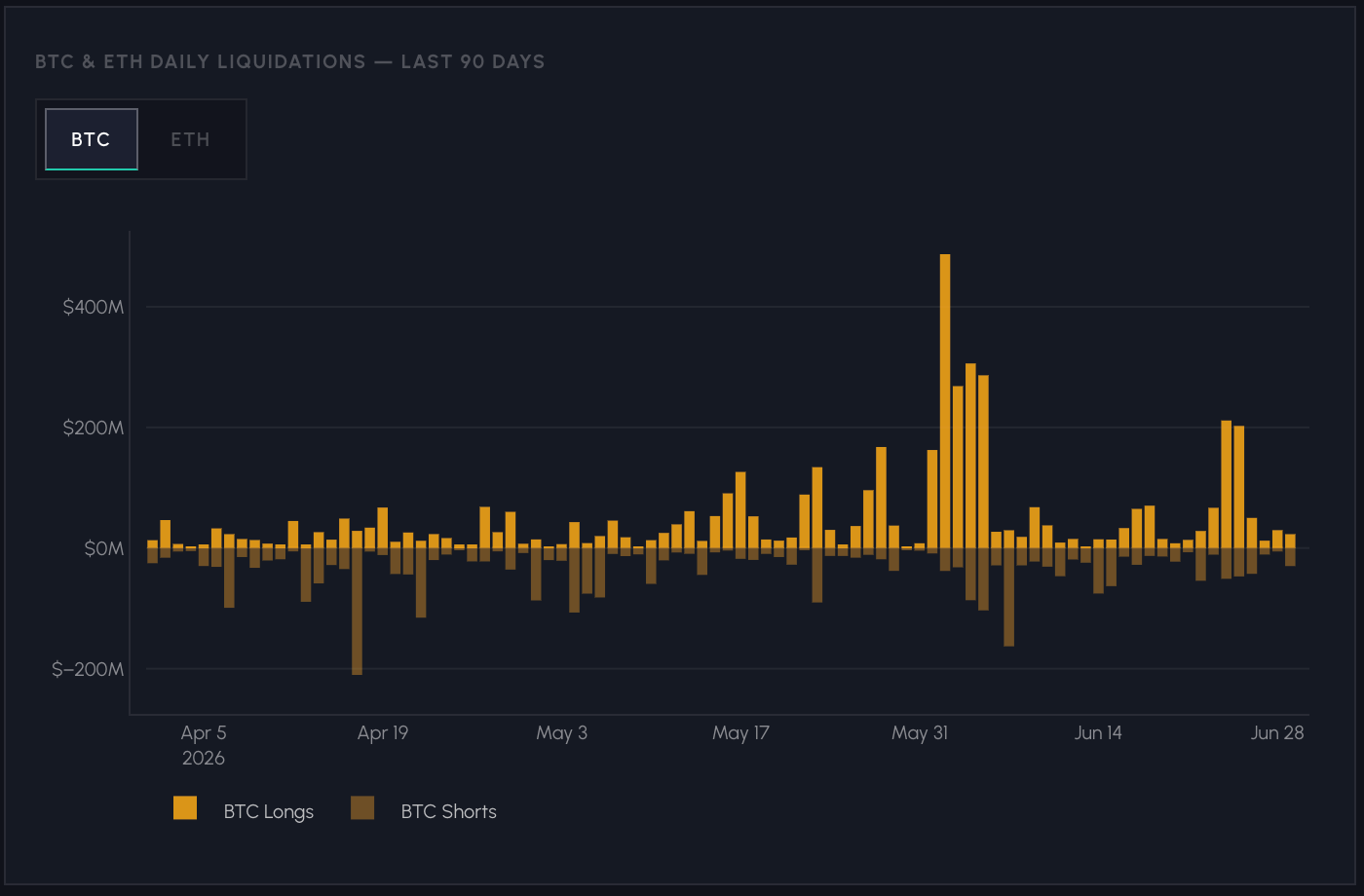

Open interest peaked ahead of the May selloff with BTC hitting $49.2B and ETH reaching $27.2B. These figures have now fallen to $33.5B for BTC and $16.2B for ETH respectively, down 32% and 40% from their peak. Combined BTC and ETH long liquidations totaled $8.35B across Q2. More than half of these liquidations occurred between May 25 and June 7, as overleveraged longs were flushed out in a self-reinforcing loop. The market enters Q3 in a more deleveraged state.

Funding rates were volatile across Q2, swinging from deeply negative (-16% annualized) in mid-April, to strongly positive into May (+10% annualized) as long positioning built up. The following selloff brought rates back to neutral, ending the quarter oscillating around zero with cautious sentiment.

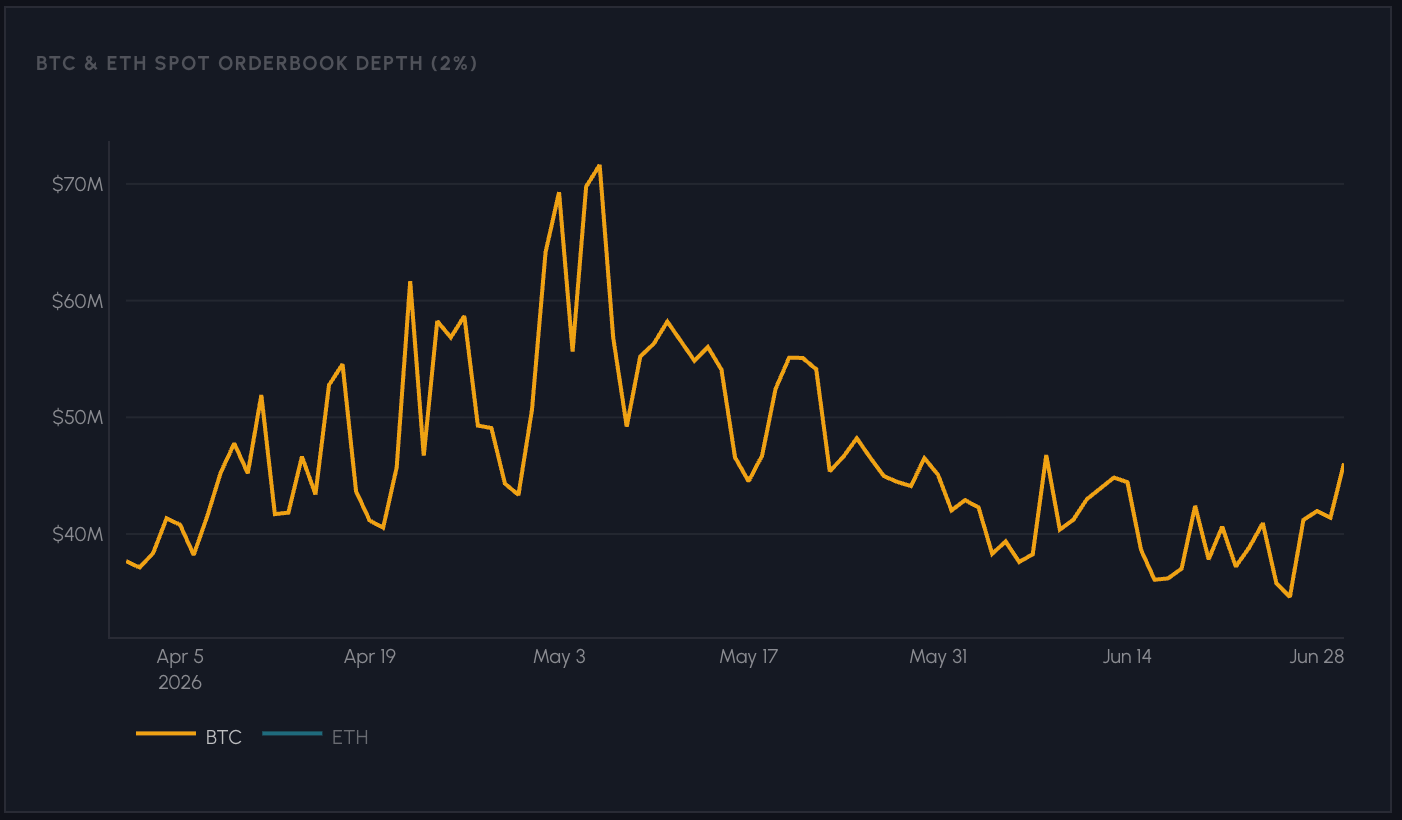

Liquidity deteriorated in parallel. Bitcoin’s 2% orderbook depth declined from a peak near $70M in early May to roughly $35-40M by late June, indicating thinner markets and reduced capacity to absorb selling pressure.

Source: Talos State of the Market Dashboard

Themes Shaping the Quarter & Ahead

Beyond the quarter’s price action, several structural developments point to where markets are headed, from new asset classes coming onchain to the infrastructure underpinning them.

- Tokenized Equities: Coinbase announced 1:1 backed tokenized stocks with full legal rights. As new models for tokenizing securities like stocks emerge, we mapped out the different forms of equities exposure onchain. [The Spectrum of Tokenized Stock Exposure].

- RWA Perpetuals Take Off: Onchain trading and price discovery expanded beyond crypto into stocks, indices and commodities through Hyperliquid HIP-3 perpetuals and centralized exchanges offering 24/7 RWA perps. [Perps, Outcome Markets & USDC Yield, Perpetually Open: The Rise of 24/7 Onchain Markets].

- SpaceX IPO Gets Priced Onchain: The $1.7T SpaceX IPO was priced on crypto rails ahead of its public listing, providing an early signal of price discovery for private companies. [Pre-IPO Price Discovery on Crypto Rails]

- Vaults & Lending Markets: Onchain vaults are becoming a core allocation layer for institutional capital, pooling deposits into curated lending strategies across protocols like Morpho and Aave. With traditional asset managers like Bitwise entering vault curation, the infrastructure is maturing rapidly. [Vaults: Mechanics, Landscape & Risk]

Subscribe and Past Issues

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.