Layer-1 Landscape: The Specialization of Blockspace

State of the Network #358

Layer-1 Landscape: The Specialization of Blockspace

Introduction

State of the Network #358

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways

- As blockspace scales and transaction costs fall, differentiation between chains is shifting from cost to use-case specialization.

- Bitcoin’s 20 millionth coin was mined in March, while a growing ecosystem of wrapped tokens and ZK rollups are beginning to unlock Bitcoin’s programmability and productive utility.

- Ethereum is reinforcing its role as the on-chain liquidity and settlement hub, with L1 fees at record lows as L2s evolve from scaling solutions to specialized execution environments.

- Solana is advancing its Internet Capital Markets vision through growing payments adoption and sophisticated onchain trading infrastructure, with Alpenglow targeting sub-second finality.

Introduction

The cost of transacting onchain has fallen materially as blockspace scales across networks. Ethereum mainnet fees have declined substantially following recent upgrades, Solana transactions remain at fractions of a cent, and L2s offer similarly low-cost execution environments. As costs compress, blockspace differentiation is increasingly defined by ecosystem liquidity, throughput, and use-case specialization rather than marginal cost advantages.

In this issue of State of the Network, we explore how major L1s are evolving around distinct roles: Bitcoin expanding its programmability and productive utility, Ethereum consolidating as the settlement and liquidity hub for stablecoins, RWAs, and DeFi, and Solana positioning for high-frequency payments and trading.

Bitcoin

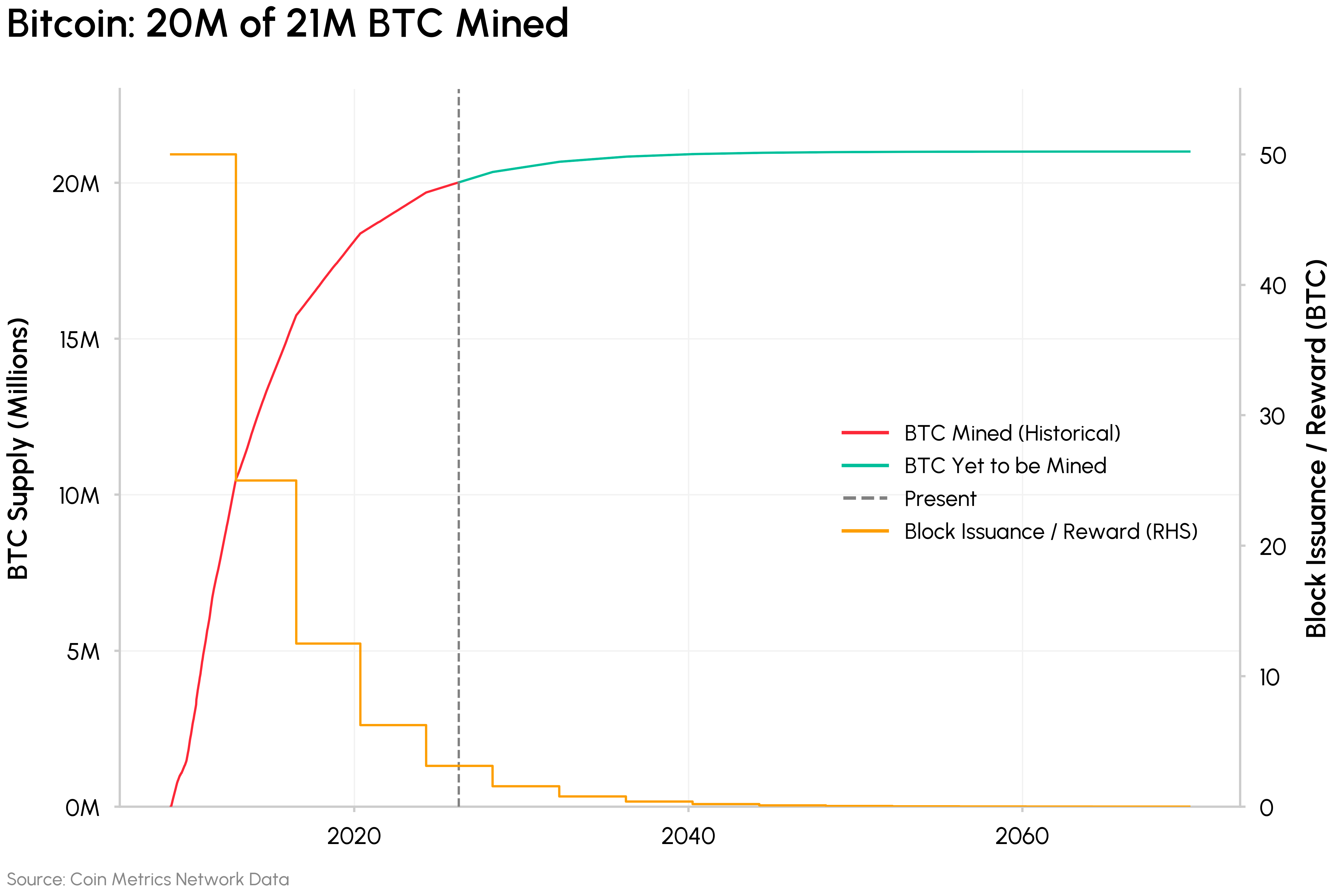

In March 2026, the 20 millionth Bitcoin was mined, leaving only 1 million BTC left to be issued going ahead. Over 95% of Bitcoin’s total supply is already in circulation, and with the block subsidy now at 3.125 BTC following the April 2024 halving, issuance continues its programmatic decline.

Source: Coin Metrics Network Data Pro

As block rewards diminish, transaction fees become an increasingly critical component of miner revenue. Outside of episodic spikes, transaction fees make up less than 1% of total miner revenue. Since fees on Bitcoin flow entirely to miners, the long-term question for Bitcoin’s security model is whether organic fee demand can sustainably fill the gap left by declining issuance.

Making Bitcoin Programmable and Productive

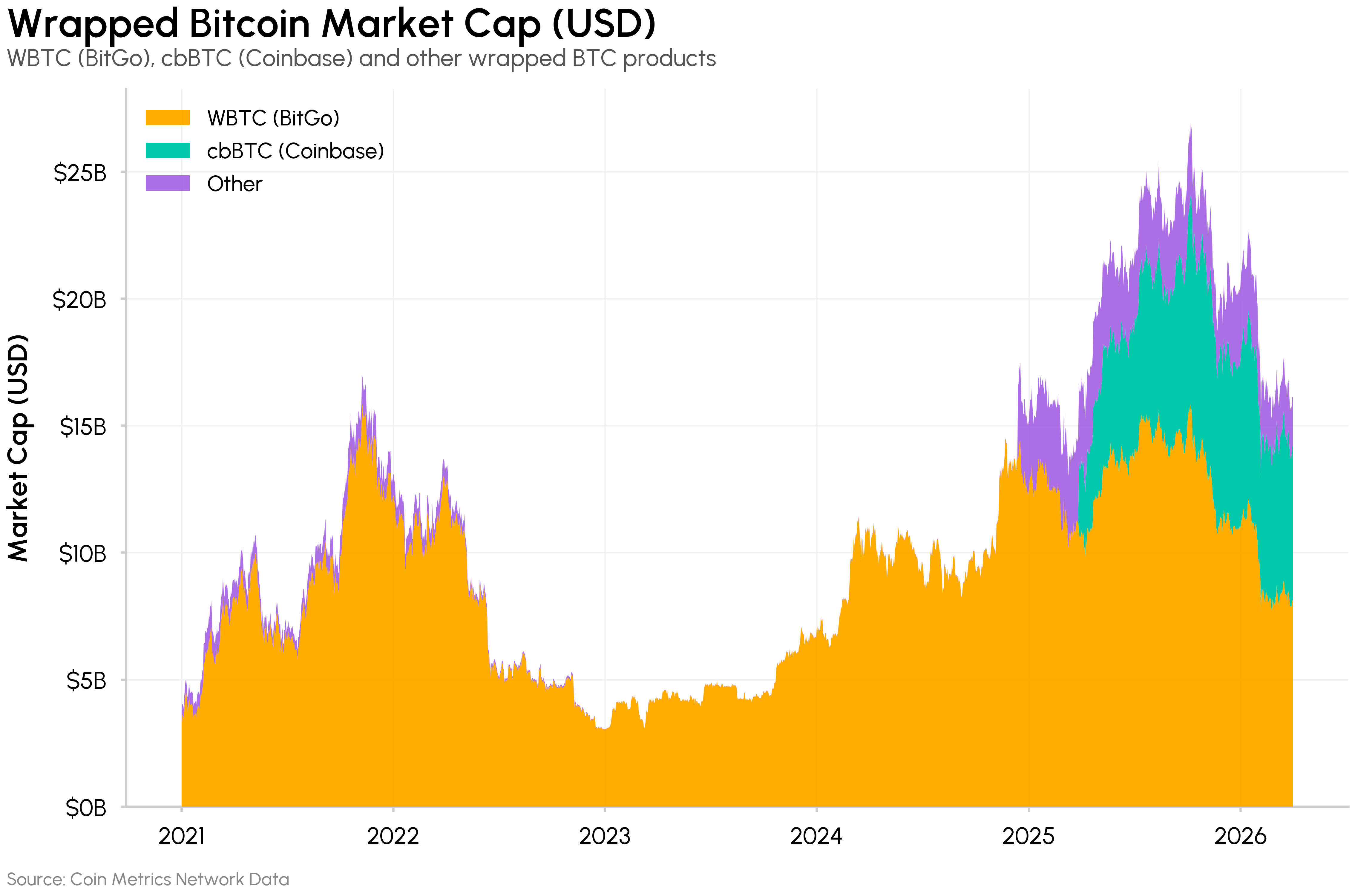

Despite Bitcoin’s ~$1.3T market capitalization, around 60% of BTC has not moved in over a year, and approximately 2.4 million BTC (around 11% of supply) sits on centralized exchanges while an additional ~243,000 BTC circulates as wrapped tokens on other chains. The majority of Bitcoin’s capital base remains economically passive, and most of the activity and fee generation around it happens off the base layer.

Bitcoin’s functional role is evolving along two fronts: expanding base‑layer programmability and increasing BTC’s productive utility. A growing ecosystem of sidechains, L2s like the Lightning Network, wrapped Bitcoin tokens and liquid staking protocols have enhanced Bitcoin utility, but carry varying degrees of trust assumptions, from fully custodial to smart contract-based models.

Source: Coin Metrics Network Data Pro

At the more trust-minimized end is Citrea, a ZK rollup that settles directly on Bitcoin L1. Using BitVM, a framework that allows programs to be verified within Bitcoin’s existing scripting system, Citrea enables EVM-compatible applications secured by Bitcoin’s proof-of-work (PoW). Unlike sidechains, it uses zero-knowledge proofs to settle on Bitcoin directly, while relying on a non-custodial bridge for withdrawals.

In parallel, the productive use of BTC as collateral is growing. Wrapped Bitcoin tokens collectively represent over $15B in value across chains like Ethereum, with Coinbase’s cbBTC-backed lending markets on Morpho also crossing $1B. Liquid staking protocols like Babylon extend this further, allowing BTC to serve as economic security for external proof-of-stake networks. These developments are beginning to unlock the productive capacity of capital that has historically sat idle.

Ethereum

Ethereum continues to serve as the liquidity and settlement hub. It holds ~62% of total stablecoin market cap, hosts the deepest DeFi liquidity of any chain, and is a growing destination for tokenized real-world assets (RWAs), from money market funds to tokenized treasuries and equities.

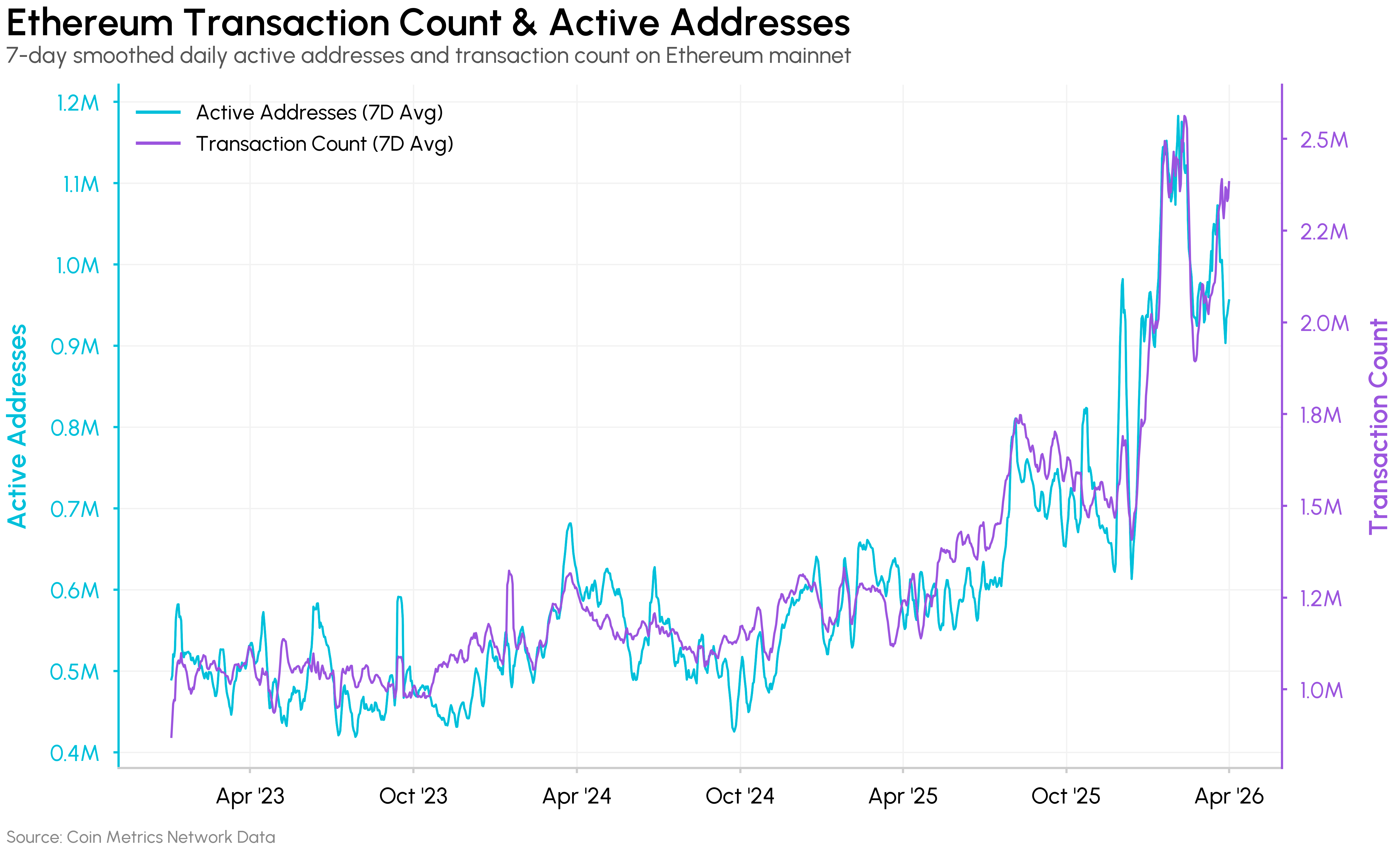

Recent upgrades are reinforcing Ethereum’s base layer as the core of economic activity. PeerDAS, larger blob space, and higher gas limits through the Pectra and Fusaka have driven L1 fees to multi‑year lows, expanding the range of activity that can settle directly on mainnet.

Source: Coin Metrics Network Data Pro

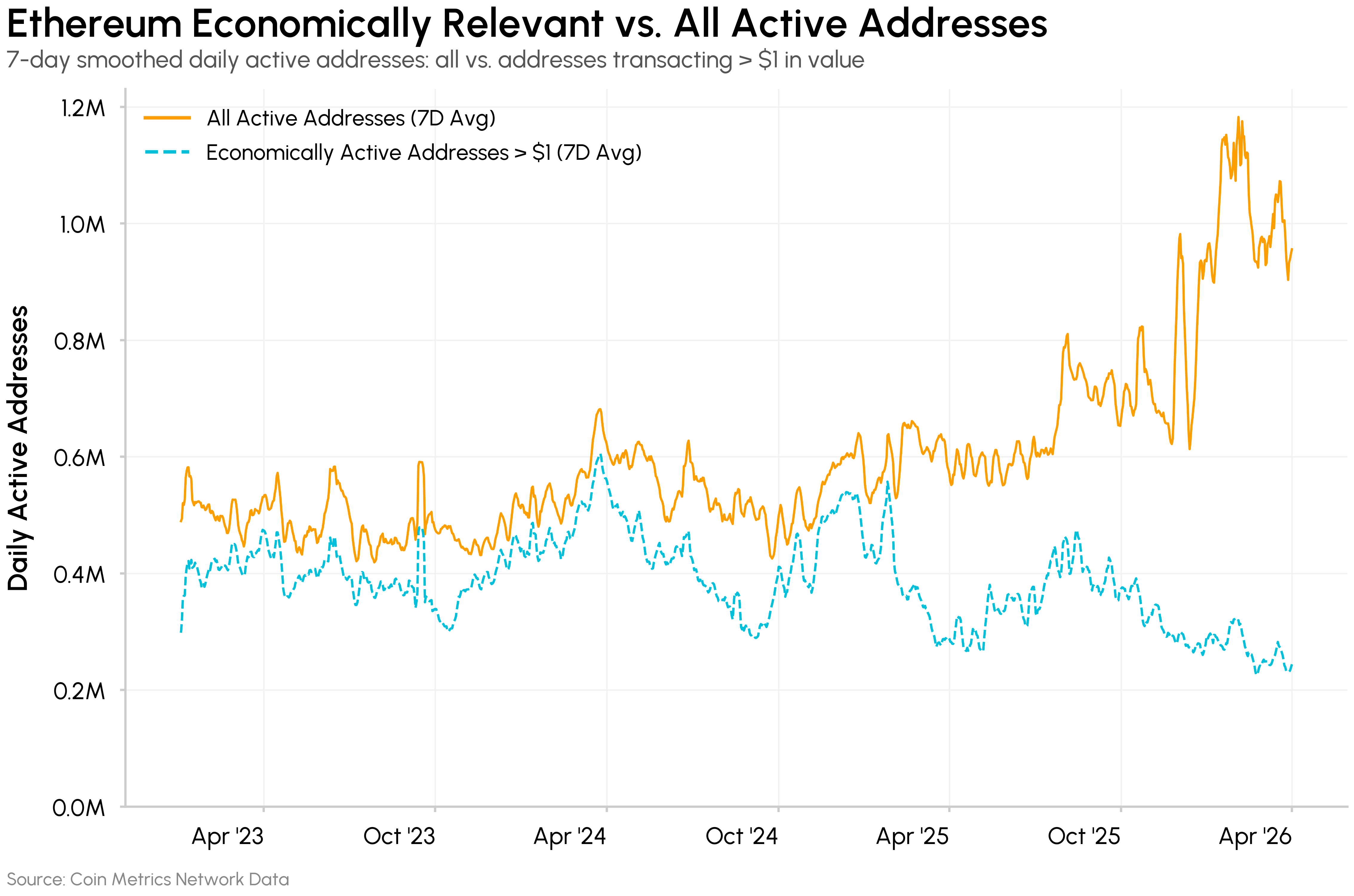

Daily active addresses and transactions on Ethereum mainnet have roughly doubled year over year, crossing 1M and 2.4M respectively. However, as we previously found, a portion of this increase reflects address poisoning attacks and a rise in dust addresses (wallets holding under $1), which at times have made up a significant share of daily active addresses.

Source: Coin Metrics Network Data Pro

The Shifting L1 <> L2 Relationship

As transacting on L1 becomes materially cheaper, the role of Ethereum’s Layer‑2s is being re‑examined. L2s were conceived as Ethereum’s primary scaling mechanism, offloading execution to bring costs down. That objective is now shifting. As outlined in a recent blog post from the Ethereum Foundation, the primary purpose of L2s is now to provide differentiated features, customizations, and specialized execution environments, with additional scale as a secondary benefit.

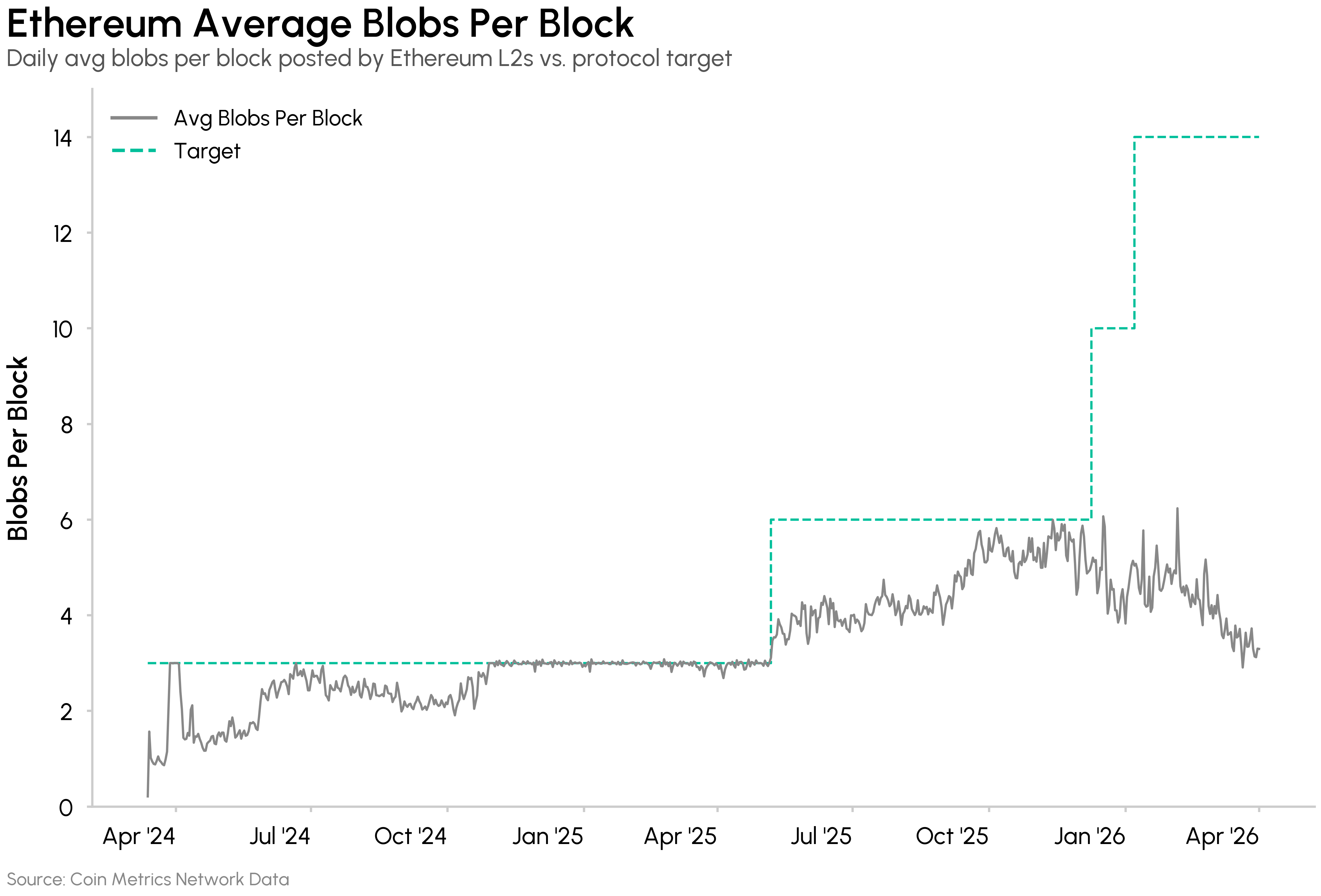

Blob space (the dedicated data availability layer L2s use to post transaction data to Ethereum) is <30% full, with ~3 blobs per block on average following recent capacity expansions. Blob utilization is concentrated among a few L2s and blob fees remain a negligible portion of overall transaction fee revenue. The L1 has scaled ahead of L2 settlement demand, and the cost of settling on Ethereum is no longer a meaningful moat for most L2s.

Source: Coin Metrics Network Data Pro

The L2s finding durable traction are those with something more specific to offer. Base has built a distribution advantage through Coinbase’s consumer products and Arbitrum through deep DeFi liquidity. A new generation of specialized chains like MegaETH, Lighter, Robinhood Chain, Ink and others are now targeting specific use cases, or providing new business models and forms of distribution.

The Ethereum roadmap further encourages deeper L1/L2 integration through interoperability and trust-minimized architectures like native rollups, which could reinforce ETH's role as the ecosystem's liquidity and settlement core.

Glamsterdam and Other Upgrades

Scheduled for H1 2026, the Glamsterdam hard fork builds on this trajectory. By raising the gas limit toward 200 million and introducing parallel transaction execution, it targets a significant increase in L1 throughput alongside reductions in fees for complex smart contract interactions. Enshrined Proposer-Builder Separation (ePBS) integrates block building into the protocol, reducing MEV centralization and improving transaction ordering transparency. These changes are designed to make Ethereum L1 a more competitive execution environment by ensuring the base layer remains the most credible venue for high-value settlement and DeFi.

Solana

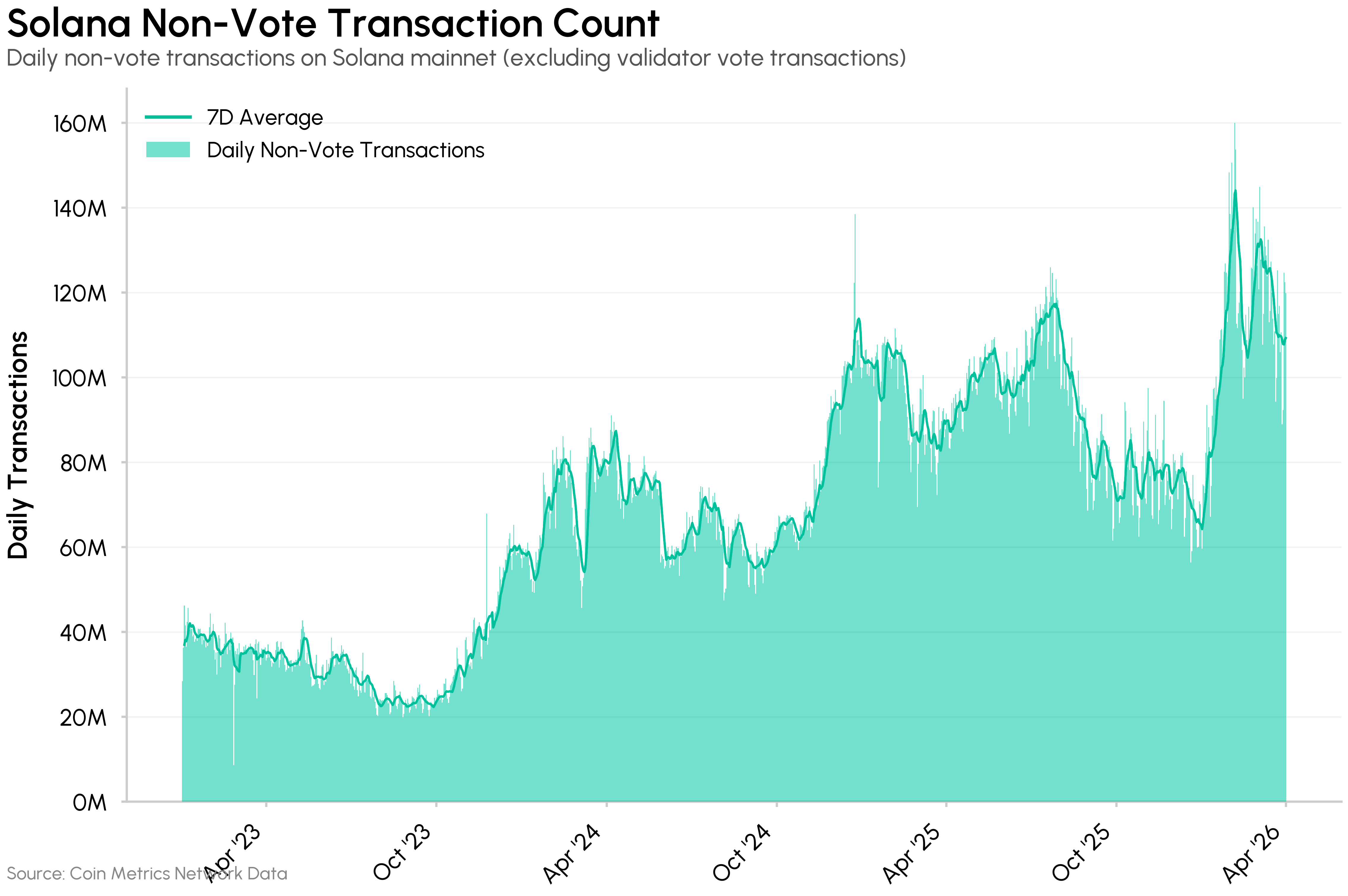

Solana is moving beyond its early reputation as the “retail and memecoin chain” towards its Internet Capital Markets vision. Sub-cent transaction fees and block times under 400 milliseconds make Solana the natural environment for applications that demand high velocity such as payments, micropayments, and high-frequency trading. This profile is attracting a distinct class of applications that require low-latency execution at scale.

Source: Coin Metrics Network Data Pro

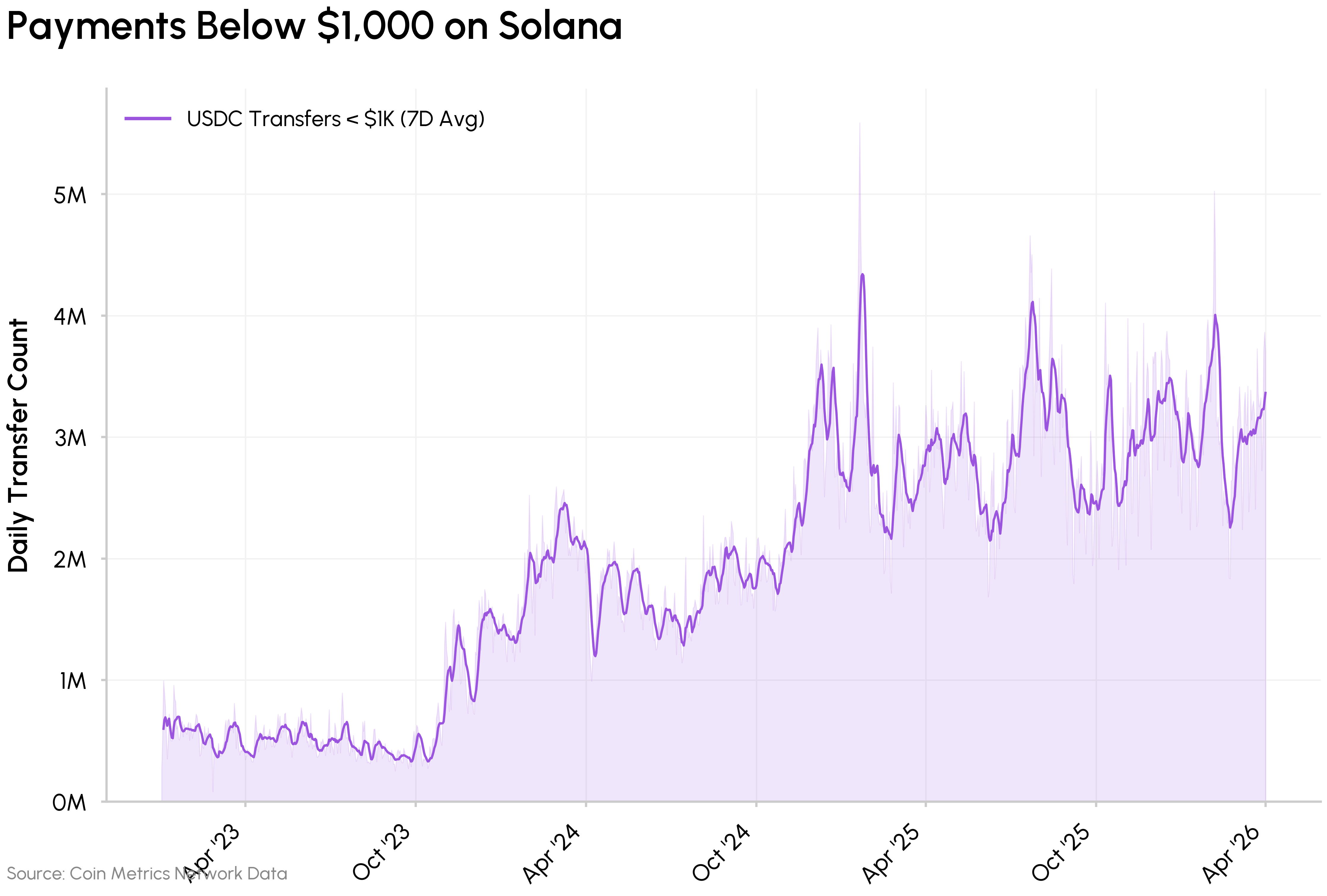

Payments & High-Frequency Micropayments

Solana’s low-cost environment has made it a leading chain for payments and consumer-scale value transfer. Sub-$1,000 USDC transfers consistently see ~3M in daily transactions, with median transaction sizes consistently below $100.

An emerging development is x402, an open HTTP payment protocol developed by Coinbase that allows any API or digital service to charge per request in stablecoins. While this remains a competitive multi-chain environment with Base and Stripe’s Tempo, Solana has captured a large share of x402 transactions, becoming one of the early adoption layers for agentic micropayments.

Source: Coin Metrics Network Data Pro

Trading Infrastructure

Solana’s throughput has also attracted sophisticated on-chain trading infrastructure. Proprietary AMMs (propAMMs), built by professional trading firms using private, off-chain pricing models, function more like dark pools than public DEXs. Unlike AMMs like Uniswap whose pricing curves are vulnerable to front-running and arbitrage, propAMMs update prices off-chain and settle on Solana, making them resistant to MEV extraction.

Alpenglow and Other Upgrades

Upcoming infrastructure upgrades are set to deepen Solana’s edge in these areas. Alpenglow targets block finality in the 100–150 millisecond range, down from ~12 seconds, by replacing Tower BFT and Proof of History with Votor, a lightweight vote aggregation protocol. BAM (Block Assembly Marketplace), developed by Jito, gives trading applications control over their own transaction ordering, enabling features like cancel prioritization and improves execution fairness.

Conclusion

As blockspace scales and costs compress, the basis of competition across blockchain networks is shifting from cost to specialization. Major L1s are building toward their architectural strengths to meet a diverse set of use cases, while purpose-built chains like Hyperliquid for trading, Canton for institutional finance, and Arc and Tempo for enterprise-grade stablecoin payments are optimizing around application specific requirements, making deliberate trade-offs around permissioning, compliance, and execution design. The question ahead is what this landscape looks like when onchain demand meaningfully scales.

A shared risk remains across onchain infrastructure. Google Quantum AI’s March 31 whitepaper suggests that breaking the elliptic‑curve cryptography that secures Bitcoin, Ethereum, and most blockchains could require fewer than 500,000 physical qubits, around 20× fewer than earlier estimates of 20 million. Early stage initiatives like Bitcoin’s BIP-360 and Ethereum’s post-quantum roadmap are taking shape. The deeper challenge is coordinating social consensus and voluntary adoption across decentralized networks, a process likely slower and less predictable than for centralized institutions.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.