Coin Metrics State of the Network is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Key Takeaways

- Crypto markets extended their recovery in April, with Bitcoin (BTC) rising by ~16% to over $78K.

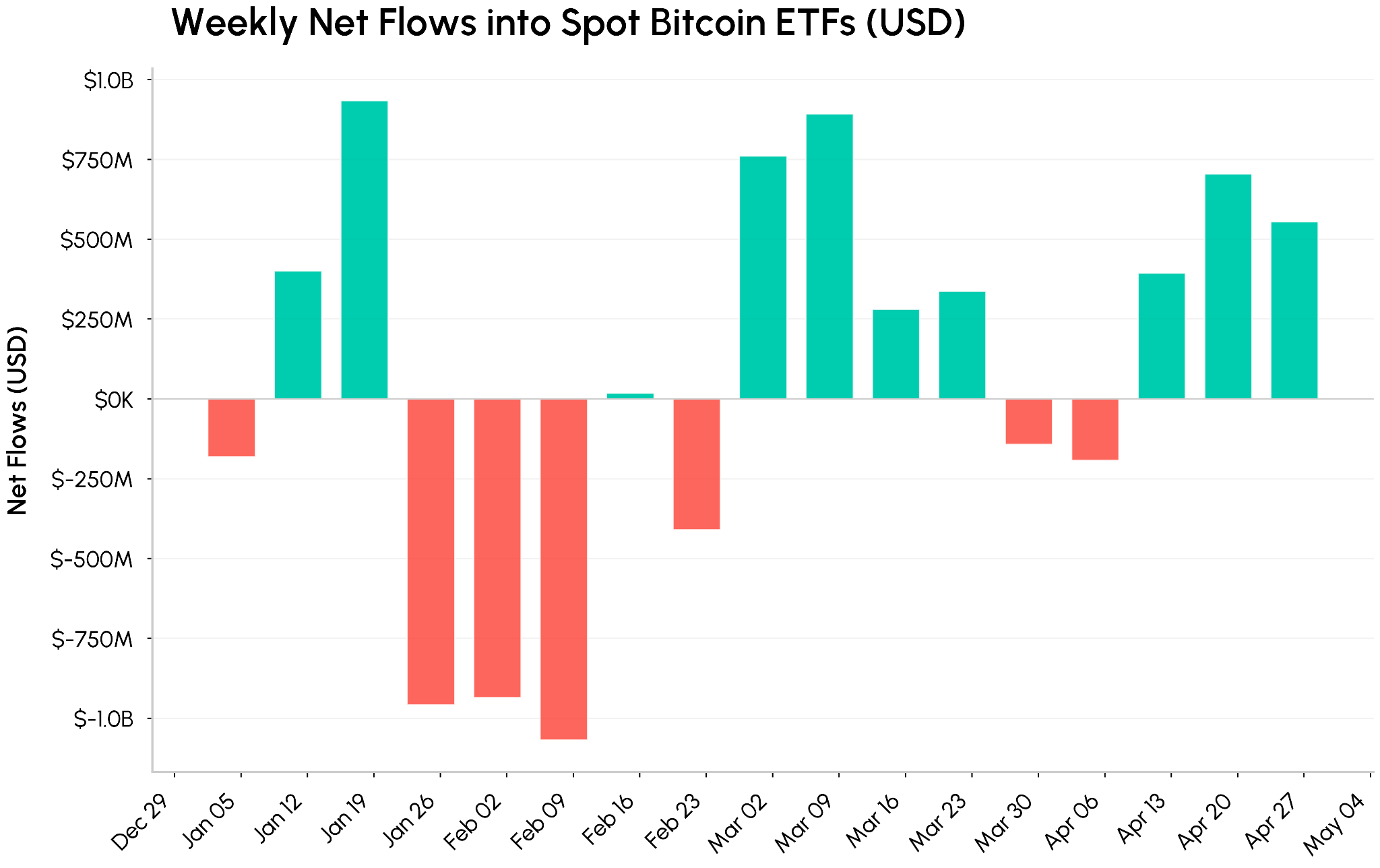

- April saw the strongest monthly net inflows into spot Bitcoin ETFs since October 2025, while futures positioning leaned short and funding stayed mostly negative.

- Tokenized treasuries are emerging as a core onchain yield and reserve layer, competing with idle stablecoins and higher-risk crypto collateral by offering exposure to short-duration U.S. government debt.

In this issue of State of the Network, we provide an overview of key developments that shaped crypto markets over the past month.

Market Overview

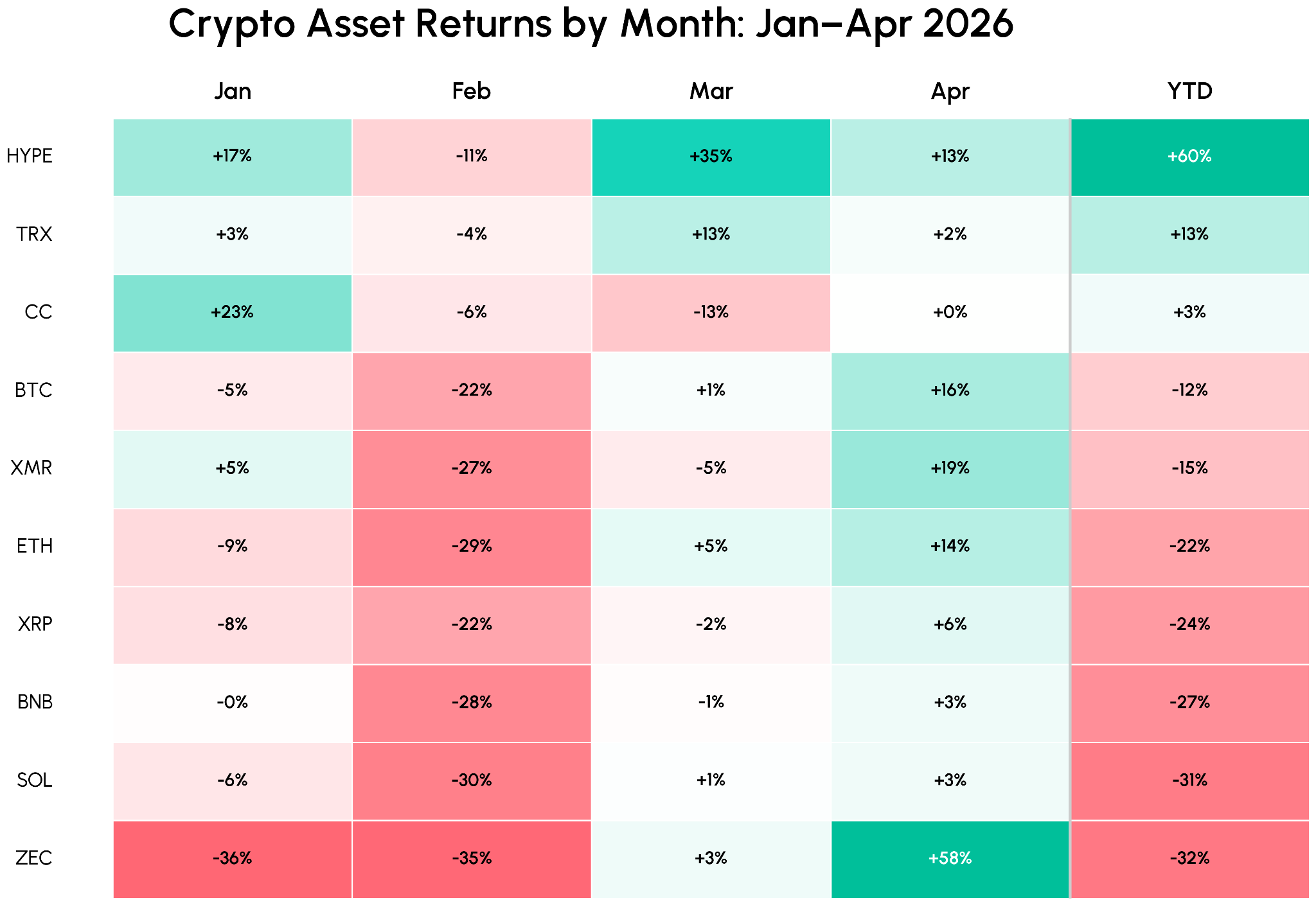

In April, the total crypto market capitalization climbed by around 10% to ~$2.7T, extending the market’s recovery against a backdrop of extended geopolitical conflict and disruption to oil and energy markets. Bitcoin (BTC) and Ethereum (ETH) rose 16% and 14% respectively, while major equities indices also rebounded from their March lows. Bitcoin dominance remains around 57% as BTC pushes towards the upper end of its recent price range, with notable altcoin outperformers over the month including Zcash (+59%) and Morpho (+33%).

The month also introduced new urgency in crypto’s quantum tail risk, with Google’s Quantum AI group publishing a whitepaper estimating that breaking the elliptic‑curve cryptography securing Bitcoin and most public blockchains could require roughly 20× fewer resources than previously thought (around 500,000 physical qubits), compressing the timeline for a credible quantum threat.

At the same time, April was a challenging period for the onchain ecosystem, with events like the Drift hack and KelpDAO rsETH bridge exploit raising questions about the risk‑reward of depositing onchain and how protocol level risk management and cross‑chain infrastructure can better isolate risk.

Flows & Positioning

Institutional Demand Rebuilds

Institutional demand continued to build underneath through improving ETF flows, adding to March’s momentum since the US-Iran ceasefire came into effect. Net inflows into spot Bitcoin ETFs in April crossed roughly $1.7B, making it the strongest month since October 2025.

Demand was further reinforced by Strategy’s bitcoin purchases totaling 56,238 BTC (~$4.1B) over the same period. This now puts Strategy’s holdings of 818,334 BTC ahead of BlackRock’s IBIT fund, which holds a total of ~802,654 BTC. Unlike prior waves of buying that were funded mainly by at-the-market (ATM) common stock issuance, recent purchases have been driven largely by its Stretch (STRC) perpetual preferred stock.

As a perpetual preferred stock, STRC provides a variable dividend of 11.5%, and is designed to trade near a $100 par value through dividend adjustments. When STRC trades near or above par, Strategy issues new shares via its ATM program and channels the proceeds into spot BTC purchases, turning this instrument into a repeatable funding source for its accumulation strategy.

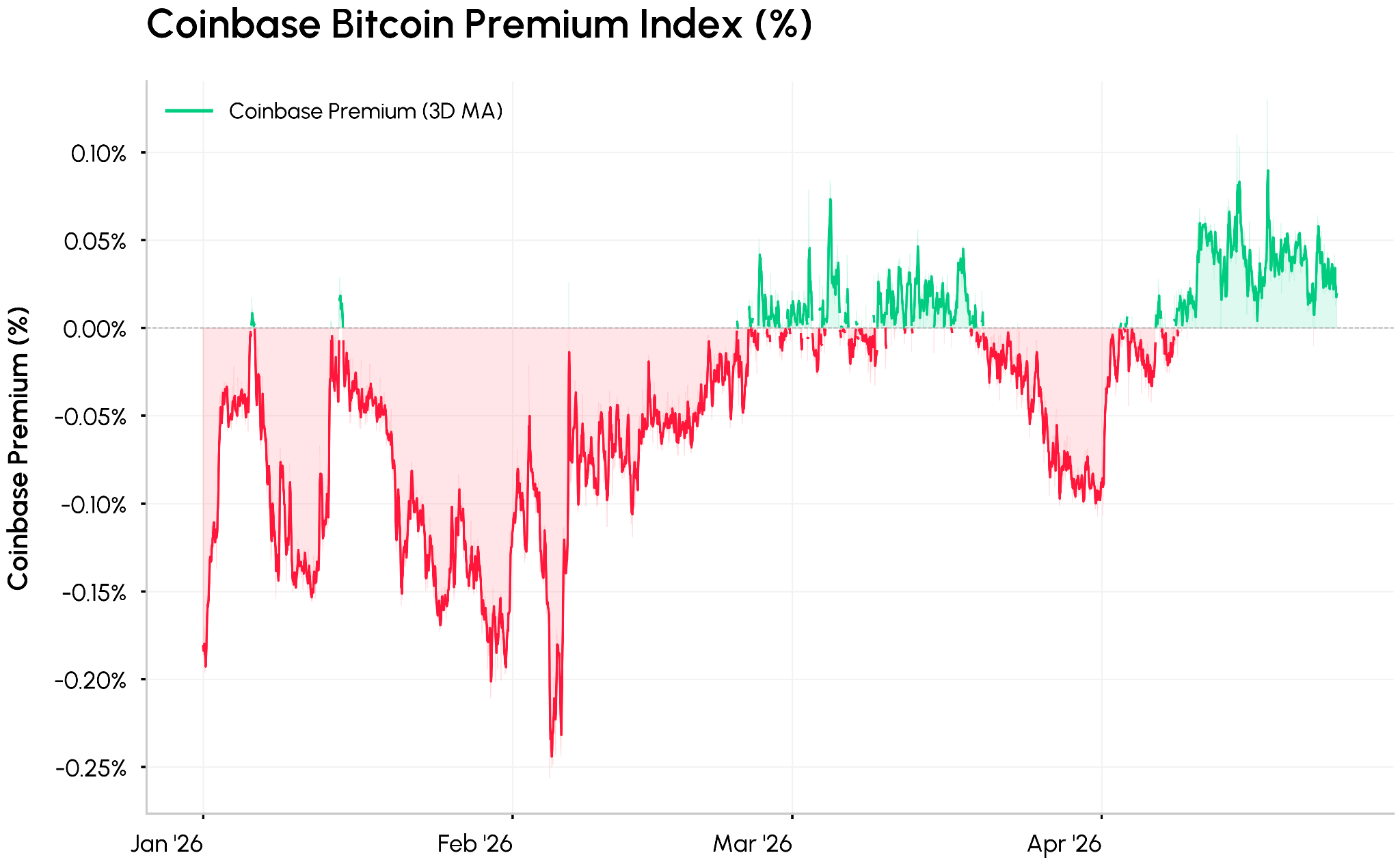

The Coinbase premium index, which tracks the difference between BTC/USD on Coinbase and BTC/USDT on Binance, also moved into positive territory, confirming the influence of U.S. spot demand. This rebuilding demand comes alongside BTC exchange reserves reaching a 7-year low of ~2.3M, indicating that cons are moving into long-term storage rather than onto exchanges for sale.

Futures Positioning Leans Short

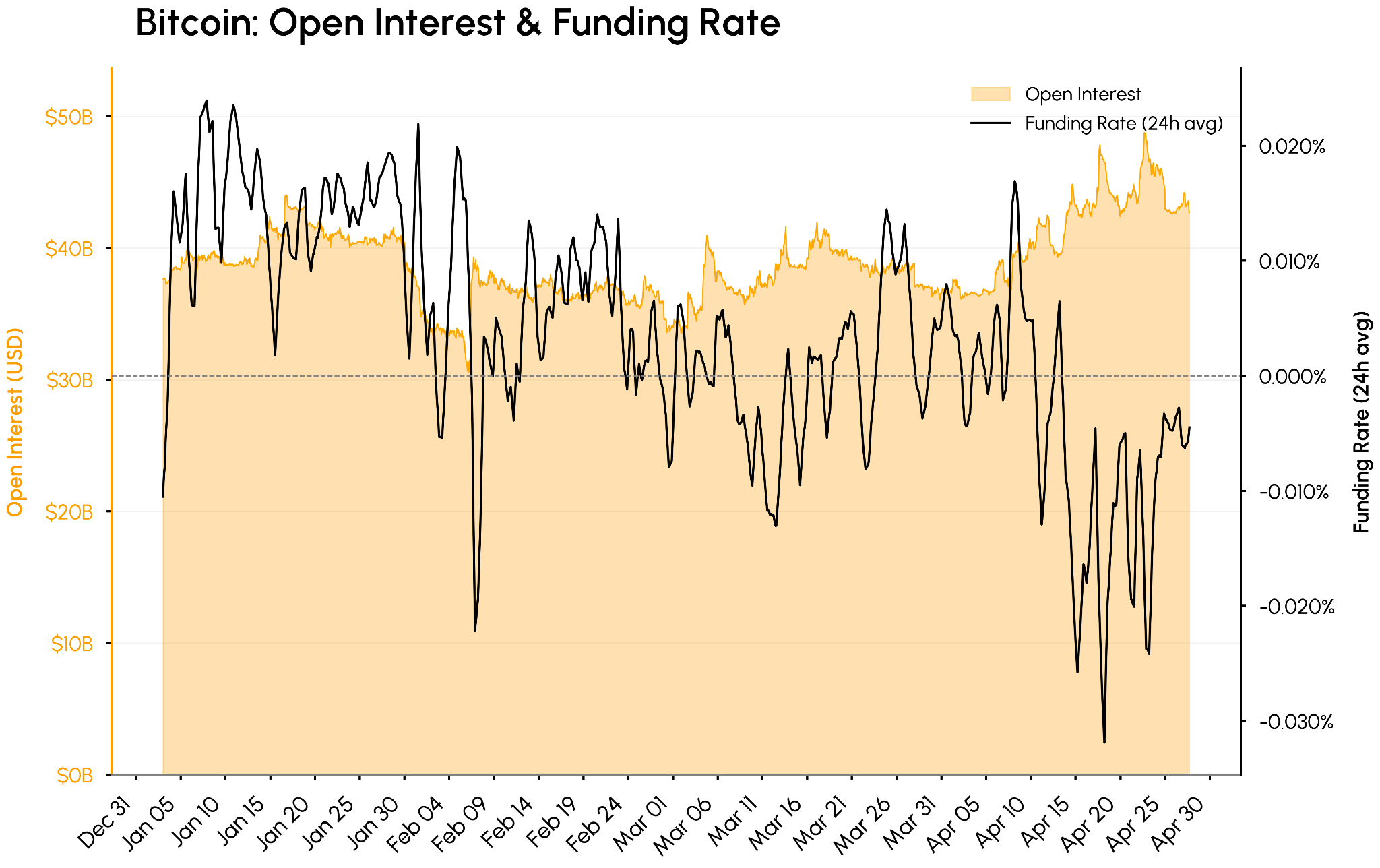

At the same time, derivatives positioning remains more cautious. As the chart above shows, Bitcoin futures open interest pushed higher toward $50B, while BTC funding rates spent most of April in negative territory. Traders have been willing to remain short or hedged as spot buyers accumulate. The combination of high open interest and persistent negative funding suggests a market where the structural spot bid is being met by short positioning, leaving room for further short‑squeeze dynamics. Since March, BTC has seen roughly $1.9B in short liquidations, indicating that parts of this rally have already been driven by forced covering rather than broad conviction.

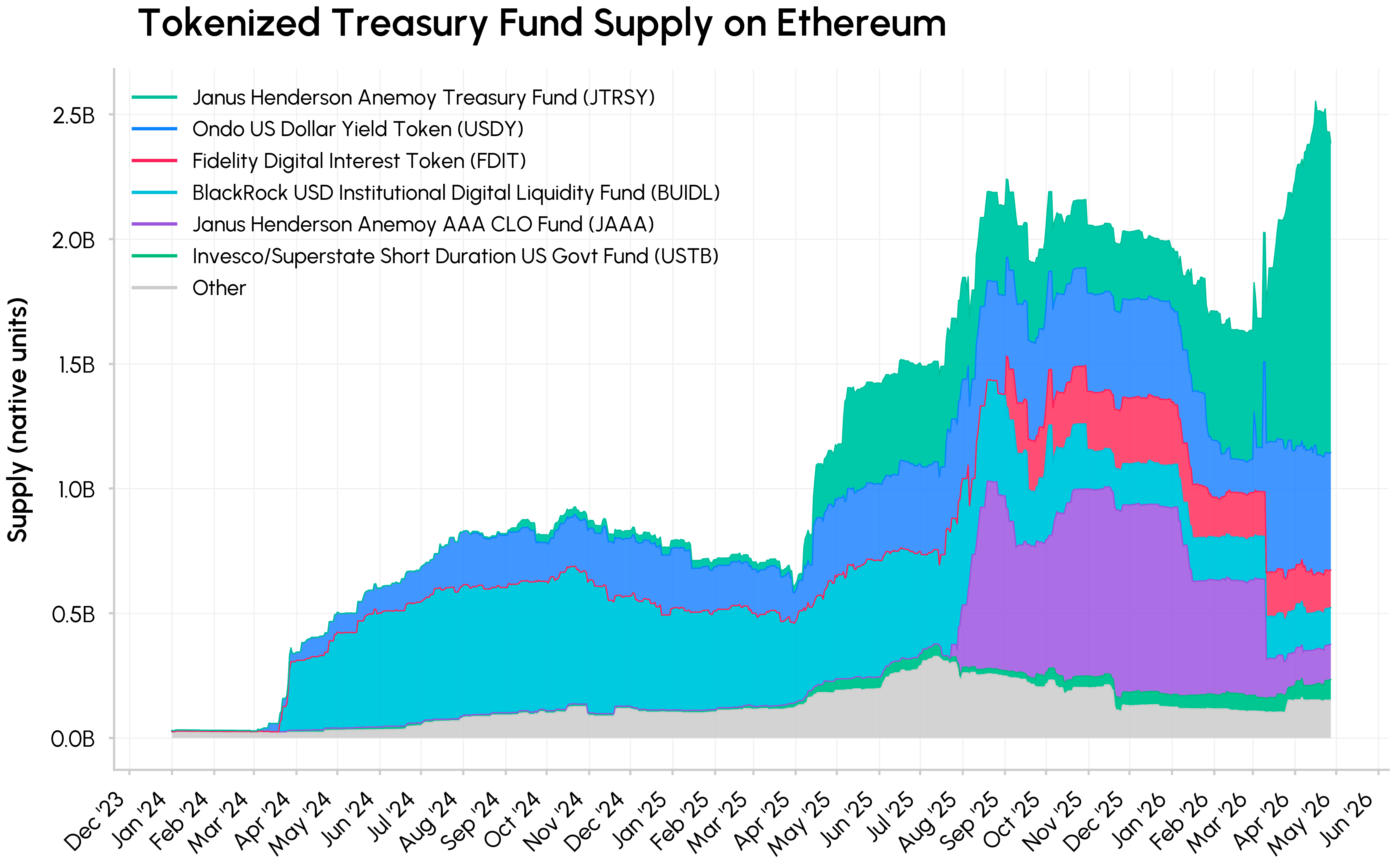

Tokenized Treasuries & Onchain Yield

Tokenized U.S treasuries have continued to gain traction as one of the fastest growing segments in the real world asset (RWA) market. In an environment of elevated interest rates, many funds provide tokenized exposure to the “risk free rate”, offering an alternative to non-yielding stablecoins through tokens (shares) that represent claims on short‑duration government debt held in funds.

The circulating supply of major tokenized treasury funds such as Ondo’s US Dollar Yield (USDY) and Short-term US Government Bond Fund (OUSG), Janus Henderson’s Anemoy Treasury Fund (JTRSY), and BlackRock’s BUIDL have grown from effectively zero in early 2024 to its highest levels yet by April 2026 on Ethereum, while also expanding their footprint cross-chain.

As tokenized RWAs and funds compete more directly with yield‑bearing stablecoins, and other forms of crypto collateral, the risk–reward spectrum for onchain yield is coming into sharper focus. At one end are onchain representations of off‑chain assets such as tokenized treasuries, where returns are mostly driven by interest rates and fund structure but still involve issuer, smart‑contract, and liquidity risk. At the other end, yield‑bearing stablecoins, LSTs/LRTs, and associated lending markets and vaults add further layers of operational, governance, liquidity, and rehypothecation risk, as recent incidents have highlighted.

Therefore, allocators are likely to think of onchain yields in terms of the buckets of risk they are taking, from offchain exposures like tokenized treasuries or credit, blue-chip DeFi collateral to more complex and leveraged strategies.

Conclusion

Crypto markets have continued to recover from their lows, supported by rebuilding institutional appetite through spot ETFs and aggressive corporate balance sheet accumulation from Strategy. Positioning leans cautious, with rising futures open interest, negative funding, and order book liquidity still below 2025 levels for majors and altcoins. In the near term, sustained ETF inflows and momentum in CLARITY Act odds, will be key drivers, while quantum security remains a long‑term risk. Against this backdrop, tokenization and DeFi risk management remain central themes, as tokenized treasuries and other RWAs increasingly move onchain and anchor the yield landscape.

Disclaimer: The information herein is provided for informational purposes only. Talos Trading, LLC and its affiliates (“Talos”) does not give any representations or warranties in relation to the accuracy, validity, or completeness of the information of this material, including without limitation the factual information obtained from publicly available sources considered by Talos to be reliable at the time. Talos accepts no liability for any consequences of using the information contained in this material. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication and are subject to change without notice. Neither this material nor any copy thereof may be taken, reproduced, or redistributed, directly or indirectly, without Talos’s prior written permission. Any views or opinions expressed are those of the authors and do not necessarily reflect the views of Talos. This communication does not constitute an offer to buy or sell, or a promotion or recommendation of, any digital asset, security, derivative, commodity, financial instrument, or product or trading strategy. This document and information are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Subscribe

If you’d like to get State of the Network in your inbox, please subscribe below.

Latest insights and research

Request a demo

Find out how Talos can simplify the way you interact with the digital asset markets.