Q1 2026 Review: Crypto Markets Reset as Traditional Assets Go 24/7

State of the Network #357

Q1 2026 Review: Crypto Markets Reset as Traditional Assets Go 24/7

Introduction

State of the Network #357

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways

- Crypto markets stayed under pressure in a volatile macro and geopolitical backdrop, but improving ETF demand over the quarter helped BTC find support at current levels.

- Onchain venues and tokenization pushed further into 24/7 markets for traditional assets, with equity and index perpetuals on platforms like Hyperliquid and new stock perps from major exchanges driving steady growth in open interest.

- Stablecoin supply stayed steady near ~$300B while adjusted transfer volumes grew to around $21.5T in Q1, as emerging regulatory clarity around stablecoin yield and distribution continues to shape the sector.

Introduction

With the first quarter of 2026 coming to a close, it’s a good moment to take stock of the developments and themes that shaped crypto markets. Q1 2026 was driven by a combination of geopolitical and macroeconomic uncertainty, creating a volatile, risk-off backdrop. While it was a challenging quarter for crypto markets with the total market cap sliding ~22%, themes like tokenized equities and 24/7 onchain trading of traditional asset classes stood out as bright spots, building on fundamental progress in the industry.

In this issue of State of the Network, we look back at Q1 2026 to understand the market trends and themes that shaped the quarter.

Market Performance

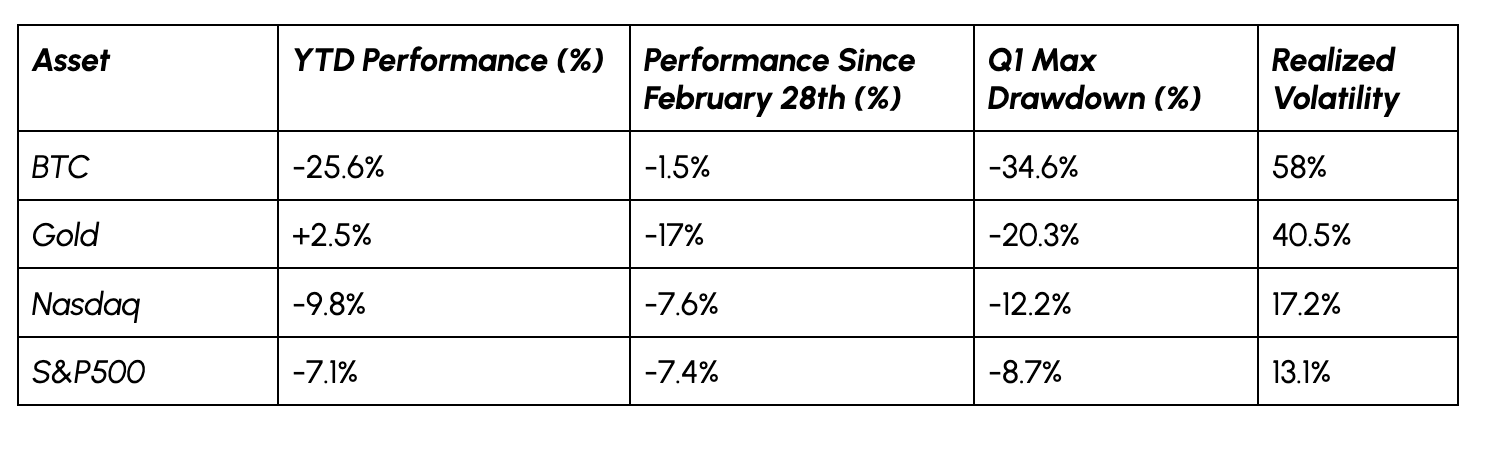

Bitcoin (BTC) experienced over a 30% drawdown from ~$95K in February, ending the quarter down 22% year to date. In addition to macroeconomic pressure, the move was exacerbated by a broader selloff in risk-assets and liquidations in derivatives markets, reigniting questions around Bitcoin’s role as a safe haven and store of value. However, since the outbreak of the Iran war on February 28th, Bitcoin has demonstrated notable relative strength compared to both equities and gold, suggesting some degree of resilience and return in demand.

Source: Coin Metrics Prices & Google Finance

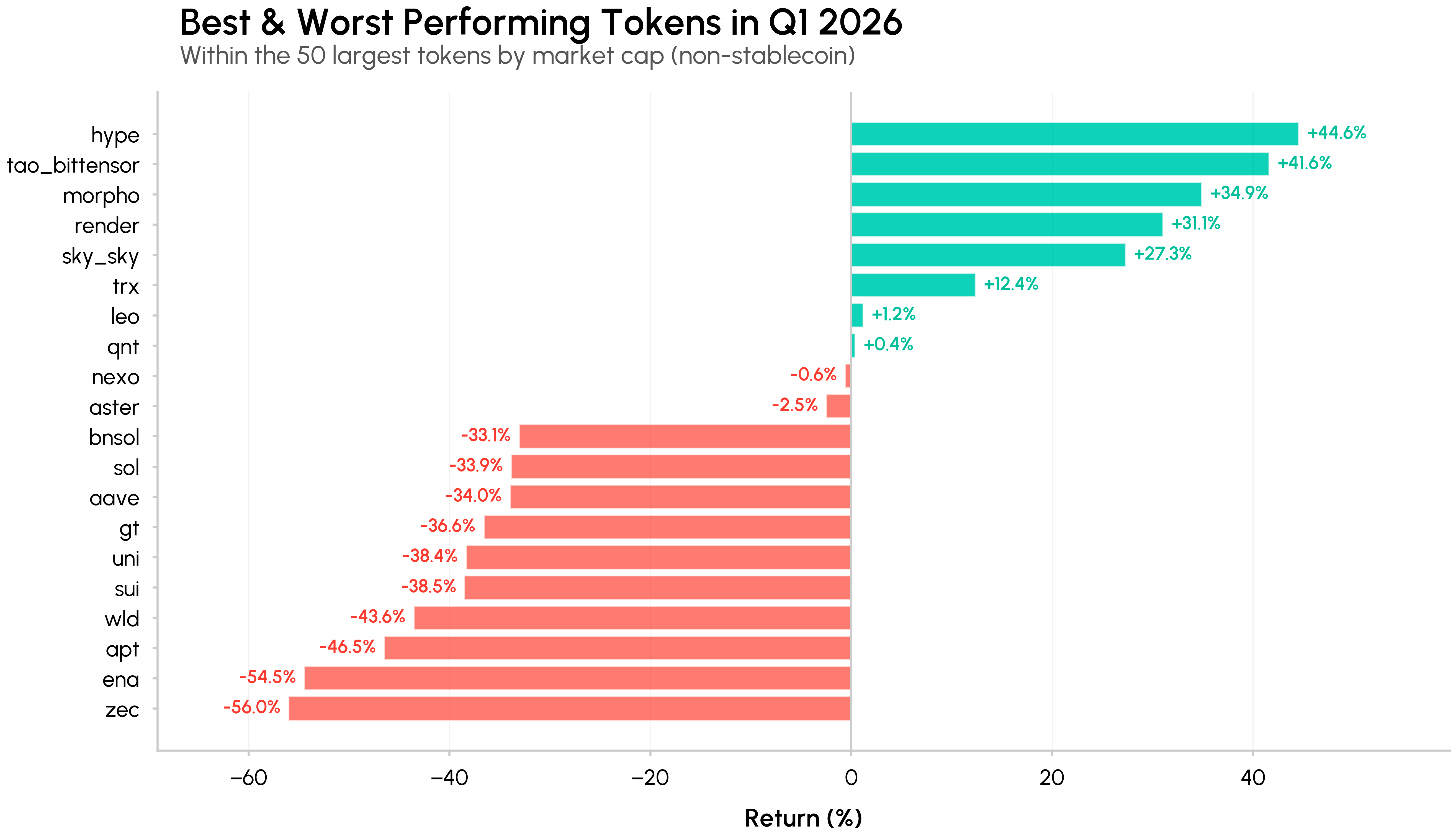

Among cryptoassets, performance was concentrated in a handful of altcoins with strong narrative momentum and real usage growth, pointing to a market of narrowing breadth.

Notable outperformers included Hyperliquid (HYPE), Bittensor (TAO) and Morpho (MORPHO), each returning over 30% over the quarter. Hyperliquid benefitted from growth in its HIP-3 markets (particularly commodities and equity indices), extending its footprint across asset classes beyond crypto. Bittensor and Morpho were also supported by growth in the AI infrastructure and DeFi credit verticals, with growing institutional interest in decentralized AI and vault curation.

Source: Coin Metrics Prices & Network Data Pro

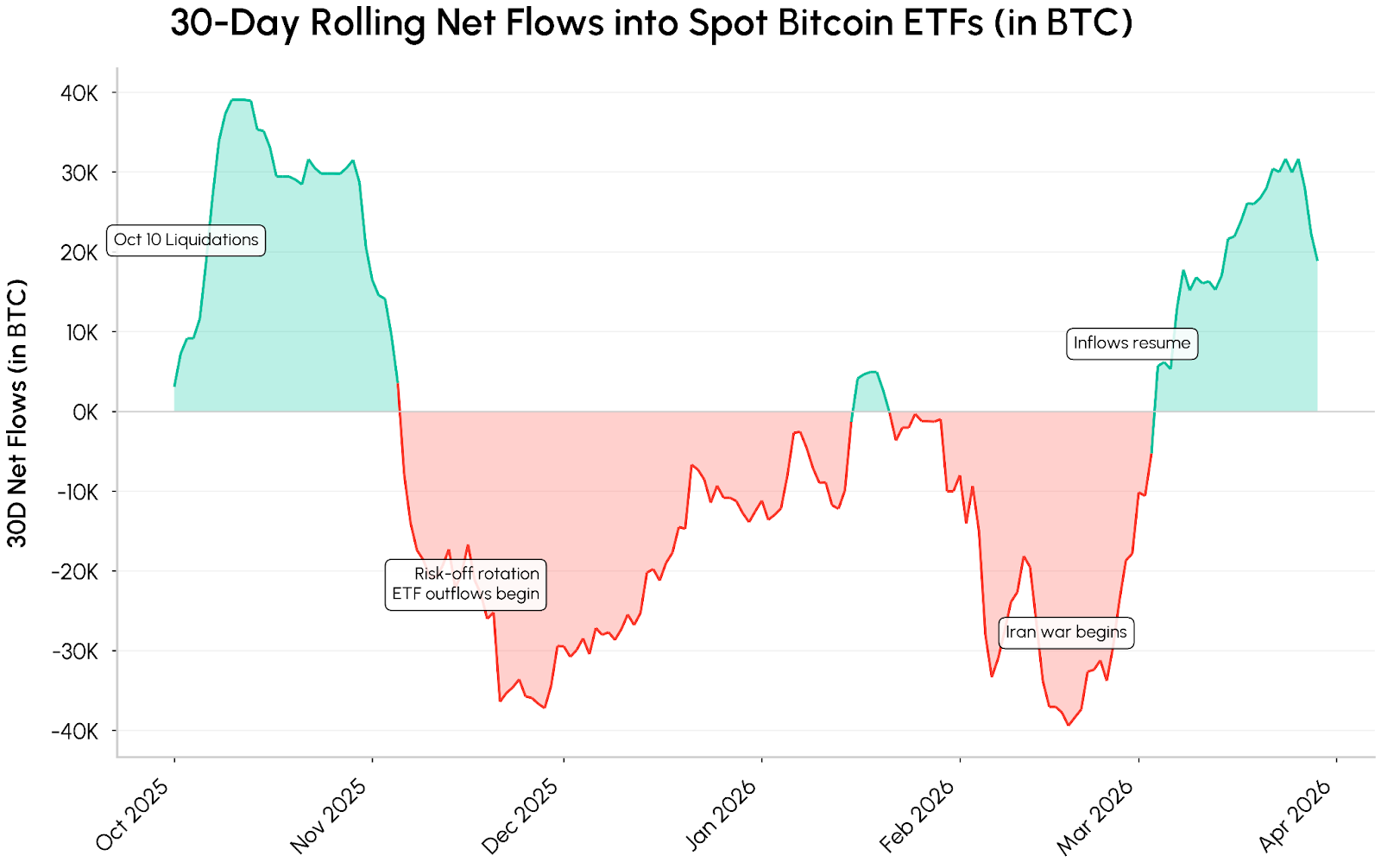

Bitcoin Demand Finds its Footing

The risk-off environment prevalent through early parts of the quarter reversed in March. Despite some weakness, demand from spot Bitcoin ETFs has improved in a meaningful way, shifting from the sustained outflows seen since November 2025. On a 30-day rolling basis, net ETF flows have turned positive by over 30K BTC, supporting its consolidation near the $70K level.

Source: Coin Metrics Network Data Pro

Whether this demand sustains and accelerates will largely depend on how the macro and policy backdrop evolves. A de‑escalation in geopolitical risk, clearer signs that inflation is easing and rate‑cut expectations are back on track, and continued growth in ETF and digital asset treasury (DAT) balance‑sheet demand, including programs like Strategy’s $42B Bitcoin raise, would all help reinforce flows.

24/7 Onchain Markets & Tokenized Equities

Hyperliquid & Traditional Asset Classes

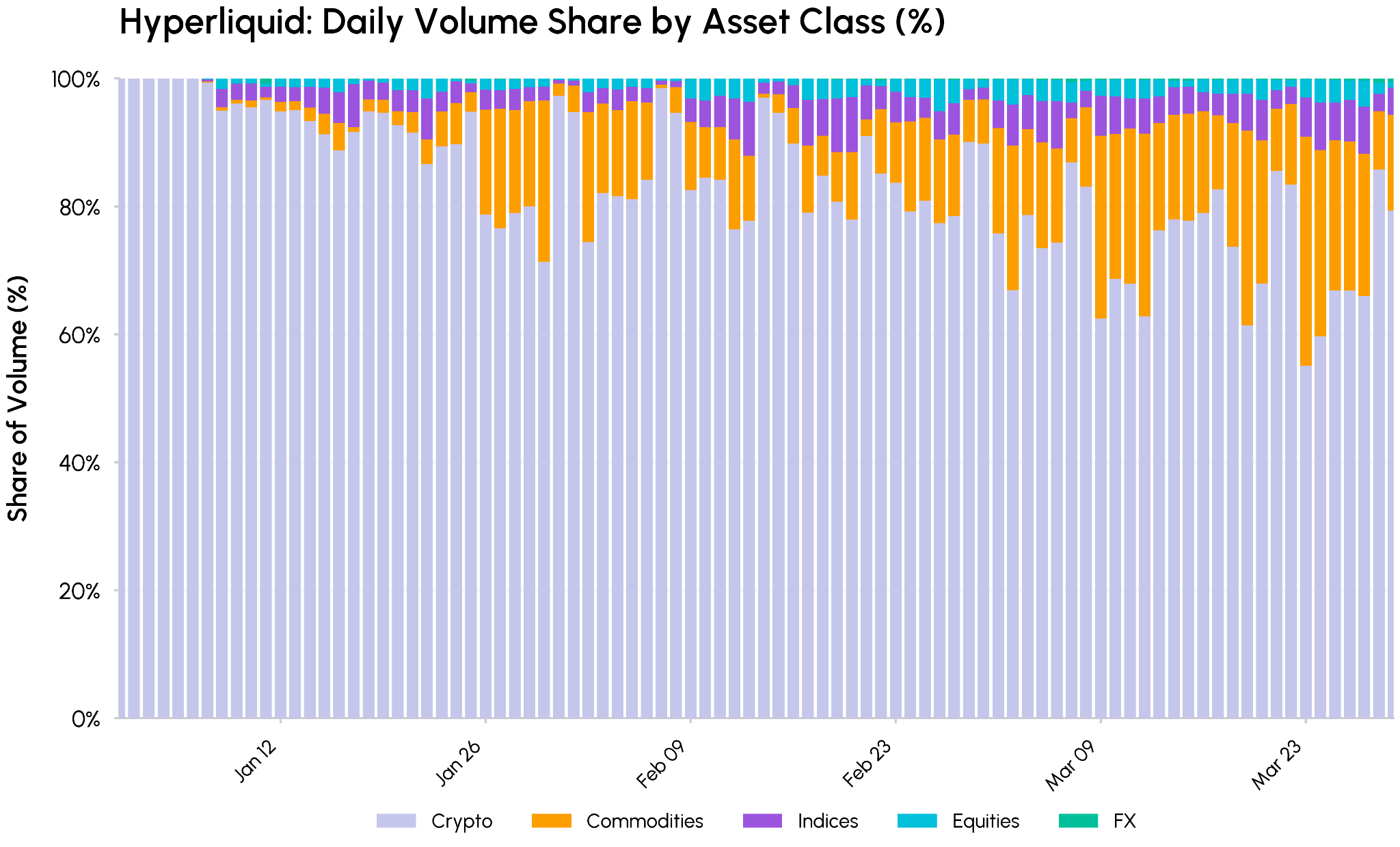

A defining theme this year has been the accelerating convergence of traditional financial markets and onchain infrastructure through both tokenized issuance and 24/7 trading. The growth in perpetual futures on traditional asset classes was one of the clearest examples of this momentum.

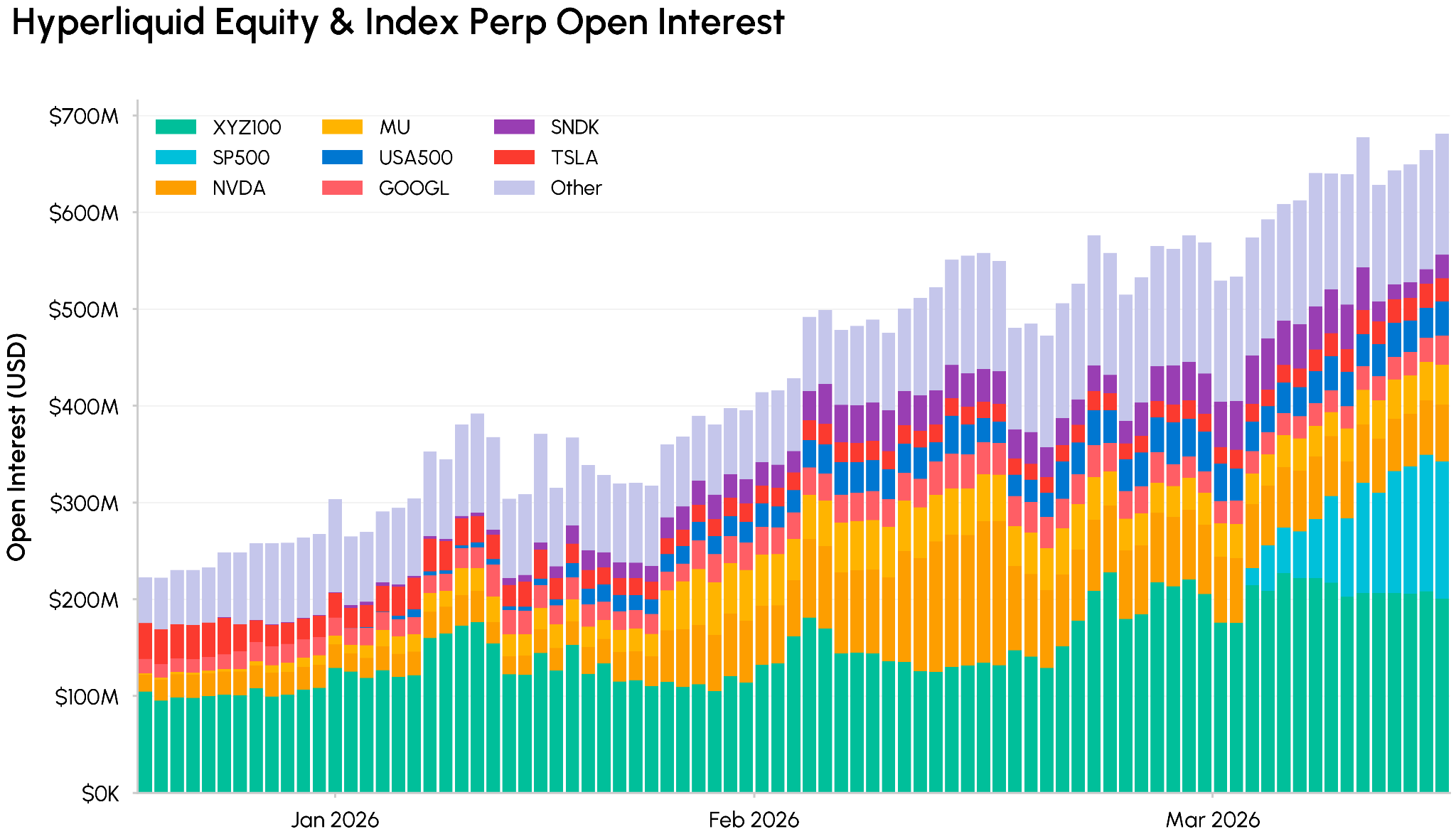

Hyperliquid, which launched HIP-3 markets on asset classes like equities, indices and commodities, saw its share of non-crypto volume grow significantly over the quarter to ~45%. Overall volume and open interest (OI) rose meaningfully as traders sought round the clock exposure to metals and oil amid geopolitical shocks, with OI in (HIP-3) traditional asset classes making up ~28% ($1.9B) of overall open interest on the platform.

Source: Coin Metrics Market Data Feed

The Rise of Equity Perps

Within this segment, benchmarks on major stocks and indices have been the fastest growing as venues expand access. Kraken introduced perpetual futures contracts (perps) on xStocks in February, while Coinbase International rolled out stock perps, providing leveraged exposure to US stocks. Meanwhile, Hyperliquid’s largest HIP-3 deployer trade[XYZ] launched the first official S&P 500 perpetual contract in partnership with S&P Dow Jones Indices, adding to an array of markets providing exposure to global equities.

Source: Coin Metrics Market Data Feed

Open interest in Hyperliquid’s equity and index perps has climbed steadily. Flagship benchmarks such as XYZ100 (Nasdaq 100) and SP500 now sit among the largest markets on the venue by OI, with single‑name stocks like Nividia (NVDA), Micron Technology Inc (MU) and others also building meaningful depth. Tokenized equity and fund issuance is also growing in tandem, from frameworks like xStocks to tokenized money‑market and equity funds issued by players such as Ondo on Ethereum and Solana.

Together, this growth in tokenized equity and RWA perps reinforces the idea that onchain venues are starting to function as 24/7 extensions of traditional markets rather than purely crypto‑native trading environments.

Stablecoins: Steady Supply, Growing Utility

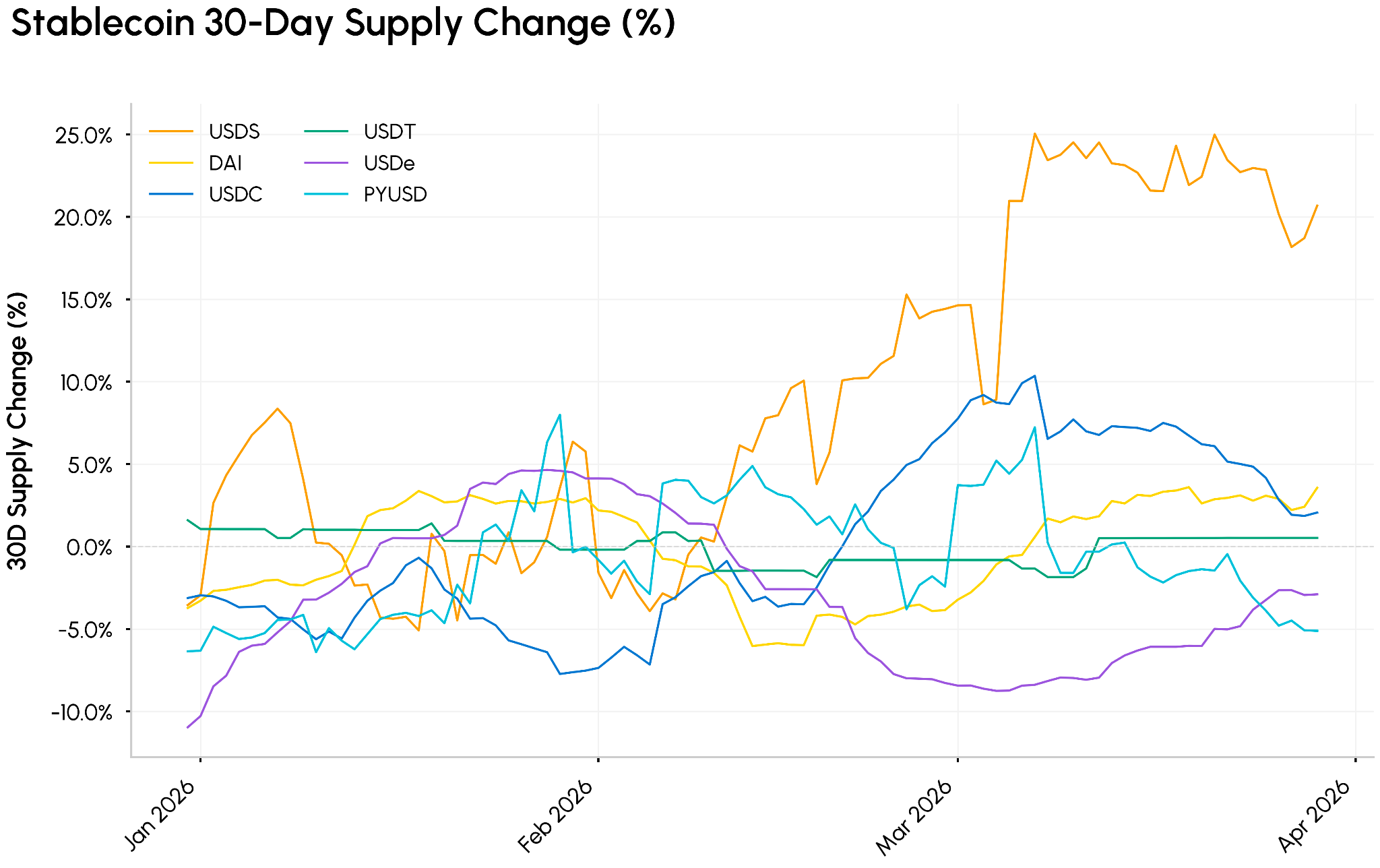

Stablecoins continued to demonstrate their role as the bedrock of onchain liquidity. Despite a broader market selloff, total stablecoin supply held steady near $300B through Q1, with 30-day supply growth ticking higher in February. Among stablecoins, growth was led by USDS, a USD pegged stablecoin backed by crypto & real-world asset (RWAs) collateral and issued by Sky Protocol (formerly MakerDAO). USDS supply grew by 43% to ~$8B, while Circle’s USDC supply reached $77B while USDT remained steady ~$184B.

Source: Coin Metrics Network Data Pro

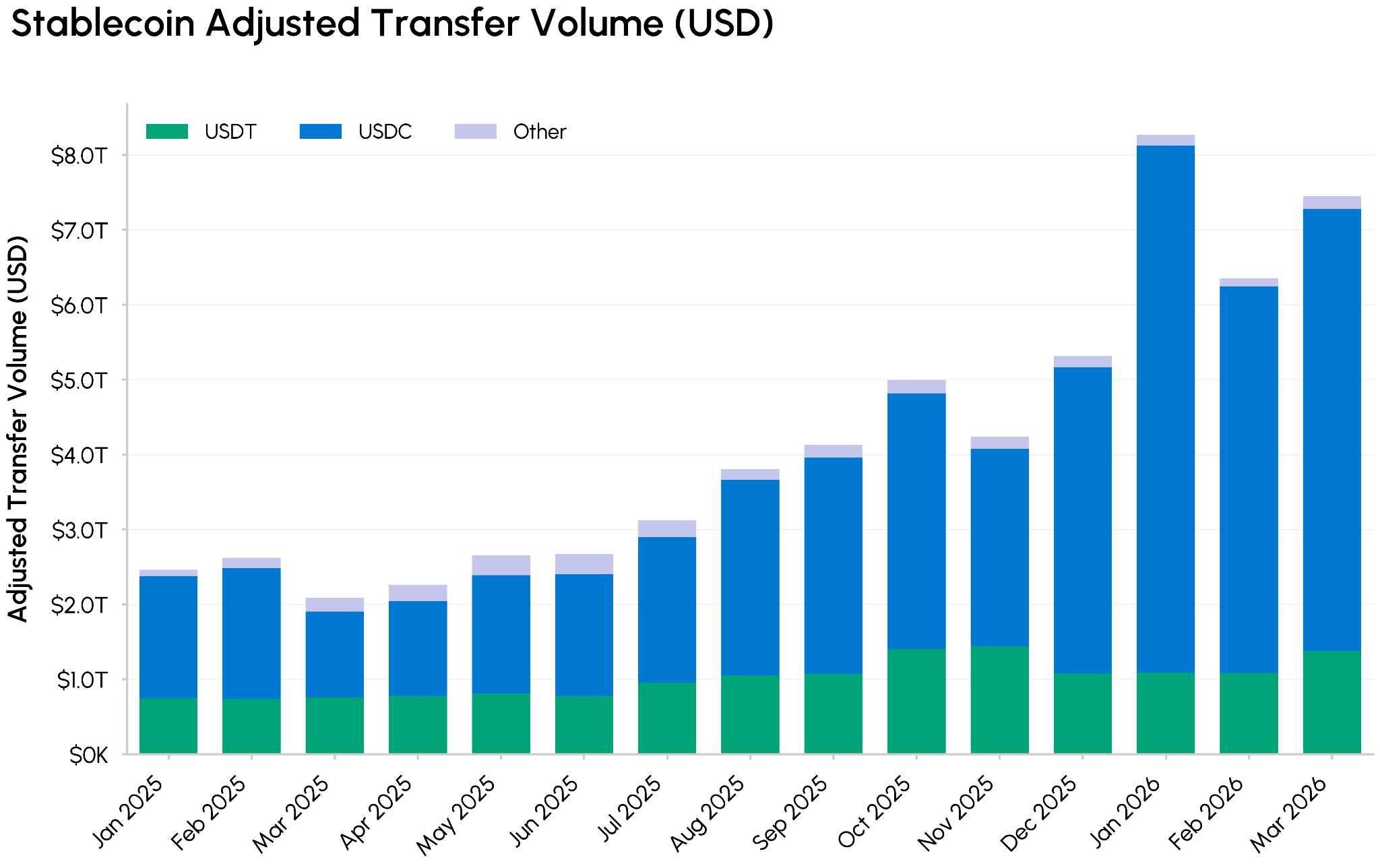

While supply held steady, stablecoin turnover and usage increased meaningfully. Adjusted stablecoin transfer volumes reached a total of $21.5T in the quarter, roughly 3x levels seen in Q1 2025. Over 80% of this volume came from USDC, gradually gaining a larger share of transactional usage relative to USDT. This activity was largely driven by USDC on Base, which alone saw $13T in transfer volume in Q1. As we explored in a recent issue, a significant portion of this flow reflects DeFi infrastructure activity such as LP rebalancing and flash loans rather than end‑user payments or settlement, even as those use cases grow.

Source: Coin Metrics Network Data Pro

Going forward, the sector’s trajectory may hinge around yield and distribution dynamics. A recent draft of the CLARITY Act bill proposed banning yield on passive stablecoin balances, while permitting activity-based rewards tied to payments or platform usage. Such a provision could alter the economics for key participants.

For Coinbase, where stablecoin revenue now represents over 25% of total revenues, constraints on offering USDC yield could weaken its ability to attract and retain balances, while Circle appears somewhat more insulated and could benefit if elevated rates and clearer rules push usage toward payments and transaction‑driven revenue. The knock‑on effects for DeFi lending, yield‑bearing stablecoins, and tokenized treasuries also bear watching as the bill advances.

SEC Reveals Digital Asset Taxonomy

The quarter also brought important regulatory clarity. The SEC and CFTC released joint interpretation that introduces a five‑category taxonomy for crypto assets and explains how each fits within existing securities and commodities law.

- Digital commodities: Core network tokens whose value is tied mainly to a functional crypto system and market supply–demand (e.g., major L1s) are treated as commodities rather than securities.

- Digital collectibles and tools: NFTs, in‑game items, gas and access tokens are generally outside securities rules unless they’re fractionalized or marketed primarily as investments.

- Payment stablecoins: Fiat and RWA‑backed payment stablecoins are viewed as money‑like instruments, though yield‑bearing or non‑qualifying designs can still trigger securities analysis.

- Digital securities. Tokenized stocks, bonds, credit RWAs and similar instruments remain full securities regardless of on‑chain format.

- Staking, mining, wrapping. Native staking, mining, airdrops and basic wrapping are not securities transactions, but pooled staking and yield‑wrapped/structured tokens can be investment contracts depending on the promises made to buyers.

For a deeper dive deeper dive into the new token taxonomy, CLARITY Act negotiations, and global policy moves, see Talos’s latest Regulatory Roundup

Conclusion

While prices remained sensitive to macro and geopolitical forces, the underlying rails kept advancing. Bitcoin has started to find support at current levels, and onchain venues pushed further into 24/7 markets for equities, commodities, and RWAs. At the same time, major traditional players like NYSE and Nasdaq actively moved into tokenization to modernize equity trading. Regulatory developments around the CLARITY Act and stablecoin yield will be central for the sector, and a better macro backdrop would give risk appetite more room to return to crypto assets.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.