Challenges of Including Long-Tail Assets in Crypto Benchmarks

State of the Network #364

Challenges of Including Long-Tail Assets in Crypto Benchmarks

Introduction

State of the Network #364

Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways

- The timing of asset inclusion in benchmarks shapes how accurately they represent the market. Staggered reconstitution helps avoid temporarily popular projects but can delay adding tokens that better reflect market performance.

- The variety of products and services a protocol offers can lead to different asset classifications, resulting in different benchmark compositions and risk‑return profiles.

- Tokens with smaller market capitalizations experience greater slippage and more fragmented liquidity across exchanges, making benchmarks that include the long tail more expensive and time‑consuming to replicate.

Introduction

Crypto long-tail assets are tokens that sit outside major market cap thresholds (typically below the top 20 coins) and are available on fewer trading venues due to fragmented liquidity.

While large-cap cryptos have received the majority of investor attention, the maturing token landscape and protocol focus on returning value to token holders can enable small-cap tokens to achieve greater returns. This is similar to small-cap stocks historically outperforming large-cap stocks over long horizons due to factors such as less coverage and compensation for greater risk.

Benchmarks provide a standard to measure the performance of assets against overarching investment strategies. Benchmarks measure broader market movements such as the S&P 500 or semiconductor industry performance against the investor’s strategy. To measure long-tail crypto performance, the appropriate benchmark is a basket of long-tail assets that represent the market’s return of similar risk-reward expectations.

An investor cannot invest in a benchmark. Rather, they invest in index funds that mimic benchmarks to achieve the same risk and expected return. If indices were to focus on small-cap crypto, there are fewer liquid venues and thinner order books that support long-tail assets. This can make it difficult to build a benchmark that can be realistically replicated. This is one of the challenges of designing benchmarks focused on long-tail assets that can be replicated by real investors. Including smaller, niche assets to compare performance against institutional portfolios introduces new challenges for designing benchmarks that accurately represent the investable universe.

In this State of the Network, we examine the challenges of adding long-tail assets to crypto benchmarks, diving into inclusion frequency, asset classification, and liquidity fragmentation.

Speed: A Double-Edged Sword

Benchmarks are not “set and forget” strategies. Assets can be added or dropped if they do not meet or are not relevant to the benchmark’s criteria, known as reconstitution. Reconstitution occurs typically on a quarterly basis depending on the benchmark’s goals for universe inclusion and market capitalization. Reconstitution ensures the market is appropriately represented by the benchmark’s included assets.

Selective Inclusion Protects from Short-Term Trends

Benchmarks work to represent passive investment across assets. Investors mimicking benchmarks aim for low turnover, incurring low or infrequent trading costs. Frequent index reconstitution leads to high turnover and trading. Investors then must buy and sell the stocks that were added and dropped respectively to continue mimicking the index.

Source: Coin Metrics Reference Rates

The use of quarterly reconstitutions avoids crypto “pump and dumps” and assets that gain significant temporary attention. These events are not reflective of the larger market performance. The chart above compares performance of an even-weighted DeFi benchmark that includes existing assets classified as DeFi with one project that gained popularity in 2024. If it had been included since then, the benchmark would have underperformed the version without the asset by over 300 basis points.

Delayed Inclusion Fails to Represent the Market

If appropriate assets are not included in a benchmark in a timely manner, the benchmark struggles to represent the market. Assets not in the benchmark cannot contribute to reducing volatility, diversifying the benchmark, and protecting returns.

Source: Coin Metrics Reference Rates

Morpho, a decentralized lending protocol, has continued to attract capital as institutional interest in vaults grow. Through institutional partnerships including Coinbase directly lending cbBTC in Morpho Vaults, Morpho is becoming a core component of the DeFi landscape.

Morpho’s inclusion in an even-weighted DeFi benchmark modestly improves the benchmark’s Sharpe Ratio. The speed of asset inclusion can both help and hurt efforts to represent broader market performance. When is it too early to recognize if this is temporary popularity from the market versus when is it too late to report in a benchmark that this has been an important, unrepresented infrastructure that contributes to the market’s performance?

Classification Differences Alter Benchmark Composition

Like traditional finance benchmarks categorizing equities by industry, crypto benchmarks can also be categorized by industry-wide classifications. Classification of crypto, whether it is based on what the protocol does or if the asset is backed by other investments, can have different interpretations.

In partnership with MSCI and Goldman Sachs, our Datonomy classification creates inclusion standards for an investable universe. Assets are classified based on the token or protocol’s products and services.

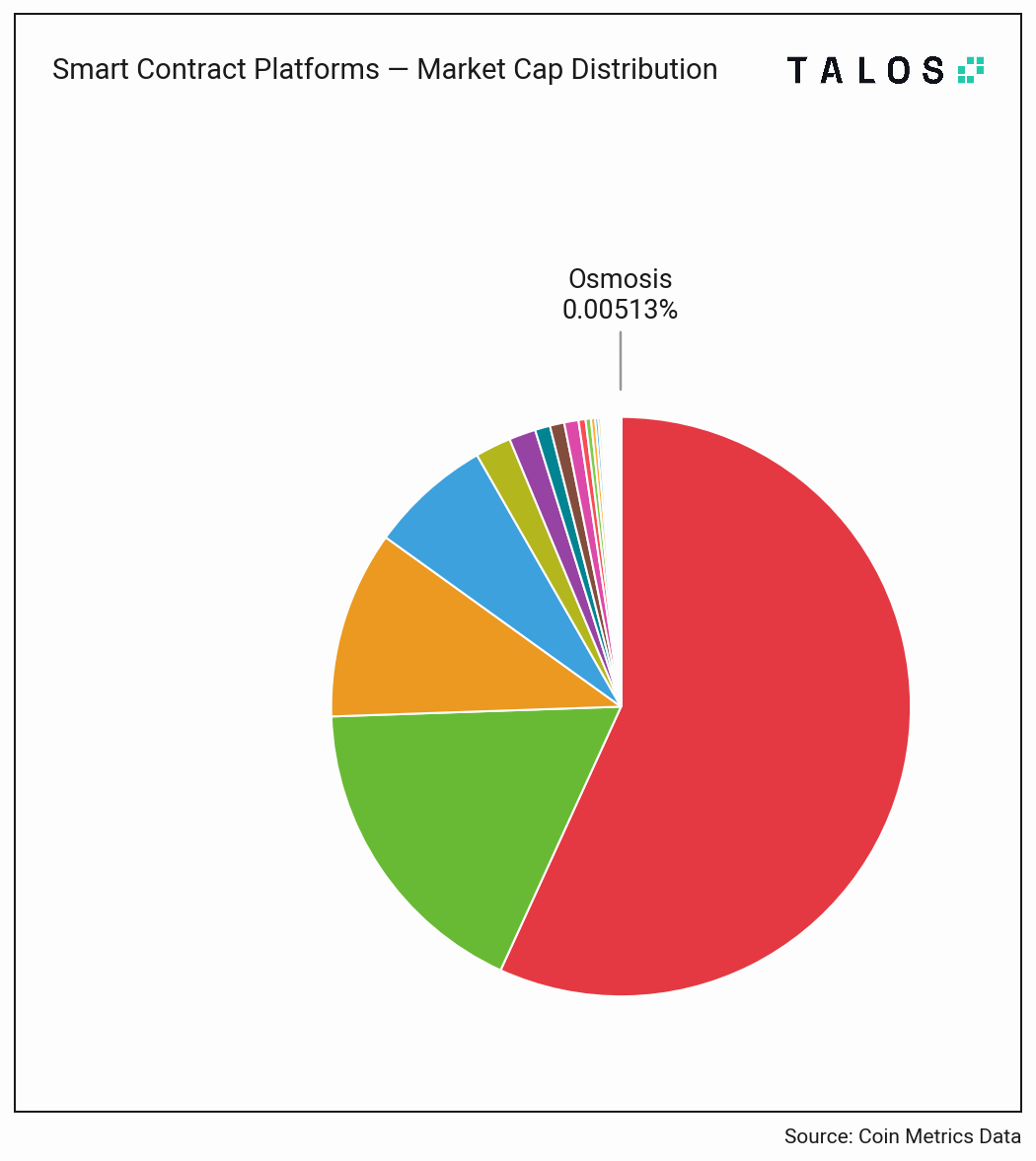

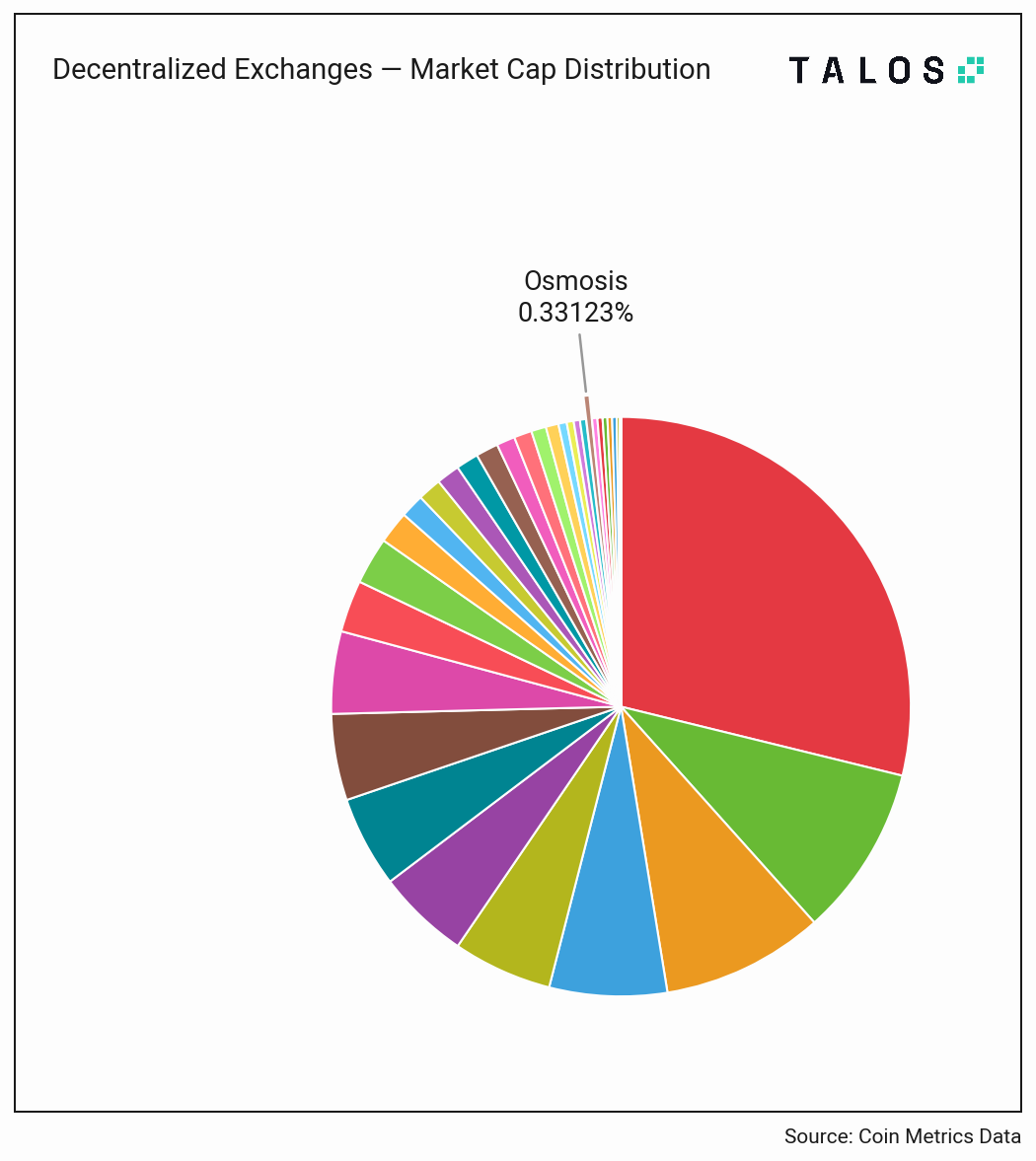

Classifications can vary because of the expansive services and operations a protocol provides. For example, Osmosis (OSMO) supports token swaps, acting as a decentralized exchange. To operate, Osmosis has a decentralized validator set validating transactions and approving transfers in and out of the network.

Osmosis could be considered a Layer 1 network because it has a decentralized validator set and charges fees in OSMO tokens. It can also be considered a Decentralized Exchange because Osmosis specializes in facilitating token swaps. Selecting a specific classification changes how a benchmark performs with or without the asset.

Despite OSMO not comprising a large weight in a market cap-weighted benchmark for either classification, this example emphasizes the challenge of appropriately classifying assets for accurate benchmarking and return comparison.

Liquidity Fragmentation for Equal-Weighted Benchmarks

Equal-weighted benchmarks provide equal exposure to assets. This is beneficial when investors want equal exposure or there are disproportionately few assets weighted heavily in the benchmark based on market cap.

However, to replicate an equal-weighted benchmark, enough tokens must be available for purchase across exchanges to reduce price impact. Slippage measures the difference between expected trade value and actual execution value, driven by price movements in the order book.

Source: Coin Metrics Market Data Pro

Large-cap assets, on average, have lower slippage than long-tail assets. It becomes easier to replicate an even-weighted benchmark for large-cap crypto because there is less price impact for purchases at scale. Additionally, the quote asset of each market affects slippage. USDT markets are consistently more liquid across assets than USDC and USD markets, helping replicate benchmarks more easily.

Source: Coin Metrics Market Data Pro

Another way to look at liquidity is order book depth. Order book depth examines how many tokens or dollars are within a certain percent of the mid price. BTC and ETH are very liquid around the mid‑price, and as we move toward long‑tail assets, order‑book depth becomes thinner. It can be increasingly difficult for a portfolio to replicate a benchmark with over $1 million in an equal-weighted benchmark of long-tail assets if the order book is thin with minimal price impact.

Ethena (ENA) is a stablecoin issuer with over $1 billion market capitalization. Ethena is best known for its issuance of the USDe stablecoin, a delta-neutral, yield-bearing stablecoin. USDe is an alternative stablecoin to fiat-backed stablecoins and growing in popularity. If ENA were included in an equal-weighted benchmark, investors with sizable allocations will struggle to replicate the benchmark.

Source: Coin Metrics Market Data Pro

Filling an order of $800,000 in ENA on Binance incurs over 2% of slippage on a weekly average. The Binance-USDT pair is the only market out of 37 markets that can support less than 5% slippage on the trade size on both bid and ask. Aggregating orders across exchanges and acquiring ENA over time can reduce the price impact but could delay the replication of the benchmark.

Conclusion

It is important to recognize the challenges that arise when including long‑tail assets in benchmarks. As institutional adoption of crypto protocols grows and investors diversify to improve their risk exposure, measuring long‑tail asset performance relative to the market becomes crucial for comparing returns.

Comparing model benchmarks, maintaining up‑to‑date knowledge of relevant assets in the market and aggregating market liquidity across venues can help in designing benchmarks that incorporate the long tail while remaining representative and investable.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.